Net Profit Margin: A Historical Financial Metric Explained

Understanding profitability metrics has been essential to business success throughout financial history. Among the various measures investors and analysts employ, net profit margin stands as one of the most revealing indicators of a company's financial health and operational efficiency. This metric has guided investment decisions through bull markets and bear markets alike, providing crucial insights into how effectively businesses convert revenue into actual profit. Whether you're analyzing the robust margins of technology giants in the 1990s or examining the compressed margins during the 2008 financial crisis, this fundamental ratio offers a window into corporate performance that transcends time periods and economic cycles.

Understanding the Net Profit Margin Formula

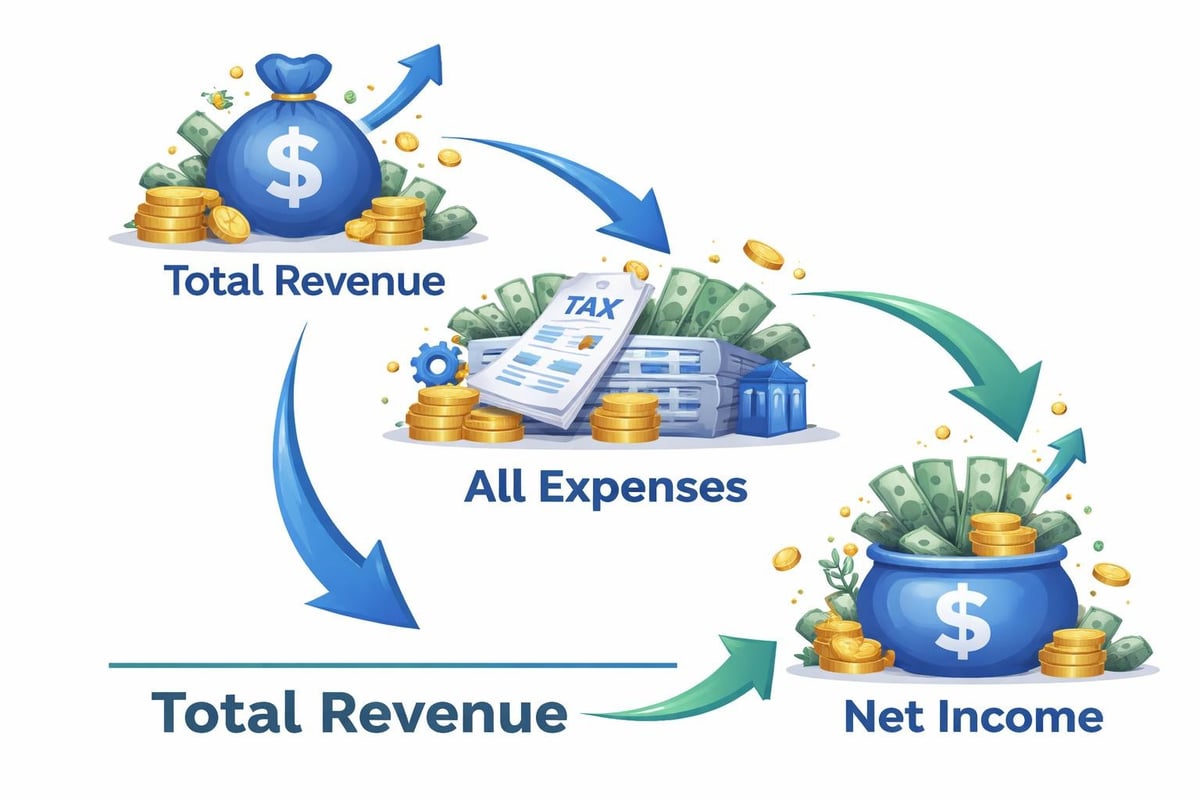

The net profit margin represents the percentage of revenue that remains as profit after all expenses, taxes, and costs have been deducted. The calculation itself is straightforward: divide net income by total revenue, then multiply by 100 to express the result as a percentage. This simple formula reveals how many cents of profit a company generates for each dollar of revenue earned.

The basic formula looks like this:

- Net Profit Margin = (Net Income ÷ Total Revenue) × 100

For example, if a company generated $10 million in revenue and posted $1.2 million in net income, the net profit margin would be 12%. This means that for every dollar of sales, the company retained twelve cents as profit after covering all operating expenses, interest payments, taxes, and other costs.

Historical analysis reveals that net profit margin calculations have remained consistent, but what constitutes a "good" margin has varied significantly across industries and time periods. During the post-World War II manufacturing boom, margins looked vastly different from the service-oriented economy of the 21st century.

Components That Impact Net Profit Margin

Several elements influence this profitability metric beyond simple revenue and expenses. Understanding these components helps explain why margins fluctuate across quarters, years, and economic cycles.

Key factors include:

- Cost of goods sold (COGS): Direct costs of producing products or services

- Operating expenses: Administrative costs, salaries, marketing, and overhead

- Interest expenses: Debt servicing costs that reduce net income

- Tax obligations: Corporate tax rates that vary by jurisdiction and time period

- One-time charges: Restructuring costs, asset write-downs, or extraordinary items

The relationship between these elements and operating margin provides additional context for financial analysis. While operating margin focuses on operational efficiency before interest and taxes, net profit margin captures the complete financial picture.

Historical Perspective on Industry Margins

Examining net profit margin through a historical lens reveals fascinating patterns across different sectors and economic eras. The Business Development Bank of Canada's analysis demonstrates how this metric serves as a critical barometer for business health across diverse industries.

During the technology boom of the late 1990s, software companies demonstrated extraordinary margins as their scalable business models produced high profitability. Conversely, traditional retail businesses operated on razor-thin margins, often below 5%, as they balanced competitive pricing with substantial overhead costs.

| Era | High-Margin Industries | Typical Range | Low-Margin Industries | Typical Range |

|---|---|---|---|---|

| 1980s | Pharmaceuticals, Software | 15-25% | Grocery Retail, Airlines | 1-3% |

| 1990s | Technology, Consulting | 18-30% | Manufacturing, Hospitality | 3-6% |

| 2000s | Financial Services, Tech | 12-22% | Automotive, Retail | 2-5% |

| 2010s | SaaS, Biotechnology | 20-35% | Food Service, Transportation | 2-4% |

| 2020s | Cloud Computing, Pharma | 18-28% | Traditional Retail, Energy | 3-7% |

The analysis of profit margins by industry shows how sector-specific characteristics create predictable margin patterns. Capital-intensive industries like manufacturing historically maintain lower margins due to substantial equipment investments and ongoing maintenance costs.

Margin Evolution During Economic Cycles

Net profit margin behavior during recession periods provides valuable lessons for contemporary investors. During the 2008 financial crisis, many companies saw margins compressed as revenue declined while fixed costs remained constant. Banks, in particular, experienced dramatic margin contractions as loan losses mounted and EBIT deteriorated.

The COVID-19 pandemic of 2020-2021 created unusual margin dynamics. Some industries like e-commerce and technology services expanded margins as demand surged and operational efficiency improved. Others, particularly hospitality and travel, witnessed margins evaporate entirely as revenue collapsed.

Recession impact patterns typically include:

- Initial margin compression as revenue drops faster than companies can reduce costs

- Aggressive cost-cutting measures that eventually stabilize margins

- Quality differences emerge between well-managed and poorly-managed firms

- Recovery phase where margins often expand beyond pre-recession levels

Interpreting Net Profit Margin in Context

Raw margin percentages tell only part of the story. Sophisticated analysis requires understanding context, comparisons, and trends over time. A 5% net profit margin might represent excellent performance for a grocery chain but signal serious problems for a software company.

Klipfolio's industry benchmarks provide essential context for evaluating company performance. Comparing a firm's margins against industry peers reveals competitive positioning and operational efficiency relative to companies facing similar market conditions.

Year-over-Year Margin Analysis

Tracking how net profit margin evolves over multiple quarters and years uncovers important trends that single-point measurements miss. Expanding margins often indicate improving operational efficiency, pricing power, or successful cost management initiatives. Contracting margins might signal increasing competition, rising input costs, or operational challenges.

Consider the case of major retailers during the 2010s. Companies that successfully adapted to e-commerce maintained or improved margins by reducing physical store footprints and optimizing supply chains. Those that failed to adapt saw margins steadily erode as sales shifted to lower-margin online channels while maintaining expensive store networks.

Margin trend indicators include:

- Consistent expansion suggesting sustainable competitive advantages

- Volatile fluctuations indicating sensitivity to external factors

- Steady decline potentially signaling structural business challenges

- Seasonal patterns reflecting industry-specific demand cycles

The relationship between margins and capital expenditure cycles also deserves attention. Companies making substantial investments in growth often experience temporary margin compression before realizing benefits.

Factors That Drive Margin Improvement

Companies employ various strategies to enhance net profit margin over time. Historical case studies reveal both successful and failed approaches to margin expansion, offering valuable lessons for contemporary businesses.

Pricing power represents one of the most direct paths to margin improvement. Companies with strong brands, unique products, or dominant market positions can raise prices without proportional volume losses. Apple's margin expansion from the 2000s onward exemplifies this principle, as the company commanded premium pricing while maintaining strong demand.

Operational Efficiency Initiatives

Cost reduction programs have historically produced mixed results. Successful efficiency initiatives target structural improvements rather than across-the-board cuts. Toyota's lean manufacturing principles, developed in the 1970s and 1980s, demonstrated how process optimization could simultaneously reduce costs and improve quality.

Effective margin improvement strategies:

- Process automation: Replacing manual tasks with technology to reduce labor costs

- Supply chain optimization: Negotiating better terms, consolidating suppliers, reducing waste

- Product mix shift: Emphasizing higher-margin products or services

- Customer segmentation: Focusing on more profitable customer segments

- Scale economies: Spreading fixed costs across larger revenue bases

The strategies outlined by Finverium emphasize sustainable approaches to margin enhancement that avoid damaging customer relationships or long-term competitive positioning.

Net Profit Margin and Investment Decisions

Investors have long used net profit margin as a key screening criterion when evaluating potential investments. Warren Buffett's investment philosophy emphasizes companies with durable competitive advantages that manifest partly through superior margins sustained over decades.

During growth phases, investors often tolerate lower margins if companies demonstrate clear paths to future profitability. Amazon's history illustrates this pattern, as the company operated on extremely thin margins during its expansion phase, reinvesting nearly all gross profits into growth initiatives. As the business matured, margins expanded substantially.

| Margin Level | Interpretation | Investment Consideration |

|---|---|---|

| Below 0% | Unprofitable | Evaluate path to profitability, cash runway |

| 0-5% | Low margin | Assess industry norms, competitive position |

| 5-10% | Moderate margin | Compare to sector peers, trend direction |

| 10-20% | Strong margin | Examine sustainability, competitive threats |

| Above 20% | Exceptional margin | Consider defensibility, market dynamics |

The relationship between net profit margin and other metrics like debt-to-equity ratio provides additional investment context. High leverage combined with thin margins creates significant risk, as revenue volatility can quickly push companies into financial distress.

Margin Quality Assessment

Not all profit margin improvements deserve equal credit. Analysts distinguish between high-quality margin gains driven by operational improvements versus lower-quality gains resulting from one-time benefits or unsustainable cost cuts.

Revenue growth accompanied by margin expansion typically signals exceptional business performance. This combination suggests both strong market demand and operational leverage. Conversely, margin expansion amid declining revenue often indicates defensive cost-cutting rather than competitive strength.

Quality indicators include:

- Margin improvement coupled with market share gains

- Consistent margins across economic cycles

- Organic growth rather than acquisition-driven expansion

- Investment in research and development despite margin pressure

Sector-Specific Margin Dynamics

Different industries exhibit characteristic margin profiles shaped by competitive dynamics, capital requirements, and business model structures. Understanding these sector-specific patterns enhances interpretation of individual company performance.

Technology and software companies have historically demonstrated the highest net profit margins due to low marginal costs and significant operating leverage. Once software is developed, distributing additional copies costs virtually nothing, allowing extraordinary margins as revenue scales. Microsoft's margins during its Windows and Office dominance exemplified this dynamic.

Retail and Consumer Goods Margins

Retail businesses operate in highly competitive markets with limited differentiation, resulting in characteristically low margins. Walmart's strategy of accepting minimal margins while maximizing volume illustrates one successful approach. Luxury retailers like Tiffany demonstrate that positioning and brand value can support substantially higher margins even within retail.

The IBISWorld analysis of margin increases highlights which sectors have recently experienced significant margin expansion, providing insights into evolving industry dynamics and competitive conditions.

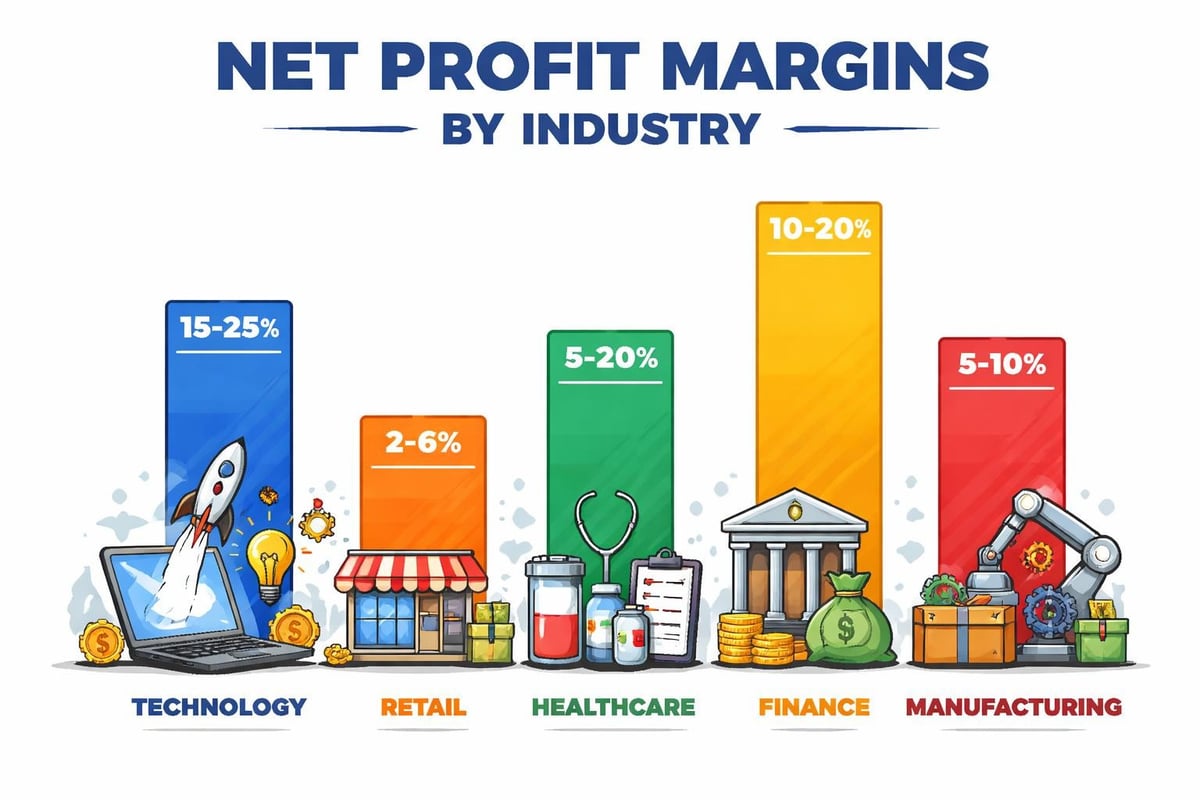

Sector margin characteristics:

- Technology/Software: 15-30% typical, driven by scalability and intellectual property

- Healthcare/Pharmaceuticals: 10-25% typical, reflecting R&D costs but patent protection

- Financial Services: 10-20% typical, varying with interest rate environments

- Retail: 2-8% typical, compressed by competition and operational complexity

- Manufacturing: 5-12% typical, influenced by automation and capacity utilization

Financial institutions present unique margin considerations related to net interest margin, which measures the spread between interest earned and interest paid. This metric complements traditional net profit margin analysis for banks and lending institutions.

Common Margin Analysis Mistakes

Even experienced analysts sometimes misinterpret net profit margin data, leading to flawed conclusions. Recognizing common pitfalls improves analytical accuracy and investment decision quality.

Comparing margins across incompatible industries represents a frequent error. Judging a grocery chain's 3% margin against a software company's 25% margin provides no useful insight, as the business models bear no resemblance. Meaningful comparisons require similar business characteristics and competitive dynamics.

Ignoring Margin Sustainability

Another mistake involves projecting current margins indefinitely into the future without considering competitive threats or cyclical factors. The newspaper industry's historically strong margins eroded dramatically as digital disruption transformed media consumption. Investors who assumed margin persistence suffered significant losses.

Common analytical errors:

- Overlooking one-time items that artificially inflate or depress margins

- Failing to adjust for accounting changes that affect comparability

- Ignoring cash flow metrics that might contradict margin trends

- Neglecting capital intensity differences between companies

- Misunderstanding inventory accounting impacts on margins

The relationship between net profit margin and free cash flow deserves particular attention. Companies can show strong margins while generating weak cash flow if substantial capital reinvestment is required or working capital demands are significant.

Using Historical Data for Margin Forecasting

Historical margin analysis provides valuable inputs for projecting future profitability. Examining how companies performed during previous economic cycles, competitive disruptions, or industry transformations helps calibrate realistic expectations.

General Electric's margin history illustrates both the insights and limitations of historical analysis. The company's margins varied substantially across different business units and economic periods. Understanding these patterns helped predict performance during industrial downturns but failed to anticipate the financial services challenges that emerged in 2008.

Pattern recognition across multiple companies and time periods produces more reliable forecasts than analyzing single companies in isolation. When most competitors in an industry face margin pressure simultaneously, sector-wide challenges likely exist rather than company-specific problems.

Historical analysis approaches:

- Identify margin behavior during previous recessions or expansions

- Examine competitor margin evolution to understand industry dynamics

- Assess correlation between margins and economic indicators

- Study impact of technological disruption on historical margin patterns

- Evaluate management's track record of margin improvement initiatives

The finance terms glossary at Historic Financial News provides additional context for understanding the various metrics that complement margin analysis.

Regulatory and Accounting Considerations

Accounting standards and regulatory requirements significantly impact reported margins. Changes in revenue recognition rules, depreciation methods, or lease accounting can alter margins without affecting underlying business performance.

The shift from LIFO to FIFO inventory accounting, for instance, affects both reported margins and tax obligations. During inflationary periods, LIFO typically produces lower margins and tax bills, while FIFO shows higher margins but increased tax expenses.

International companies face additional complexity from currency translation effects. A strengthening dollar might compress margins for U.S. companies with significant international operations, even if operational performance remains strong in local currency terms.

Accounting factors affecting margins:

- Depreciation and amortization methods that allocate costs over time

- Revenue recognition timing that affects when sales are recorded

- Inventory valuation approaches impacting cost of goods sold

- Capitalization versus expensing decisions for certain expenditures

- Treatment of stock-based compensation in operating expenses

Understanding how deferred revenue impacts financial statements helps explain margin variations for subscription-based businesses that collect payment before delivering services.

Margin Analysis in Different Market Conditions

Net profit margin behavior varies substantially depending on overall market conditions and economic environments. Bull markets often see margin expansion as revenue growth outpaces expense increases and consumer confidence supports pricing power.

Bear markets typically compress margins through multiple mechanisms. Revenue often declines faster than companies can reduce expenses. Competitive pressures intensify as firms fight for shrinking demand. Input costs may remain elevated even as selling prices decline.

The stagflation period of the 1970s presented particularly challenging margin dynamics. Companies faced rising input costs from inflation while weak economic growth limited pricing power. Margins compressed across most industries as businesses absorbed cost increases without corresponding revenue gains.

Market condition impacts:

- Economic expansion: Revenue growth, operating leverage, margin expansion typical

- Peak cycle: Maximum margins, potential warning sign of coming slowdown

- Recession: Revenue decline, cost rigidity, severe margin compression common

- Recovery: Variable margins as revenue stabilizes faster than cost structure adjusts

- High inflation: Input cost pressure, lagging price adjustments, margin squeeze

Net profit margin remains one of the most reliable indicators of business performance across different industries, time periods, and economic conditions. By examining how companies have managed profitability through various market cycles, investors and analysts gain crucial insights that inform better decision-making. Historic Financial News empowers users to explore these patterns through interactive historical charts and AI-powered analysis, helping you understand the stories behind market movements and spot trends that shape investment outcomes. Whether you're researching specific companies or analyzing industry dynamics, our platform provides the historical context needed to make profitability metrics truly meaningful.