Non-Performing Loan Guide: Insights & Solutions for 2025

The global financial landscape is shifting fast, with non-performing loan volumes reaching new highs in 2025. In some regions, banks are facing NPL ratios not seen since the aftermath of the pandemic.

Why does this matter? Non-performing loan challenges can ripple through banks, entire economies, and even impact everyday borrowers. As risks climb, so does the need for fresh strategies.

This guide breaks down what non-performing loans are, why they matter, and the most effective solutions for individuals, institutions, and policymakers. Ready to navigate the NPL landscape and protect your financial future? Start here.

Understanding Non-Performing Loans: Definition and Key Concepts

The non-performing loan issue sits at the center of today’s financial conversations. As economies adapt in 2025, understanding this concept is crucial for banks, businesses, and individuals. A non-performing loan signals more than a missed payment—it reflects deeper financial stresses and systemic risks.

What Is a Non-Performing Loan?

A non-performing loan is a credit facility where the borrower has not made scheduled payments for at least 90 days, or where there is significant doubt about full repayment. Banks use several criteria to classify a loan as non-performing, including missed payments, capitalized interest, or evidence of high default risk.

Definitions can vary across regions. For example, the European Union applies a 90-day overdue rule, while the United States and Asia have their own standards. Despite these differences, the core idea remains consistent: a non-performing loan reflects financial distress. For readers who want to explore more financial terminology, the Financial terms glossary is a helpful resource.

Types of Non-Performing Loans

Non-performing loans come in several forms. Consumer NPLs involve personal loans, credit cards, or mortgages, often affecting individuals. Commercial NPLs, on the other hand, relate to business lending—either to small and medium-sized enterprises (SMEs) or large corporations.

Loans can also be secured, like mortgages backed by property, or unsecured, such as credit cards. Notably, non-performing property loans (NPPLs) have played pivotal roles in banking crises, as seen during the subprime mortgage crisis. The distinction between SME and large corporate NPLs is crucial for risk assessment.

| Type | Secured/Unsecured | Example Sector |

|---|---|---|

| Consumer NPL | Both | Mortgages, credit |

| Commercial NPL | Both | SME, corporations |

| Property (NPPL) | Secured | Real estate |

Why NPLs Matter: Economic and Banking Impact

A rising non-performing loan ratio can put significant strain on banks. NPLs reduce a bank’s profitability because they tie up capital and limit the ability to issue new loans. High levels of NPLs can slow down economic growth, as credit becomes less available for households and businesses.

The impact often spills across borders, especially in interconnected economies like the EU. After the 2008 financial crisis, the surge in non-performing loans became a major concern, signaling systemic financial stress. Policymakers now watch NPL trends closely as early warning signs of broader instability.

How NPLs Are Measured and Reported

Banks and regulators use key metrics to track non-performing loan trends. The NPL ratio shows the proportion of non-performing loans to total loans, while the NPL coverage ratio indicates how much provision is set aside for potential losses.

Reporting standards such as IFRS9 and Basel III provide frameworks for consistent measurement, but challenges persist due to inconsistent definitions. Transparency is essential for effective NPL management. Since 2017, the EU has pushed for harmonized reporting, aiming to make cross-country comparisons easier and enhance financial stability.

The Current State of Non-Performing Loans in 2025

The financial world in 2025 is facing a renewed spotlight on the non-performing loan challenge. After a brief dip, NPL volumes are rebounding globally, with markets and regulators keeping a close eye on emerging risks. This year, understanding the current state of non-performing loan issues is critical for banks, investors, and policymakers alike.

Global and Regional NPL Trends

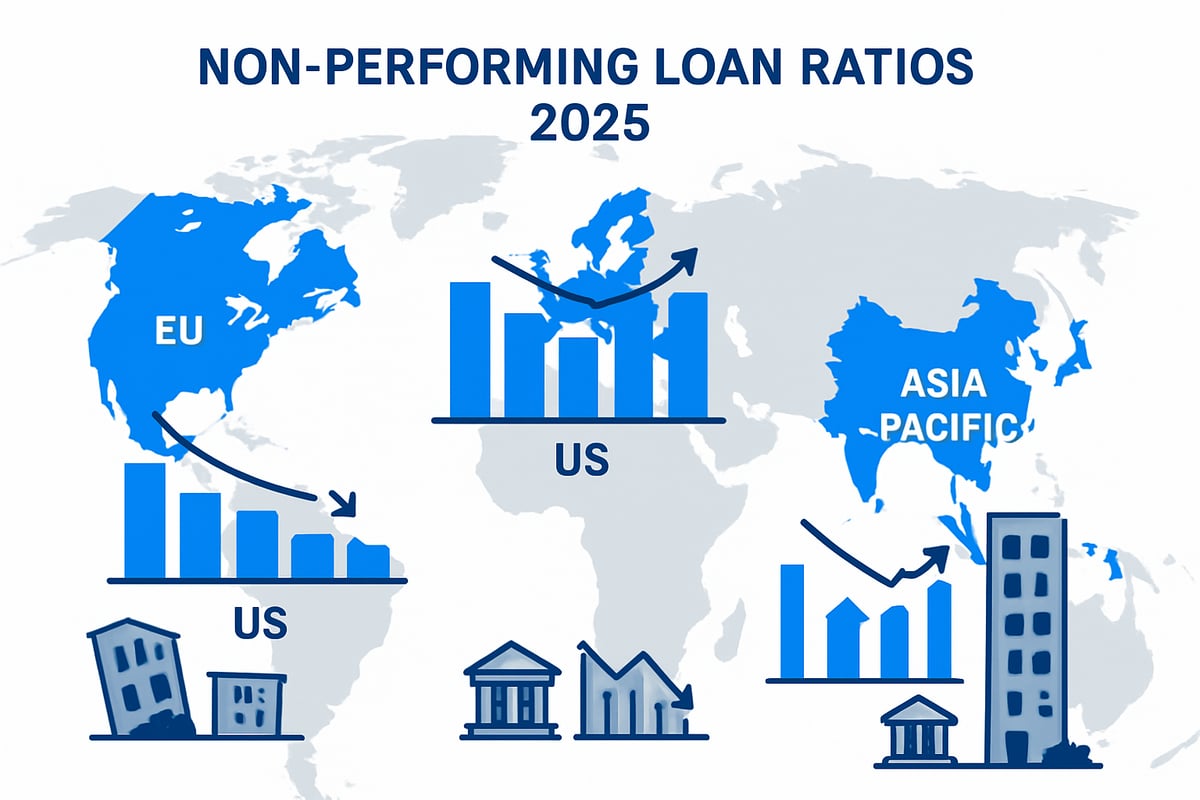

In 2025, non-performing loan volumes have surged in several regions, reversing the declining trend seen in the aftermath of the pandemic. The Eurozone faces a warning from the ECB, estimating NPLs could reach €1.4 trillion, particularly as government support measures fade. Asia-Pacific markets are also experiencing a pickup in NPLs, especially in countries reliant on sectors hit hardest by global slowdowns.

The United States continues to monitor its non-performing loan ratio closely, with recent data showing a moderate uptick after years of relative stability. For those interested in historical and current figures, the US Non-Performing Loans Ratio, 1985 – 2025 provides a comprehensive timeline of these trends. Meanwhile, some emerging economies are struggling with persistently high NPL ratios, while others have managed to contain the fallout.

Causes of NPL Accumulation

Several factors are driving the accumulation of non-performing loan portfolios in 2025. Economic downturns, triggered by inflation and uneven recoveries, have resulted in higher unemployment and business closures. Lenders that relied on looser credit standards during the pandemic are now seeing those loans turn sour.

Industry-specific shocks, such as the continued slump in global tourism and real estate volatility, are major contributors. Temporary policy responses like payment moratoria delayed the recognition of non-performing loan problems but did not solve them. Borrower financial literacy and changing consumer behaviors also play a role, with some households and businesses struggling to adapt to new economic realities.

Sectors Most Affected by NPLs

The non-performing loan landscape in 2025 is defined by sectoral concentration. Real estate and property loans are among the most vulnerable, especially in markets where prices have stagnated or declined. Small and medium-sized enterprises (SMEs) face heightened risk, as many lack the buffers needed to survive prolonged downturns.

Consumer credit, including auto and personal loans, is another hotspot for non-performing loan growth. Banks with heavy exposure to these sectors are experiencing increased concentration risk, raising concerns about broader financial stability. Cross-sector contagion is a real threat, as defaults in one area can quickly impact others, amplifying systemic risk.

Key Statistics and Data Points

The latest data reveal significant disparities in non-performing loan ratios by country and sector. In the EU, the average NPL ratio has fallen by over one third since 2014, yet volumes remain elevated in certain southern European nations. Asset management companies (AMCs) are actively purchasing and managing NPL portfolios, helping to stabilize bank balance sheets.

Secondary markets for non-performing loan trading have expanded, with transaction volumes reaching new highs in 2025. Recent legislative milestones, such as EU directives supporting NPL sales, play a pivotal role in fostering market development. The continued growth of AMCs and secondary markets signals a maturing approach to non-performing loan resolution.

| Region | 2025 NPL Ratio | Key Sector Impacted |

|---|---|---|

| Eurozone | Up to 7% | Real Estate, SMEs |

| US | 1.7% | Commercial, Consumer |

| Asia-Pacific | 4-8% | Property, Manufacturing |

The Impact of COVID-19 and Economic Recovery

COVID-19 profoundly shaped the non-performing loan landscape, with payment moratoria and loan deferrals masking the true scale of credit risk. As these measures expire, banks are confronting a delayed surge in NPL recognition. The ECB and EU Commission have projected further growth in NPLs, prompting policy responses like dividend bans and the creation of "bad banks" to safeguard stability.

The European Commission's 2020 action plan set the stage for more coordinated NPL management, but risks remain as economic recovery is uneven across regions. Some countries are seeing NPLs spike as support ends, while others are weathering the storm. Ongoing vigilance and adaptive strategies are essential to navigating the non-performing loan challenge in 2025.

Challenges in Resolving Non-Performing Loans

Resolving a non-performing loan is rarely straightforward. Multiple obstacles stand in the way, making it a complex process for banks, regulators, and borrowers alike. Let’s break down the key challenges that shape the landscape in 2025.

Structural and Regulatory Hurdles

Structural and regulatory issues often complicate non-performing loan resolution. Definitions and valuation methods for non-performing loans can vary significantly between countries and even banks. This inconsistency leads to confusion and delays, as there is no single standard to follow.

Banks might hesitate to write off non-performing loans due to worries about capital adequacy or fear of recognizing losses on their balance sheets. Regulatory frameworks may not always provide clear guidance, which can stall decision-making. Recently, there has been rising concern that banks are not making enough proactive provisions, especially as non-performing loans are on the rise again for banks, yet no proactive provisions made.

This reluctance can ultimately increase risks for the entire financial system, making early and consistent action critical.

Market and Operational Barriers

A major challenge in resolving a non-performing loan is the lack of mature secondary markets. Many countries have limited investor interest, so banks find it hard to sell off risky assets. When a non-performing loan does get sold, the price may be heavily discounted due to uncertainty about recovery.

Operationally, due diligence and valuation are time-consuming and costly. Investors often demand steep discounts, sometimes buying loans for as little as 1% of their original value. This creates a wide pricing gap and discourages transactions.

High transaction costs, combined with limited market infrastructure, can leave banks holding onto non-performing loans longer than they should, which increases systemic risk.

Legal and Judicial Obstacles

The legal environment can also slow down non-performing loan resolution. National insolvency and foreclosure laws differ widely, making cross-border collections especially difficult. Complex court procedures mean it can take years to recover collateral or settle claims.

Consumer protection laws, though necessary, sometimes create additional hurdles for banks trying to enforce their rights. For example, the European Union has been working to harmonize collateral recovery frameworks, but inconsistencies still persist.

These obstacles drive up both the time and cost of resolving a non-performing loan, reducing recovery rates and discouraging new lending.

Incentive Misalignments and Governance Issues

Banks may be tempted to understate their non-performing loan portfolios due to reputational risk or regulatory pressure. This lack of transparency can delay the recognition of losses and weaken trust in the financial system.

Government interventions, such as setting up asset management companies, can sometimes create moral hazard, where banks rely on bailouts instead of managing risk responsibly. Weak corporate governance in loan management can further complicate matters.

Stakeholder conflicts can arise. Banks, regulators, and borrowers often have different priorities, making it difficult to agree on the best course of action for non-performing loan resolution.

Societal and Economic Consequences

The impact of a non-performing loan extends beyond banks. High levels of non-performing loans can drag down credit supply, making it harder for small businesses and consumers to access financing.

Systemic risk grows as more loans go unpaid, potentially threatening financial stability. Social consequences, such as housing crises or rising unemployment, often follow. For instance, during the subprime mortgage crisis in ASEAN countries, non-performing loan spikes contributed to widespread economic hardship.

Addressing these challenges requires coordinated action and a deep understanding of both financial and social dynamics.

Policy Responses and Regulatory Solutions for NPLs

The global response to the non-performing loan challenge has evolved rapidly, with policymakers and regulators adopting diverse strategies to stabilize banks and protect economies. In 2025, the mix of regulatory tools, market initiatives, and consumer protections continues to shape how countries manage the risks linked to non-performing loan portfolios.

Decentralized vs. Centralized Approaches

When tackling non-performing loan problems, policymakers often weigh decentralized and centralized strategies. Decentralized solutions involve each bank setting aside provisions, following regulations, and managing their own NPL stock. Centralized approaches, in contrast, create asset management companies (AMCs) or "bad banks" to pool and resolve toxic assets across institutions.

Consider the case of Korea Asset Management Corporation, which helped clear non-performing loan burdens after the Asian crisis. Hybrid models, such as the EU’s action plan, blend both methods for greater flexibility. The choice depends on the scale of the crisis and the health of the financial sector. For example, the FHFA Releases Update of Enterprise Sales of Non-Performing Loans offers a look at how U.S. agencies have managed NPL sales through centralized programs, achieving positive outcomes for both banks and borrowers.

Legislative and Regulatory Initiatives

Robust legislative action is key to addressing the non-performing loan challenge. The EU’s 2017 ECOFIN action plan set the stage for harmonized rules, while the Credit Servicers and Credit Purchasers Directive (2021/2167/EU) standardized how distressed assets are handled. Many countries have tightened capital requirements, mandating minimum coverage for new NPLs.

National reforms have also modernized insolvency and enforcement laws, making it easier for banks to recover collateral. A harmonized approach across the EU has supported the development of secondary markets and improved investor confidence in the non-performing loan sector.

Enhancing Transparency and Reporting

Transparency is essential for effective non-performing loan management. International standards like IFRS9 and Basel III require banks to disclose NPL data using consistent methodologies. The EU has pushed for harmonized reporting, setting up the NPL Advisory Panel in 2021 and extending its mandate in 2023.

Consultation processes, such as the 2021 targeted review of secondary market efficiency, have helped identify data gaps and streamline disclosures. These initiatives boost trust among investors, regulators, and the public, ensuring that non-performing loan risks are identified and addressed promptly.

Secondary Markets and Securitization

A vibrant secondary market is vital for resolving non-performing loan portfolios. Legislative support has paved the way for NPL sales, securitization, and trading via asset-backed securities and covered bonds. The EU’s blueprint for national AMCs encourages standard practices and transparency.

When investors can confidently buy and sell non-performing loan assets, banks free up capital and refocus on new lending. Securitization, while complex, can help spread risk and attract a broader pool of investors, supporting the overall stability of the financial system.

Proactive Bank Supervision and Incentives

Prudential supervision is a cornerstone of non-performing loan policy. Regulators require banks to hold extra capital against NPL risks, apply early intervention frameworks, and sometimes ban dividends to preserve bank strength. During the 2020 pandemic, the ECB’s dividend ban ensured banks could absorb losses from rising non-performing loan levels.

Incentives for forbearance and debt restructuring encourage banks to work with distressed borrowers, while ongoing supervision keeps risks in check. Early action is crucial for preventing small NPL problems from becoming systemic threats.

Consumer Protection and Social Considerations

Protecting borrowers is a top priority in non-performing loan policy. Regulations aim to balance creditor rights with safeguards for individuals and families, especially in residential property cases. Out-of-court recovery mechanisms help resolve disputes efficiently, while rules against predatory NPL sales protect vulnerable consumers.

For example, EU directives include provisions ensuring fair treatment of homeowners during foreclosure. Social impact assessments guide policymakers, helping them design solutions that support both financial stability and social well-being.

Effective Strategies for Managing and Resolving NPLs in 2025

Managing a non-performing loan portfolio in 2025 requires a blend of traditional banking skills and innovative tools. Banks, investors, and policymakers must stay proactive, using structured steps to address risks and unlock recovery value. Below, we explore the most effective, actionable strategies for tackling non-performing loan challenges in today's financial landscape.

Step 1: Early Detection and Risk Assessment

Timely identification is the first defense against non-performing loan escalation. Banks must reinforce credit risk assessment at the point of origination, ensuring robust borrower evaluation.

Using real-time monitoring and early warning indicators, such as missed payments or sudden changes in account activity, helps spot trouble before it grows. AI-powered analytics can flag at-risk loans, allowing for rapid response.

Liquidity metrics are vital here. For example, banks often track the quick ratio and liquidity to gauge their ability to absorb shocks from rising non-performing loan volumes. By acting early, institutions can prevent minor issues from turning into systemic threats.

Step 2: Loan Restructuring and Forbearance

Once a non-performing loan is identified, restructuring becomes a critical tool. This means negotiating revised payment schedules, reduced interest rates, or temporary payment holidays with borrowers under stress.

Clear regulatory guidance ensures that restructuring is transparent and does not mask true risk. During the COVID-19 crisis, forbearance measures such as payment deferrals helped both banks and borrowers navigate uncertainty.

Balancing support for borrowers with the bank’s long-term health is essential. Effective restructuring can convert a non-performing loan back into a performing asset, stabilizing cash flows and reducing loss severity.

Step 3: Asset Management and Sale of NPLs

When recovery through restructuring is not viable, banks can bundle and sell non-performing loan portfolios to specialized investors or Asset Management Companies (AMCs).

Due diligence and accurate pricing are crucial. Structured approaches, such as using sinking funds in debt management, can help banks gradually build reserves for potential losses from non-performing loan sales.

Securitization, where NPLs are converted into tradable securities, is another method to transfer risk and free up capital. However, avoiding fire sales is key to preserving value and ensuring market stability.

Step 4: Legal Enforcement and Collateral Recovery

Legal enforcement is often the final step for a stubborn non-performing loan. Streamlined foreclosure and insolvency proceedings can significantly shorten recovery times.

Recent legislative changes in the EU, like out-of-court collateral recovery frameworks, are making the process faster and more predictable. Cross-border loans may pose extra challenges, but harmonized laws are reducing friction.

Clear legal pathways boost confidence among investors and banks. Ensuring that collateral can be recovered efficiently makes non-performing loan resolution more attractive and less costly.

Step 5: Strengthening Bank Governance and Internal Controls

Strong governance is the backbone of any non-performing loan management strategy. Banks should have dedicated NPL committees, robust internal controls, and transparent reporting to regulators and stakeholders.

Board oversight ensures accountability and continuous improvement. Training staff on the latest NPL management practices and using technology for internal audits can further reduce risk.

Post-2008 reforms emphasized these points, making them non-negotiable in today’s environment. Well-governed banks are better equipped to handle non-performing loan surges and maintain market trust.

Step 6: Leveraging Technology and Innovation

Technology is transforming how banks manage the non-performing loan lifecycle. Fintech solutions enable real-time monitoring and automated flagging of risky accounts.

Blockchain can facilitate secure loan tracking and transfer, while AI-driven analytics optimize portfolio management. Digital trading platforms for non-performing loan sales, inspired by the EU’s “Amazon-style” model, bring speed and transparency.

By embracing digital innovation, banks can reduce costs, accelerate recovery, and stay ahead in a rapidly evolving market. A tech-forward approach is now a must-have for effective non-performing loan resolution.

Future Outlook: Non-Performing Loans and Financial Stability in 2025

The road ahead for non-performing loan management in 2025 is filled with both challenges and opportunities. As global markets adjust to post-pandemic realities, the stability of financial systems hinges on how well institutions and regulators anticipate upcoming trends, coordinate policies, and strengthen resilience.

Anticipated Trends and Risks

Looking forward, non-performing loan levels are expected to remain a focal point for banks and regulators. The economic rebound from COVID-19 has been uneven, creating pockets of vulnerability in sectors like real estate and small businesses. Inflation and rising interest rates could place additional strain on borrowers, increasing the risk of defaults. Geopolitical instability may also disrupt credit markets. Scenario planning is vital, as the best-case outlook involves steady recovery, while worst-case projections warn of renewed spikes in non-performing loan ratios, particularly in countries with weaker financial infrastructures.

Policy Evolution and International Coordination

International cooperation is more important than ever for non-performing loan resolution. The EU continues to lead with ongoing policy initiatives, including cross-border frameworks and harmonized reporting standards. Lessons from previous crises have shaped new regulatory approaches, encouraging collaboration between the ECB, European Commission, and national authorities. Best practices now emphasize early intervention and transparency, enabling a more unified response to emerging risks. Effective coordination ensures that banks and markets adapt swiftly to changes, minimizing systemic threats from non-performing loan surges.

The Role of Banks, Investors, and Regulators

Banks, investors, and regulators share responsibility for maintaining non-performing loan stability. Banks must adopt proactive risk management and transparent reporting. Investors play a crucial role in secondary NPL markets, helping to absorb distressed assets and inject liquidity. Regulators oversee the entire ecosystem, balancing risk and stability. A real-world example can be seen in the Financial Institutions, Inc. Announces Second Quarter 2025 Results, where the institution's NPL data and management strategies offer insight into current practices and market responses. Collaboration among all parties is essential to contain non-performing loan challenges and support economic growth.

Building Resilient Financial Systems

Future-proofing the financial sector against non-performing loan shocks requires resilience at every level. Banks must integrate NPL management into their risk culture, supported by robust governance and digital transformation. Transparent frameworks and stress testing help prepare for unexpected disruptions. Understanding key metrics, such as the debt-to-equity ratio explained, is crucial for assessing bank health in this context. By combining technology, sound policy, and adaptive strategies, financial systems can withstand shocks and maintain stability even as non-performing loan pressures evolve.

After diving into the complexities of non performing loans and the lessons history offers us, it’s clear that understanding the past is key to navigating the future. Whether you’re an investor, student, or just curious about financial markets, having the tools to explore patterns and stories behind market shifts can give you a real edge. If you want to stay ahead by learning from yesterday’s market moves and today’s challenges, why not get involved with our evolving platform? You can help shape a resource built for insight and discovery—Join Our Beta.