Quick Ratio Guide: Understanding & Using It in 2025

Can your business still pay its bills if cash flow suddenly tightens in 2025? Financial health can shift quickly, making it vital to have reliable tools for monitoring your company’s resilience.

That’s where the quick ratio comes in—it offers a fast, clear snapshot of your business’s liquidity. For business owners, investors, and finance professionals, understanding this metric is more crucial than ever in today’s unpredictable environment.

This guide will break down the quick ratio: what it is, how to calculate it, how to interpret your results, benchmarking, and how to use it for smarter financial decisions in 2025.

You’ll get a complete, actionable roadmap to mastering the quick ratio for modern financial management. We’ll cover the essentials, real-world applications, limitations, and practical tips so you can stay ahead.

What Is the Quick Ratio?

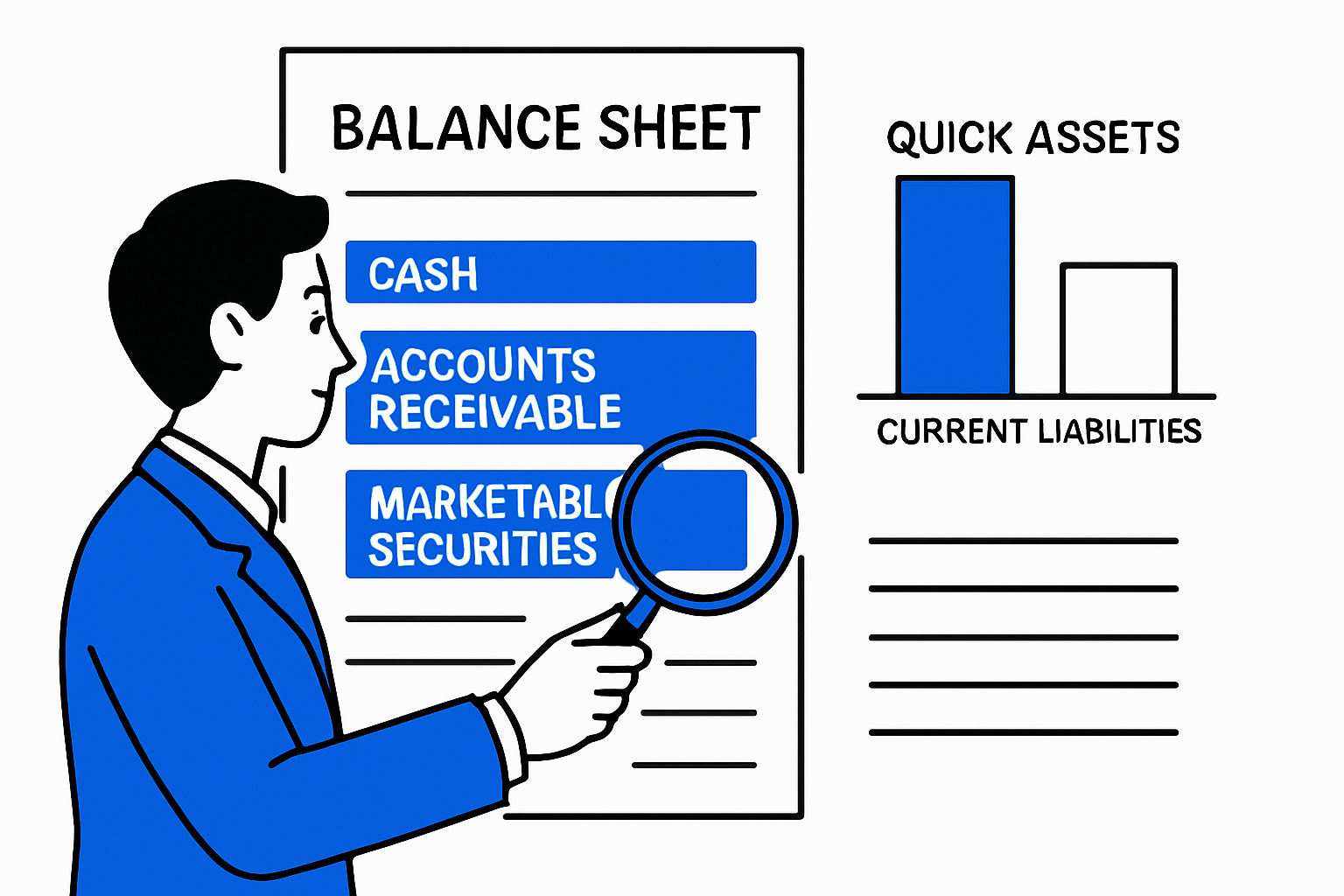

Have you ever wondered how quickly your business could pay its bills if cash flow suddenly got tight? The quick ratio is a financial tool designed to answer that question at a glance. Also known as the acid-test ratio or liquidity ratio, the quick ratio measures a company’s ability to meet its short-term obligations using only its most liquid assets.

Why does this matter? In today’s unpredictable markets, having a clear view of your immediate financial health is crucial. While the current ratio includes all current assets, the quick ratio focuses on assets that can be converted to cash almost immediately. For example, if a company’s quick ratio is 1.2, it means it has $1.20 in liquid assets for every $1.00 of short-term liabilities. This signals to creditors and investors that the business is likely well-prepared for sudden expenses. For a deeper dive into definitions and practical examples, see this Quick Ratio Formula With Examples resource.

Definition and Purpose

The quick ratio is designed to measure how easily a company can meet its short-term debts using assets that are either cash or can be quickly converted to cash. The term “quick” highlights that only the most liquid assets are considered. Unlike the current ratio, which includes inventory and other assets that may take time to sell, the quick ratio excludes anything that might not be immediately available.

This focus on liquidity makes the quick ratio especially useful in times of economic uncertainty. Investors and lenders often check this ratio to gauge whether a business can weather a sudden downturn or cash crunch. For instance, a quick ratio above 1 usually means the company can cover its short-term liabilities without selling inventory or taking on new debt.

Key Components of the Quick Ratio

To calculate the quick ratio, it’s important to know which assets and liabilities are included. Quick assets are:

- Cash and cash equivalents

- Marketable securities (like stocks and bonds)

- Accounts receivable (money owed by customers)

Excluded from the quick ratio are:

- Inventory (can be hard to sell quickly)

- Prepaid expenses (not convertible to cash)

- Fixed assets (like equipment or property)

Current liabilities typically include:

- Accounts payable

- Salaries and wages payable

- Short-term loans and credit lines

- Current portion of long-term debt

- Accrued expenses

Here’s a quick summary:

| Included in Quick Assets | Excluded from Quick Assets |

|---|---|

| Cash | Inventory |

| Marketable Securities | Prepaid Expenses |

| Accounts Receivable | Fixed Assets |

Suppose a company’s balance sheet lists $50,000 in cash, $10,000 in marketable securities, $40,000 in accounts receivable, and $80,000 in current liabilities. Only the first three are used in the quick ratio calculation.

When and Why to Use the Quick Ratio

The quick ratio comes into play whenever you need to assess short-term liquidity. Businesses often review this ratio during internal financial reviews, loan applications, or when preparing for uncertain market conditions. Industries like retail, manufacturing, and services pay close attention to the quick ratio, especially if they operate on tight margins or face seasonal swings.

Lenders and investors look at the quick ratio to judge risk. A strong ratio suggests the business can handle sudden bills or income delays, making it a safer bet for credit or investment. Even if it’s not the only metric considered, the quick ratio offers a fast, reliable snapshot that helps drive smarter financial decisions and supports business continuity planning.

How to Calculate the Quick Ratio (Step-by-Step)

Understanding how to calculate the quick ratio is essential for anyone looking to assess a company’s short-term financial health. This step-by-step guide will walk you through the entire process, from gathering data to interpreting results, so you can confidently evaluate liquidity in 2025.

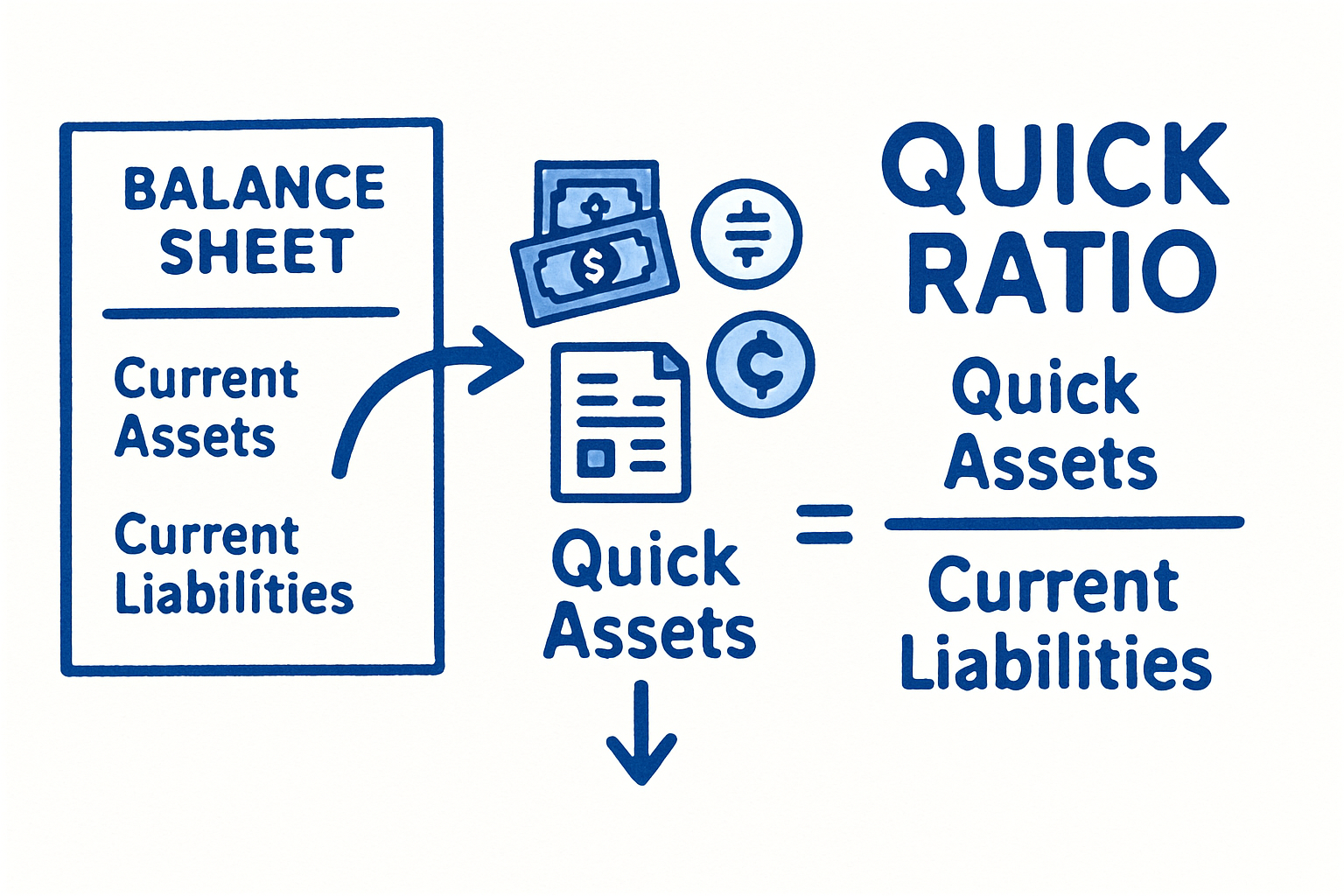

The Quick Ratio Formula

The quick ratio formula is straightforward:

Quick Ratio = (Cash + Marketable Securities + Accounts Receivable) / Current Liabilities

You might also see it called the "acid-test ratio" or "liquidity ratio." Some versions of the formula may include slightly different asset categories, but the goal remains the same: to measure a company's ability to cover its short-term obligations with assets that are quickly convertible to cash.

Example Calculation Table:

| Item | Amount ($) |

|---|---|

| Cash | 30,000 |

| Marketable Securities | 10,000 |

| Accounts Receivable | 25,000 |

| Current Liabilities | 55,000 |

Using the quick ratio formula:

Quick Ratio = (30,000 + 10,000 + 25,000) / 55,000 = 65,000 / 55,000 ≈ 1.18

A quick ratio of 1.18 means the company can cover its short-term debts with its most liquid assets.

Step 1: Gather Financial Statements

The first step in calculating the quick ratio is to collect accurate financial statements, primarily the balance sheet. You'll need up-to-date figures for both assets and liabilities.

Look for data in your accounting software, ERP system, or directly from your company's finance department. Consistency is crucial—make sure all numbers are from the same reporting period.

Common Mistakes to Avoid:

- Mixing data from different periods

- Overlooking off-balance-sheet liabilities

- Including non-quick assets by mistake

Accurate data collection is the foundation for a reliable quick ratio calculation.

Step 2: Identify and Sum Quick Assets

Quick assets are those you can convert to cash within 90 days or less. These include:

- Cash: Physical currency and checking accounts

- Marketable Securities: Stocks, bonds, or other short-term investments

- Accounts Receivable: Money owed by customers, expected soon

Excluded Items:

- Inventory (not always quickly sold)

- Prepaid expenses (can't be used to pay debts)

- Fixed assets (property, equipment)

Sample Quick Assets List:

- Cash: $30,000

- Marketable Securities: $10,000

- Accounts Receivable: $25,000

Add these up to get your total quick assets for the quick ratio formula.

Step 3: Calculate Current Liabilities

Next, sum up all current liabilities—obligations due within a year. These typically include:

- Accounts Payable: Unpaid supplier bills

- Salaries Payable: Wages owed to employees

- Short-Term Loans/Credit Lines: Debt due soon

- Current Portion of Long-Term Debt: Payments due within the year

- Accrued Expenses: Utilities, taxes, or interest incurred but not yet paid

Sample Liabilities List:

- Accounts Payable: $20,000

- Salaries Payable: $5,000

- Credit Line: $10,000

- Current Portion of Long-Term Debt: $15,000

- Accrued Expenses: $5,000

Total current liabilities in this example: $55,000. Accurate liabilities ensure a true quick ratio.

Step 4: Plug Numbers Into the Formula

With your quick assets and current liabilities ready, insert them into the formula. For the sample company:

Quick Ratio = (30,000 + 10,000 + 25,000) / 55,000 = 1.18

This step is where precision counts. Even small errors in asset or liability totals can lead to misleading results. To make things easier, you can use online calculators, such as those featured in Quick Ratio: How to Calculate & Examples, to double-check your math.

Step 5: Interpret the Result

A quick ratio above 1 usually signals strong liquidity, meaning the company can pay its short-term debts with its most liquid assets. A ratio below 1 suggests potential challenges in meeting immediate obligations.

Comparison Example:

- Company A: Quick ratio 0.8 (may struggle to pay debts)

- Company B: Quick ratio 1.5 (ample liquidity and financial flexibility)

Remember, the quick ratio is a snapshot. Use it alongside other metrics for a full financial picture.

Interpreting the Quick Ratio in 2025

Understanding the quick ratio is essential for navigating financial uncertainty in 2025. With economic shifts and evolving industry benchmarks, interpreting this metric correctly can make the difference between proactive management and missed warning signs. Let’s break down what your quick ratio really says about your business health.

What Is a “Good” Quick Ratio?

A “good” quick ratio is often seen as 1.0 or higher. This means a company’s most liquid assets can fully cover its short-term liabilities without selling inventory. According to BDC, a ratio of 1.0 or greater is considered adequate for most businesses. However, context is crucial.

Industry standards play a big role. For example, a tech company with rapid cash flow might have a higher quick ratio than a retailer, which could operate safely at a lower level due to steady inventory turnover. Company size also matters. Smaller firms might target a higher buffer, while large corporations rely on diversified funding.

It’s important to compare your quick ratio to industry benchmarks and peers. For deeper definitions and real-world context, check the Quick Ratio: Definition, Formula and Usage guide. Ultimately, a “good” quick ratio is one that fits your sector, business model, and risk tolerance.

What a High or Low Quick Ratio Means

A high quick ratio signals strong liquidity. This means your business can meet its short-term debts with ease, reassuring creditors and investors. The upside: financial safety and flexibility to seize opportunities. However, holding excess liquid assets can suggest underutilized resources that could otherwise fuel growth.

A low quick ratio, below 1.0, tells a different story. It may signal a potential cash crunch, where obligations could outpace available assets. Yet, low isn’t always bad. Seasonal businesses or those in rapid expansion may temporarily dip below the norm while investing in future gains.

Here’s a quick comparison:

| Quick Ratio | What It Means | Possible Implications |

|---|---|---|

| Above 1.0 | Strong liquidity | Safety, but maybe idle cash |

| Around 1.0 | Adequate, balanced | Meets obligations |

| Below 1.0 | Potential shortfall | Risk, but context matters |

Always view your quick ratio alongside business cycles and growth phases.

Red Flags and Positive Signals

Trends in your quick ratio can reveal a lot about your financial health. A declining ratio over several quarters is a red flag, especially if it drops below industry standards. Sudden drops may indicate operational setbacks or unexpected expenses. Persistent ratios under 1.0 could signal trouble accessing credit or paying suppliers.

On the flip side, an improving or consistently strong quick ratio is a positive sign. If your ratio steadily climbs above 1.0 or outperforms peers, it reflects better receivables management or stronger cash reserves. For instance, a company that streamlined collections and delayed payables saw its quick ratio rise from 0.8 to 1.3, leading to improved supplier terms and easier loan approvals.

Monitor patterns, not just single data points. It’s the trend that often tells the real story.

Limitations of the Quick Ratio

While the quick ratio is a valuable snapshot, it’s not a complete picture. Not all quick assets are equally liquid—accounts receivable can become “slow” if customers delay payments. One-off events or accounting changes can distort the ratio, masking real risks or improvements.

The quick ratio is best used alongside other metrics, such as the current ratio and cash flow analysis, for a thorough view. Financial institutions may not rely on the quick ratio alone, but it remains a key tool for early warning and ongoing monitoring.

In 2025, use the quick ratio as part of a broader toolkit. Combine it with qualitative insights and industry benchmarks to make well-rounded financial decisions.

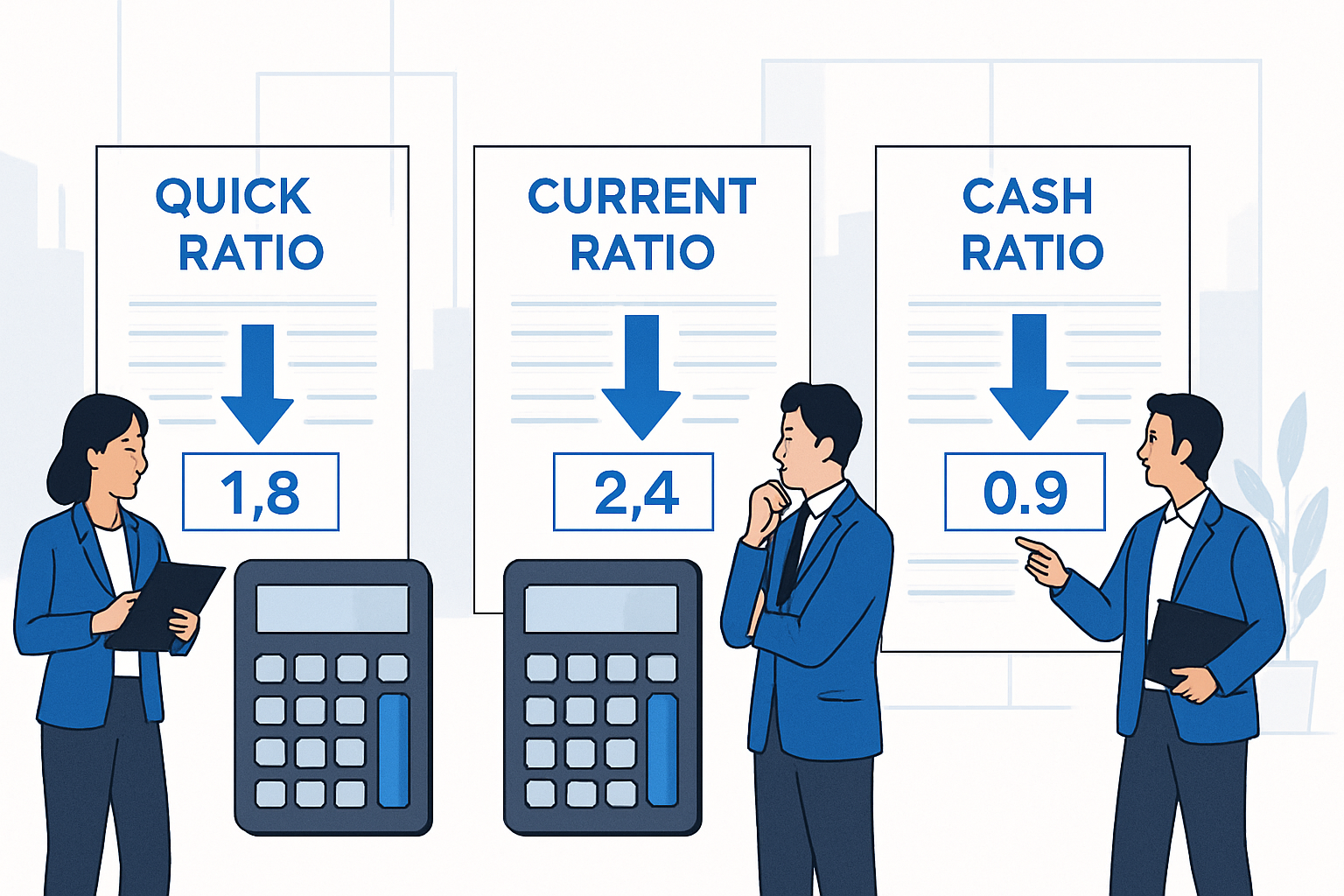

Quick Ratio vs. Other Liquidity Ratios

Understanding how the quick ratio stacks up against other liquidity ratios is essential for anyone making financial decisions in 2025. Each ratio offers a unique lens on a company's short-term financial strength, and knowing their differences helps you pick the right tool for your analysis.

Quick Ratio vs. Current Ratio

The quick ratio and current ratio are both designed to measure a company's liquidity, but they approach it differently. The current ratio includes all current assets—such as cash, accounts receivable, and inventory—divided by current liabilities. In contrast, the quick ratio focuses only on the most liquid assets, excluding inventory and prepaid expenses.

For example, imagine a company with $50,000 in cash, $30,000 in accounts receivable, $20,000 in inventory, and $60,000 in current liabilities. The current ratio would be ($50,000 + $30,000 + $20,000) / $60,000 = 1.67. The quick ratio, excluding inventory, is ($50,000 + $30,000) / $60,000 = 1.33.

The quick ratio offers a stricter view of liquidity, making it especially valuable in industries where inventory may not be easily converted to cash. For precise definitions of these ratios, see this Financial terms glossary.

Quick Ratio vs. Cash Ratio

The cash ratio goes a step further in conservatism by considering only cash and cash equivalents as assets, ignoring accounts receivable. This makes it the most stringent measure of a company's ability to cover short-term obligations.

Using the previous example, if the company has $50,000 in cash and $60,000 in current liabilities, the cash ratio is $50,000 / $60,000 = 0.83. This is much lower than the quick ratio, which signals a more cautious approach.

While the cash ratio is useful during periods of high uncertainty or when rapid payment is critical, it can underestimate liquidity for businesses with reliable receivables. The quick ratio remains a balanced measure for most scenarios, capturing both immediate cash and near-cash assets.

Choosing the Right Ratio for Your Needs

Selecting the best liquidity metric depends on your business goals, industry, and the financial questions you're trying to answer. The quick ratio is widely used because it balances caution and practicality, offering a clear view of which assets can quickly cover liabilities.

For industries like retail, where inventory turnover is fast, the current ratio might suffice. In sectors with slower inventory movement, the quick ratio provides a more accurate snapshot. The cash ratio is best for highly risk-averse environments or for short-term lenders.

Here's a quick table to summarize the differences:

| Ratio | Includes Inventory? | Includes Receivables? | Most Conservative? |

|---|---|---|---|

| Current Ratio | Yes | Yes | No |

| Quick Ratio | No | Yes | Moderate |

| Cash Ratio | No | No | Yes |

Ultimately, combining the quick ratio with other liquidity ratios creates a more complete financial picture. This approach mirrors industry best practices, ensuring you don't miss critical signals about your company's short-term financial health.

Using the Quick Ratio for Smarter Financial Decisions in 2025

Is your business ready to make sharper, faster financial calls in 2025? The quick ratio is a powerful tool for gaining clarity on liquidity and making those smart decisions. Let’s see how you can put this ratio to work across management, investment, benchmarking, and improvement efforts.

Applying the Quick Ratio in Business Management

Managers use the quick ratio as a central checkpoint for financial health. By integrating it into monthly dashboards, you can flag liquidity shifts before they become problems. Setting internal targets—like maintaining a quick ratio above 1.0—helps teams act fast if liquidity dips.

Consider reviewing the quick ratio alongside other metrics. This way, you spot trends, seasonality, or sudden changes. For example, a drop in the quick ratio after a large customer payment delay could prompt closer receivables follow-up.

Regular monitoring empowers proactive, not reactive, decisions. It also makes it easier to set policies for minimum cash reserves or trigger cost controls when the quick ratio falls below a pre-set threshold.

For Investors and Lenders

External stakeholders like investors and lenders lean on the quick ratio to gauge a business’s short-term financial strength. When reviewing a loan application, a lender will often check if the quick ratio meets internal minimums, especially during uncertain economic times.

In 2025, many lenders are tightening standards, making liquidity metrics more important. Investors also use the quick ratio to compare potential investments, weighing liquidity risks against growth opportunities.

A high quick ratio can help secure better loan terms or attract new investors. Conversely, a low quick ratio may prompt questions about risk management, even if other fundamentals look strong. For a deep dive, see Quick Ratio: Definition, Formula, Uses.

Benchmarking and Industry Comparisons

Comparing your quick ratio to industry peers is essential for context. Industry averages are available from trade groups, financial databases, and public company filings.

Here’s a quick guide to benchmarking:

- Check trade association reports for sector-specific norms.

- Use tools like BDC’s quick ratio calculator for quick comparisons.

- Review financial statements of public companies in your niche.

For example, a retailer might benchmark against the average quick ratio for their sector, while a tech firm would look for different standards. This comparison helps you set realistic targets and spot competitive strengths or weaknesses.

Improving Your Quick Ratio

If your quick ratio needs a boost, several strategies can help. Start by accelerating collections on accounts receivable—offering early payment discounts or tightening credit terms.

Additional ways to improve the quick ratio:

- Delay non-essential payments to vendors when possible.

- Increase cash reserves during strong sales periods.

- Control expenses and avoid overstocking inventory.

A real-world example: A manufacturing business improved its quick ratio from 0.9 to 1.3 in six months by focusing on receivables and renegotiating payment terms with suppliers. These small shifts made a big impact on liquidity and confidence with lenders.

Common Pitfalls and How to Avoid Them

While the quick ratio is a useful signal, it’s not foolproof. Relying on it alone can lead to blind spots.

Common mistakes include:

- Ignoring seasonality, which can temporarily distort the quick ratio.

- Misclassifying assets or liabilities, resulting in inaccurate calculations.

- Overlooking slow-paying receivables, which may not be so “quick” in reality.

To avoid these pitfalls, always use the quick ratio in combination with other financial ratios and review trends over time, not just single snapshots.

Quick Ratio Trends and Insights for 2025

Looking ahead, economic shifts like inflation and supply chain disruptions are impacting liquidity across industries. In 2025, best practices include more frequent quick ratio reviews and scenario planning for cash flow shocks.

Many businesses are adopting real-time financial dashboards to monitor the quick ratio and related metrics. This helps spot risks early and supports agile decision-making.

Staying informed about industry trends and regularly benchmarking your quick ratio are key steps for business resilience. Smart use of this ratio can mean the difference between weathering a crisis and facing a cash crunch.

Real-World Examples and Case Studies

Real-world scenarios bring the quick ratio to life, showing how it works beyond theory. Whether you’re analyzing financial statements or making major business decisions, these case studies illustrate the quick ratio’s value in action.

Example 1: Quick Ratio Calculation Walkthrough

Let’s start with a practical quick ratio example. Imagine Company X’s balance sheet lists $40,000 in cash, $20,000 in marketable securities, and $60,000 in accounts receivable. Their current liabilities total $100,000.

Apply the formula:

Quick Ratio = (Cash + Marketable Securities + Accounts Receivable) / Current Liabilities

Quick Ratio = ($40,000 + $20,000 + $60,000) / $100,000 = $120,000 / $100,000 = 1.2

A quick ratio of 1.2 means Company X can cover its current debts with its most liquid assets and still have some cushion. This calculation gives a clear, fast check on liquidity.

Example 2: Quick Ratio in Action—Business Turnaround

Now, consider a retailer facing a tight cash crunch. With a quick ratio of just 0.7, the business struggled to pay suppliers on time. Management acted fast: they chased overdue receivables, negotiated longer payment terms, and sold off unused equipment to boost cash.

Within six months, their quick ratio improved to 1.1. This not only restored supplier confidence but also attracted a new investor. The quick ratio was central to the turnaround, guiding urgent decisions and signaling improved financial health.

Example 3: Quick Ratio Red Flags—What Went Wrong

Not all quick ratio stories have a happy ending. A manufacturing firm saw its quick ratio drop from 1.3 to 0.6 in a single quarter. The cause? Customers delayed payments, and the company increased short-term borrowing to cover expenses.

This downward trend was a red flag for lenders. The firm faced tougher credit terms and had to implement strict cash controls. Monitoring the quick ratio flagged the problem early, but ignoring the warning signs led to serious consequences.

Quick Ratio Calculator Tools

Calculating the quick ratio is easier than ever with online tools. These calculators let you enter your company’s key numbers and instantly get your ratio. Many business owners use them for monthly checkups or when preparing for loans.

For those who want to explore more financial metrics, you can find helpful resources and calculators among All finance-related posts. These tools streamline analysis, though you should always double-check inputs for accuracy.

Frequently Asked Questions About the Quick Ratio

Have questions about the quick ratio? You’re not alone. Here are answers to the most common queries business owners and finance professionals face today.

What is the difference between the quick ratio and the acid-test ratio?

The quick ratio and acid-test ratio are actually the same thing. Both terms describe the same financial metric. Some sources prefer “acid-test” because it emphasizes the idea of a fast, stringent test of liquidity. If you see either term, know they refer to the same calculation. For more background on how financial experts discuss the quick ratio, check out the About Historic Financial News page.

How often should businesses calculate their quick ratio?

It’s wise to check your quick ratio at least every quarter, especially if your cash flow fluctuates. Many companies include it in monthly financial reviews. More frequent checks can help spot liquidity issues before they become problems.

Can the quick ratio be negative, and what does that mean?

Yes, the quick ratio can be negative if your quick assets total less than zero, or if liabilities vastly outweigh assets. A negative ratio is a serious red flag. It means your company may not be able to cover short-term obligations, signaling urgent financial risk.

How do you handle doubtful accounts in receivables for the quick ratio?

When calculating the quick ratio, subtract any doubtful or uncollectible accounts from accounts receivable. Only include amounts you genuinely expect to collect. This gives a more accurate measure of your liquidity.

Is a high quick ratio always good?

Not necessarily. While a high quick ratio (above 1) shows strong liquidity, an excessively high number may mean your company is holding too much idle cash or not investing in growth. Balance is key; context and industry norms matter.

What are the most common mistakes in calculating the quick ratio?

Common errors include incorrectly including inventory or prepaid expenses as quick assets, or missing certain current liabilities. Double-check your balance sheet categories to ensure accuracy.

How do economic changes in 2025 affect the reliability of the quick ratio?

Economic trends like inflation or supply chain disruptions can impact receivables and payables, making the quick ratio more volatile. Always interpret results in light of current market conditions and use other ratios for a fuller picture.

Should startups and small businesses use the quick ratio differently than large corporations?

Startups and small businesses may see more fluctuation in their quick ratio due to cash flow swings or seasonal sales. It’s important for these companies to monitor the ratio closely and use it alongside other financial health metrics. If you need tailored advice, don’t hesitate to contact financial experts for help.

Now that you’ve got a solid grip on the quick ratio and how it shapes smarter financial decisions for 2025, imagine having the power to explore these concepts through real historical market stories and interactive tools. We’re building a platform designed for curious minds like yours—investors, students, and anyone wanting to connect the dots between past market movements and today’s trends. If you want to dive deeper, spot patterns, and test your knowledge with AI-powered insights, I’d love for you to Join Our Beta. Your perspective could help shape the future of financial learning!