Sinking Fund Guide: How To Start In 2025

Picture this: your car breaks down or a surprise holiday expense pops up, but you feel calm and prepared. No panic. No credit card scramble.

That’s the power of a sinking fund. In this guide, you’ll discover exactly how to use this smart savings strategy, step by step, to handle any financial surprise in 2025.

We’ll break down what sinking funds are, why they matter now more than ever, how to set them up, proven best practices, advanced techniques, and the most common mistakes to avoid. Ready to take control of your money this year?

What Is a Sinking Fund?

Imagine facing a big bill—like car insurance or holiday gifts—without stress. That’s the power of a sinking fund. But what exactly is this financial tool, and why is it gaining popularity among budget-savvy individuals?

Definition and Core Concept

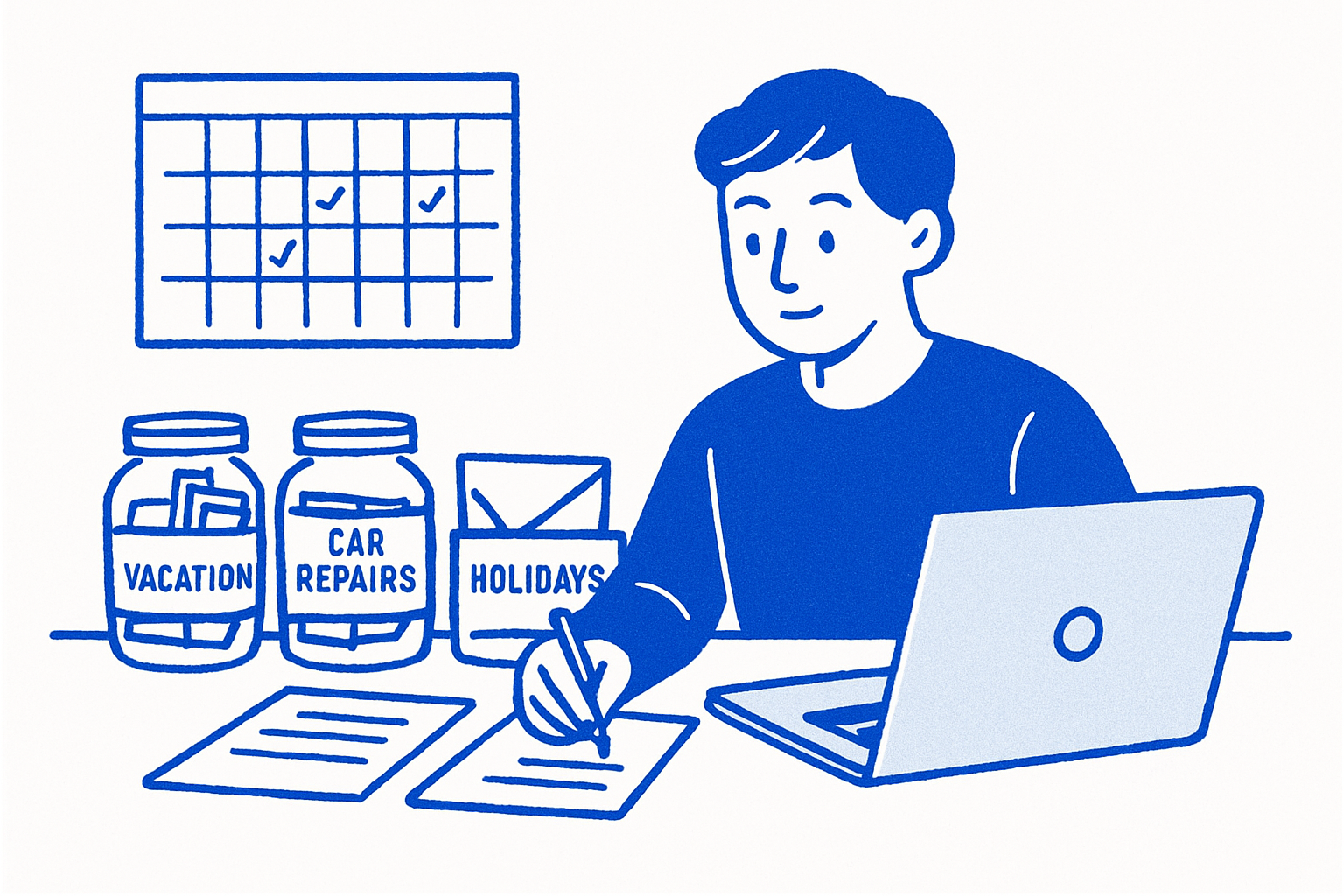

A sinking fund is a targeted savings strategy designed for planned, irregular, or larger expenses. Unlike a general savings account or emergency fund, a sinking fund is all about preparing for costs you know are coming. These are not surprise emergencies but predictable expenses that can disrupt your budget if unplanned.

Historically, sinking funds started as a way for governments and companies to repay bonds over time. Today, they’ve evolved into powerful personal finance tools for everyday people. By setting aside small amounts regularly, you break a big financial hurdle into manageable steps.

For example, let’s say your car insurance is due once a year and costs $600. By saving $50 a month in a dedicated sinking fund, you’re ready when the bill arrives—no scrambling or last-minute credit card use. In fact, 60% of Americans feel financial stress due to irregular expenses, according to CNBC, making this approach more relevant than ever. If you’re curious about more detailed applications and examples, check out this Sinking Funds Help Handle Expenses, Avoid Debt resource for a deeper dive.

Common Types of Sinking Funds

Sinking funds can be customized to fit nearly any financial goal. Some of the most common types include:

- Vacations and travel

- Home repairs or improvements

- Car maintenance and registration

- Back-to-school shopping

- Insurance premiums

You can also tailor a sinking fund for personal milestones, like weddings, tech upgrades, or property taxes. Some people use short-term sinking funds for things needed within a year, while others plan long-term for expenses several years away.

Sinking funds are especially helpful for avoiding debt. Households that use them report 30% fewer overdraft fees, according to Ramsey Solutions. Instead of relying on credit cards or loans, you pay cash for large purchases, giving you more control and peace of mind.

Benefits of Using Sinking Funds

The advantages of a sinking fund go far beyond financial organization. First, it reduces anxiety by giving you the confidence that you can handle big expenses. You’re less likely to be caught off guard, which means fewer “budget busters.”

A sinking fund encourages disciplined, goal-oriented savings. You set a target, contribute regularly, and watch your progress. This habit makes you a smarter spender, helping you prioritize what truly matters.

Perhaps most importantly, sinking funds prevent unplanned debt. For instance, using a sinking fund for holiday shopping means you won’t face a credit card shock in January. Instead, you can enjoy your purchases, knowing you planned ahead and stayed in control.

Why Sinking Funds Matter in 2025

The financial world is changing fast. If you want to stay ahead in 2025, understanding the value of a sinking fund is more important than ever. With costs rising and life feeling less predictable, planning for irregular expenses is no longer optional—it's essential.

The 2025 Financial Landscape

Inflation is expected to keep pushing prices higher in 2025. Everyday essentials, from groceries to utilities, will likely cost more. The job market is also shifting, with many people facing uncertainty about their income or work stability.

Big-ticket expenses are popping up more often, too. Cars are lasting longer, but repairs are pricier. If you own a home, surprise maintenance bills can hit hard. Family events—graduations, weddings, or new babies—add to the list of irregular costs.

A recent CNBC report found that 1 in 3 Americans expects a major irregular expense in 2025. Without a sinking fund, these surprises can catch you off guard. By setting up dedicated savings ahead of time, you can face the year’s financial curveballs with confidence.

Sinking Funds vs. Other Savings Methods

You might wonder how a sinking fund fits with other ways of saving. While an emergency fund is vital for true crises, a sinking fund is designed for expenses you can plan for. Think of it as a safety net for the predictable but irregular moments in life.

Many people rely on credit cards or "buy now, pay later" plans to cover big purchases. This often leads to debt and high interest charges. By contrast, a sinking fund lets you save gradually, so you don’t have to scramble or borrow at the last minute.

Consider this comparison:

| Expense | Sinking Fund | Credit Card | Emergency Fund |

|---|---|---|---|

| Annual Insurance | ✔️ | ❌ | ❌ |

| Car Repairs | ✔️ | ❌ | Sometimes |

| Medical Bills | ❌ | ✔️ | ✔️ |

Paying $1,200 for a new appliance from your sinking fund is far less stressful than racking up credit card debt. For more on how this strategy can help you avoid debt, check out How Sinking Funds Can Help You Avoid Debt.

Real-Life Impact and Success Stories

Sinking funds make a real difference in people’s lives. Take the example of a family who set up separate funds for a summer vacation and home repairs. When their roof started leaking, they had the money ready—no loans, no panic. Later, they enjoyed a debt-free getaway, knowing they’d planned every dollar.

Financial experts like Dave Ramsey and many personal finance bloggers recommend sinking funds for anyone who wants to get ahead. According to Ramsey Solutions, 70% of successful budgeters use a sinking fund system to handle irregular expenses.

The emotional benefits are just as powerful. People who use sinking funds report less stress, fewer arguments about money, and a greater sense of control. In a world where financial surprises are becoming the norm, this simple habit can bring real peace of mind.

Step-by-Step: How to Start a Sinking Fund in 2025

Starting a sinking fund in 2025 can transform how you handle big expenses. Whether you want to avoid financial stress or simply take control of your money, following these six practical steps will set you up for success. Let’s dive into the process, making every dollar work for your goals.

Step 1: Identify Upcoming Expenses and Goals

Begin your sinking fund journey by brainstorming all irregular or large expenses you expect in the next year. Review past bank statements, credit card bills, and digital receipts to spot annual or quarterly costs that tend to sneak up on you. Common examples include car registration, insurance premiums, holiday gifts, back-to-school shopping, and travel.

Don’t overlook life events—think birthdays, weddings, graduations, or even tech upgrades. If you’re a homeowner, add property taxes or home repairs to your list. Parents might need a fund for school supplies or extracurricular activities.

Use digital budgeting apps, spreadsheets, or printable planners to track these categories. Some people find color-coding or labeling helpful for visual organization. Regularly update your list as new goals or expenses arise.

If you want a deeper dive into integrating sinking funds with your budget, check out Sinking Funds Explained: A Beginner's Guide to Getting Started for practical tips and examples.

By proactively identifying your targets, you’ll lay a solid foundation for a stress-free financial year. The sinking fund keyword appears twice in this critical first step.

Step 2: Calculate How Much You Need

Next, estimate the total amount required for each sinking fund category. Look at previous years’ expenses and factor in any expected price increases for 2025. For example, if you spent $600 on holiday gifts last year and expect higher prices, aim for $650 or $700 this year.

Set realistic, specific savings targets for each fund. Don’t forget to pad your estimates a bit—unexpected costs can pop up. If you’re unsure, it’s better to overestimate than scramble later.

Make a clear list or table of your goals, such as:

| Expense | Target Amount |

|---|---|

| Car Maintenance | $800 |

| Vacation | $1,200 |

| Insurance Premiums | $900 |

| Holiday Gifts | $700 |

This approach ensures each sinking fund is tailored to your real needs. Planning ahead helps prevent last-minute panic and keeps your finances on track.

Step 3: Set a Savings Timeline and Break Down Monthly Contributions

Once you know your targets, set a timeline for each sinking fund. Divide the total needed by the number of months until you’ll make the purchase or payment.

For example, if you need $600 for holiday gifts by December and it’s January, divide $600 by 12 months to save $50 per month. If your car registration is due in six months and costs $300, that’s $50 per month as well.

Use calendar reminders or app notifications to keep yourself accountable. Automating these monthly transfers is a smart move—according to CNBC, automated savings can boost your success rate by 40 percent.

Breaking down your sinking fund goals into manageable monthly amounts makes saving feel less overwhelming and much more achievable.

Step 4: Choose the Right Savings Account(s)

Selecting where to keep your sinking fund is crucial. You have several options:

- Separate savings accounts at your bank for each goal

- Sub-accounts or “buckets” within a single account (many digital banks offer this)

- Cash envelopes for those who prefer physical money

- Budgeting apps that allow you to label and track different funds

Each method has pros and cons. High-yield savings accounts are great for larger, long-term sinking funds, as they offer better interest rates. Keeping funds in labeled sub-accounts or digital “jars” helps reduce the temptation to dip into them for unrelated expenses.

Choose a system you’ll actually use. The right setup will make your sinking fund feel organized and separate from everyday spending.

Step 5: Track Progress and Adjust as Needed

Consistent tracking is key to effective sinking fund management. Check your balances regularly—monthly or even weekly—using apps, spreadsheets, or visual trackers. Seeing your progress can be motivating.

If you receive a bonus, tax refund, or extra income, consider boosting your sinking fund contributions. Likewise, if your expenses change, adjust your monthly savings to stay on target.

Stay flexible. Life can throw curveballs, so be ready to reallocate funds or update your goals as needed. Regular check-ins ensure your sinking fund remains aligned with your priorities. Making adjustments isn’t a setback—it’s a sign of proactive financial management.

Step 6: Spend from Your Sinking Fund with Confidence

When it’s time to pay for a planned expense, use your sinking fund knowing you’ve prepared for this moment. Transfer the money to your checking account or pay directly from your designated savings if your bank allows.

Celebrate your success—whether it’s a debt-free family vacation, a new appliance, or stress-free holiday shopping. Each time you use your sinking fund as intended, you reinforce positive money habits and reduce financial anxiety.

Remember, the goal is to make big expenses feel routine, not scary. By sticking to your plan, you’ll gain more control, peace of mind, and confidence in your financial future.

Best Practices for Managing Multiple Sinking Funds

Managing multiple sinking fund accounts doesn’t have to be overwhelming. With the right structure, you can keep your savings organized, on track, and working toward your goals. Let’s break down the best ways to make your sinking fund system easy and effective.

Organizing and Labeling Funds

Start by giving each sinking fund a clear, specific label. Use names like “Car Repairs,” “Holidays,” or “Back to School” so you always know what each pool of money is for.

Color-coded spreadsheets or categories in your banking app can help you spot each sinking fund at a glance. Many digital banks now let you create multiple sub-accounts for this exact purpose.

If you want more inspiration or additional strategies, you can browse all personal finance posts for fresh ideas on organizing your sinking fund setup.

Prioritizing and Funding Multiple Goals

Not all sinking fund goals are equally urgent. Rank your funds by importance—some, like property taxes or insurance, are non-negotiable, while others, such as vacations, can be flexible.

Allocate more money to essential sinking fund categories first. For example, if you have three or more sinking funds, data shows that 80% of users report improved financial control. Prioritization keeps your most important goals funded, even when your budget is tight.

Automating and Streamlining Savings

Automation is your best friend when it comes to sinking fund success. Set up automatic transfers for each fund, so you never forget a contribution.

Budgeting apps like EveryDollar or YNAB let you visualize progress and set reminders. Many banks even allow you to nickname and separate each sinking fund, making tracking seamless.

By automating, you reduce the risk of missing a month or dipping into funds meant for other goals.

Reviewing and Adjusting Regularly

Life changes and so do your priorities. Schedule monthly or quarterly check-ins to review each sinking fund’s balance and progress.

When you meet a goal, reallocate those funds to your next priority. Adjust your contributions if you receive a windfall or face a new expense. Regular reviews help prevent underfunding and keep your sinking fund system aligned with your life.

Avoiding Common Pitfalls

Don’t borrow from one sinking fund to cover another expense. This can unravel your progress and create confusion.

Avoid overcomplicating your setup with too many small funds. If you notice overlap, combine similar goals—such as merging all annual subscriptions into one sinking fund. Keep your system simple and easy to maintain to ensure long-term success.

Advanced Sinking Fund Strategies for 2025

Ready to take your sinking fund to the next level? As 2025 brings new financial challenges, advanced strategies can help you maximize your savings, grow your balances, and stay ahead of big expenses. Let’s dive into smarter ways to make your sinking fund work harder for you.

Maximizing Interest and Growth

Don’t let your sinking fund sit idle. Place larger balances in high-yield savings or money market accounts to earn more interest over time. Even a small bump in your interest rate can add up on big goals, like home repairs or property taxes.

Compare options carefully:

- High-yield savings: Best for easy access and competitive rates.

- Money market accounts: Often higher rates, some check-writing ability.

- Digital banks: Frequently offer sub-accounts for each sinking fund.

For a deeper dive into optimizing your approach, check out Sinking Funds: How to Plan Ahead and Save Smarter.

Integrating Sinking Funds with Your Budget

Treat each sinking fund contribution as a fixed monthly “expense” in your budget. Zero-based or envelope budgeting works especially well, as you assign every dollar a job—including future expenses.

Try these steps:

- Add each sinking fund to your budget spreadsheet or app.

- Automate transfers on payday.

- Review monthly to adjust for any new expenses.

This method creates consistency and makes it easier to avoid overspending.

Handling Variable Income or Irregular Expenses

If your income fluctuates, your sinking fund strategy needs flexibility. Freelancers and commission-based workers can front-load contributions after high-earning months, or adjust targets seasonally.

Tips for managing variable income:

- Calculate average monthly income and base contributions on that.

- Increase sinking fund deposits after large payments.

- Pause or reduce contributions during lean months, then catch up when possible.

This keeps your savings goals on track, even when paychecks aren’t predictable.

Combining Sinking Funds with Other Savings Goals

Balance your sinking fund priorities with emergency, retirement, and investment savings. Windfalls, like tax refunds or bonuses, are perfect for boosting both sinking funds and long-term goals.

Consider this approach:

- Allocate a percentage of any windfall to each savings goal.

- Use a table to track progress and keep goals visible.

- Reassess priorities annually to align with life changes.

This well-rounded strategy supports short-term needs and future security.

Planning for Major Life Events

Major milestones demand extra sinking fund planning. Weddings, a new baby, or moving require early, steady saving. Start by setting a realistic total for the event, then break it into monthly contributions.

Action steps:

- Identify the event timeline and costs.

- Open a dedicated sinking fund account.

- Adjust monthly savings as details become clearer.

Early planning means less stress and more confidence when big moments arrive.

Common Mistakes and How to Avoid Them

Even the most diligent savers can make mistakes with a sinking fund. Recognizing these common pitfalls—and knowing how to sidestep them—can make your savings journey smoother and more effective.

Underestimating Expenses or Timelines

One of the biggest errors is underestimating how much you’ll need or when you’ll need it. If your sinking fund doesn’t cover every cost or you start saving too late, you’ll scramble when the bill arrives.

- Review past years’ expenses for hidden costs.

- Start your sinking fund as early as possible.

- Overestimate to provide a buffer for surprises.

For example, don’t forget annual subscriptions or school fees—these often catch people off guard. By starting early and planning thoroughly, you can avoid falling short.

Mixing Sinking Funds with Emergency Savings

Another common mistake is using your emergency fund for planned expenses. Although both are savings, their purposes are different. Your sinking fund should handle predictable costs, while emergency savings are for true surprises.

- Keep accounts separate and clearly labeled.

- Avoid “raiding” your emergency stash for non-emergencies.

- Review the Financial terminology explained page if you’re unsure about these terms.

Data shows that 50% of budgeters admit to dipping into emergency funds for non-emergencies, which can leave you exposed when real crises hit.

Not Adjusting for Life Changes

Life never stands still, and neither should your sinking fund contributions. Failing to increase savings after a raise, a new expense, or a major life event can leave you unprepared.

- Schedule regular reviews of your sinking fund goals.

- Adjust contributions any time your circumstances change.

- Add new categories as your needs evolve.

For instance, if you adopt a pet, start a “pet fund” right away to cover future vet visits and supplies.

Lack of Consistency or Discipline

Skipping monthly contributions or dipping into your sinking fund early weakens its power. Consistency is key for success.

- Automate transfers to your sinking fund whenever possible.

- Set clear rules about when you can use the money.

- Use reminders and visual trackers to stay motivated.

Sticking to your plan ensures your sinking fund is ready when you need it most.

Overcomplicating the System

It’s tempting to create a sinking fund for every tiny goal, but too many categories can get confusing. When your system is too complex, it’s hard to manage and track progress.

- Consolidate similar goals into broader categories.

- Use simple tracking tools or budgeting apps.

- Focus on the most important sinking fund goals.

For example, instead of separate funds for each streaming service, combine them into one “annual subscriptions” fund for simplicity.

You’ve just learned how sinking funds can give you peace of mind and real control over your finances in 2025—but there’s so much more to discover when you put your plans in a bigger context. If you’re curious about how financial strategies like this have shaped market trends, or you want to spot patterns that can help guide your money moves, why not take the next step? I invite you to Join Our Beta and explore the stories behind market movements with us. Your journey to smarter saving (and investing!) starts here.