Net Interest Margin Guide: Understanding Trends in 2025

In 2025, net interest margin is at the heart of every bank’s profitability conversation. The changing financial landscape means this metric holds even more importance for banks, investors, and industry professionals.

This guide delivers a thorough look at net interest margin, covering how it is calculated, what drives its shifts, and why it matters more than ever. You will learn the components that shape NIM, recent and emerging trends, and practical strategies for success.

Why is NIM so critical now? It influences bank strategies, investor confidence, and even broader economic trends. Understanding where NIM is headed can empower you to make smarter decisions. Read on to master NIM and stay ahead in the financial sector.

What is Net Interest Margin?

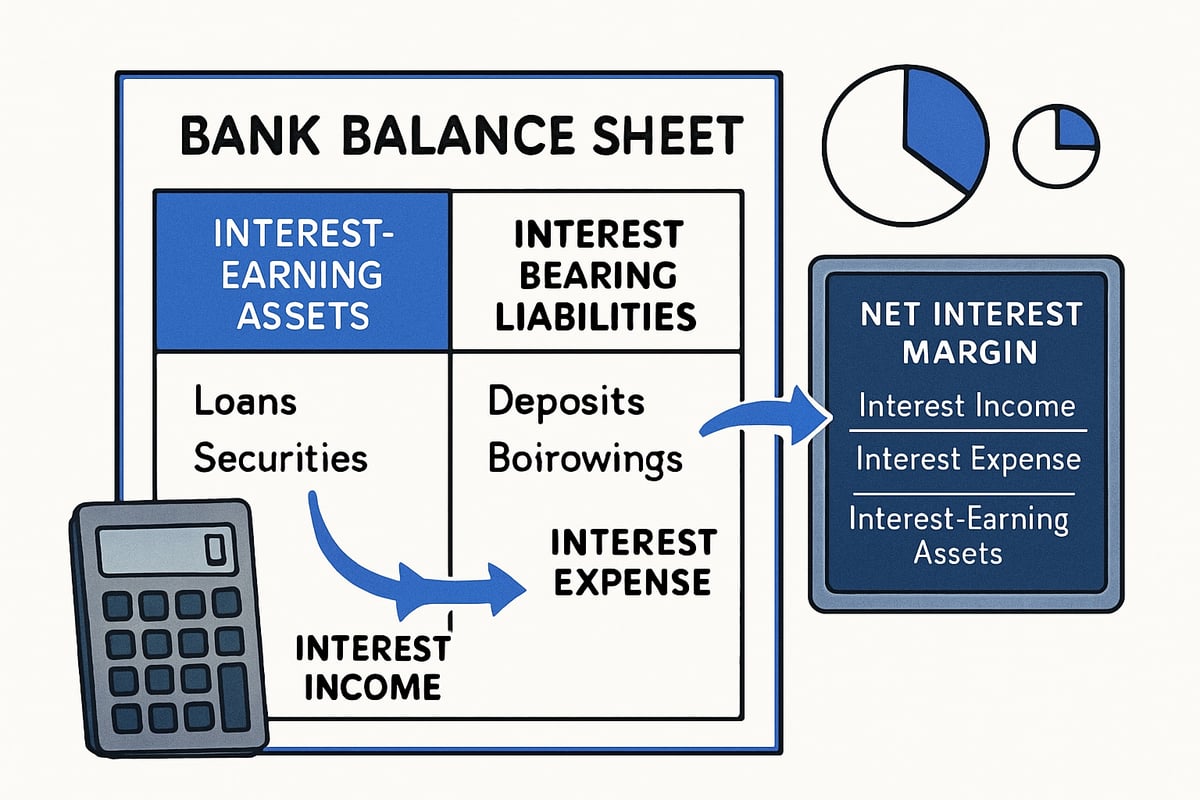

Net interest margin is a cornerstone metric in banking and finance, shaping how institutions measure profitability and efficiency. At its core, net interest margin represents the difference between what a bank earns from interest-generating assets and what it pays out on interest-bearing liabilities, relative to its average earning assets.

This ratio is vital because it provides a snapshot of how effectively a bank manages its core business: lending and borrowing. By monitoring net interest margin, banks can assess the spread between their income from loans or securities and their funding costs from deposits or borrowings. Financial professionals and investors rely on net interest margin to gauge operational performance and risk exposure.

For those new to banking terminology, our Key finance terms glossary can help clarify related concepts that often appear alongside net interest margin. Understanding this metric is essential for evaluating a bank’s health and its ability to generate value for shareholders.

Defining Net Interest Margin

Net interest margin is calculated as the difference between a bank’s interest income and its interest expenses, divided by its average earning assets. This metric helps banks and analysts understand how much profit is generated from core lending activities, after accounting for the cost of funds.

To illustrate, consider a bank that earns $5 million in interest income from loans and securities, while paying $2 million in interest expense on deposits and borrowings. If the bank’s average earning assets total $100 million, the net interest margin is calculated as:

NIM = (Interest Income – Interest Expense) / Average Earning Assets

NIM = ($5,000,000 – $2,000,000) / $100,000,000 = 0.03 or 3%

Net interest margin is often compared to other profitability ratios, such as Return on Assets (ROA) and Return on Equity (ROE). While ROA and ROE provide a broader view of overall performance, net interest margin focuses specifically on income from lending versus funding costs. This makes it a key metric for banks, especially in changing interest rate environments.

Analysts and regulators closely monitor net interest margin as it can signal operational efficiency, risk trends, and early warnings for financial distress. Even a small shift in net interest margin can have a significant impact on a bank’s net income and market valuation.

Components and Calculation of NIM

Understanding the components of net interest margin is crucial for accurate analysis. Interest income typically includes earnings from loans, mortgages, and investment securities. On the other side, interest expense covers costs associated with customer deposits, wholesale borrowings, and other funding sources.

The standard formula is:

Net Interest Margin = (Interest Income – Interest Expense) / Average Earning Assets

Let’s break down the calculation step by step:

- Calculate total interest income from all earning assets.

- Sum up all interest expenses paid on liabilities.

- Determine the average earning assets for the period.

- Apply the formula to derive net interest margin.

Banks may adjust calculations for nonperforming loans or tax-exempt securities, depending on reporting standards. For context, the average net interest margin for US banks ranged from 2.5% to 3.5% in 2023, according to industry data.

Proper classification of assets and liabilities is essential, as errors can distort the net interest margin and lead to misinformed decisions. Accurate calculation ensures that banks, investors, and regulators have a reliable measure of profitability for comparison and strategic planning.

The Importance of Net Interest Margin in 2025

In 2025, the net interest margin stands as a vital performance metric for banks and a central focus for investors, regulators, and analysts alike. As the financial sector navigates an environment marked by shifting rates and heightened competition, understanding the significance of net interest margin is essential for making informed decisions.

Why NIM Matters for Banks and Investors

The net interest margin is the heartbeat of a bank’s core business. It measures the spread between the income generated from loans and investments and the expenses paid to depositors and creditors. A robust net interest margin signals operational efficiency and strong risk management, directly influencing profitability and shareholder returns.

For banks, even minor shifts in the net interest margin can have significant financial consequences. For example, a 0.5% change in net interest margin can translate to millions, sometimes billions, in net income for large institutions. In 2023, a movement of just 10 basis points in net interest margin led to dramatic swings in profits across the sector.

| NIM Change | Estimated Impact on Net Income (Large Bank) |

|---|---|

| +0.10% | +$500 million |

| -0.10% | -$500 million |

| +0.50% | +$2.5 billion |

Banks adjust lending rates, deposit pricing, and their asset mix based on trends in net interest margin. When margins compress, institutions may tighten lending standards, seek higher-yielding assets, or innovate with new deposit products. Conversely, expanding net interest margin supports aggressive loan growth and investment.

Investors closely watch net interest margin because it directly affects bank valuations and signals underlying business health. Positive trends boost confidence, while declining margins can serve as early warnings of profitability headwinds or emerging credit risks.

Regulators also prioritize net interest margin when assessing capital adequacy and systemic stability. A declining net interest margin may prompt increased regulatory scrutiny or demands for higher capital buffers, especially in uncertain markets.

NIM’s Role in Economic Cycles and Market Conditions

The net interest margin is highly sensitive to economic cycles and shifts in monetary policy. During periods of low interest rates, such as the years following 2020, net interest margin often compresses as banks struggle to maintain spreads between what they earn on loans and pay on deposits. This compression can squeeze profitability and limit a bank’s ability to grow.

When central banks raise rates, the net interest margin typically expands, especially if banks can reprice loans faster than deposits. This dynamic was evident in 2024, when three rate hikes contributed to a 20 basis point average increase in net interest margin across U.S. banks. The relationship between the yield curve and net interest margin is crucial; an inverted curve can severely compress margins, while a steepening curve usually provides relief.

Historical data shows that net interest margin acts as both a leading and lagging indicator of broader financial conditions. For example, margin compression often precedes periods of credit tightening, while expansion can signal a more robust lending environment. During past recessions, net interest margin trends provided early warnings of deteriorating loan quality and heightened risk aversion.

In 2025, close monitoring of net interest margin is more important than ever. It offers predictive value for loan growth, asset quality, and overall bank resilience. For a current view of these dynamics, the Federal Reserve Bank of St. Louis provides a detailed analysis in Net Interest Margins Rise at U.S. Banks, highlighting recent trends and what they mean for the sector.

By tracking net interest margin alongside other financial metrics, banks and investors can better anticipate changes in the economic landscape and adjust their strategies accordingly.

Key Trends Shaping Net Interest Margin in 2025

The landscape for net interest margin in 2025 is dynamic and shaped by multiple forces. Financial professionals and investors must understand these evolving trends to successfully navigate the banking sector. Below, we break down the key factors that will define net interest margin performance in the coming year.

Interest Rate Environment and Monetary Policy

The interest rate environment remains a primary driver of net interest margin outcomes. In 2025, anticipated moves by the Federal Reserve are likely to set the tone for bank earnings. After three rate hikes in 2024, average net interest margin increased by 20 basis points, reflecting banks’ ability to reprice assets faster than liabilities.

Yield curve dynamics are critical. A flat or inverted curve compresses net interest margin, as banks struggle to profit from the spread between short-term funding costs and long-term lending rates. Conversely, a steepening curve usually leads to margin expansion, especially for institutions with a large proportion of variable-rate assets.

Forward guidance regarding future policy shifts will influence banks’ asset-liability strategies. Market expectations for additional rate moves, or a pause, will affect how banks price loans and deposits. For a deeper look at these drivers and their impact, Bank Trends: Can Margin Improvement Continue in 2025? provides an in-depth analysis of net interest margin prospects.

Competition, Digital Transformation, and Fintech Disruption

Competition is intensifying as digital banks and fintech lenders challenge traditional institutions. These new entrants often operate with lower overhead, allowing them to offer higher deposit rates and more flexible lending solutions. As a result, established banks face margin pressure and must adapt to maintain net interest margin levels.

Neobanks, for example, have gained market share by attracting rate-sensitive customers, forcing legacy banks to adjust deposit pricing. Fintech firms leverage technology and data analytics to optimize lending decisions and manage risk, impacting the competitive landscape.

Digital transformation is also reshaping operational models. The adoption of AI and automation enables banks to streamline processes, reduce costs, and better match assets and liabilities. In 2024, 35% of banks reported that fintech competition directly affected their net interest margin, signaling that innovation is now a core component of profitability strategy.

Regulatory and Accounting Changes

Changes in regulatory frameworks and accounting standards can significantly impact net interest margin reporting and management. The continued rollout of Basel III and Basel IV requirements in 2025 demands stricter capital and liquidity standards, which may narrow spreads and affect lending activity.

The Current Expected Credit Loss (CECL) model requires banks to provision for loan losses earlier, impacting how net interest margin is calculated and reported. These provisions can temporarily reduce reported margins, especially during periods of economic uncertainty.

Accounting updates under IFRS and GAAP, particularly those related to interest income recognition and asset classification, may also alter the comparability of net interest margin figures across banks. Institutions that proactively adapt to regulatory changes and enhance transparency will be better positioned to maintain investor confidence and regulatory compliance.

Shifts in Loan and Deposit Mix

The composition of a bank’s loan and deposit portfolio plays a critical role in determining net interest margin. In 2025, trends indicate a shift toward higher-yielding loan products, such as commercial and industrial loans, as banks seek to offset margin compression from intense competition.

On the deposit side, customers are migrating from low-cost checking accounts to higher-yield money market and certificate of deposit products. In 2024, there was a 15% rise in high-yield deposit offerings, reflecting consumer demand for better returns. This shift increases funding costs and can reduce net interest margin if not balanced by higher asset yields.

Banks must strategically manage their product mix to optimize profitability. Monitoring changes in loan demand, deposit flows, and market rates is essential for sustaining healthy net interest margin levels in a rapidly evolving environment.

Macroeconomic and Geopolitical Factors

Broader macroeconomic and geopolitical dynamics also shape net interest margin trends. Inflation remains a key concern, as rising prices may prompt central banks to adjust policy rates, directly influencing loan pricing and deposit costs. Persistent inflation can erode real returns on assets, impacting margin sustainability.

Geopolitical risks, such as trade tensions and global sanctions, can disrupt funding markets and increase the cost of capital. Emerging markets have experienced heightened net interest margin volatility from 2022 to 2024, highlighting the importance of geographic diversification and risk management.

Global banks may demonstrate greater resilience due to diversified operations, while domestic institutions face localized risks. Staying attuned to economic data releases and international developments will be crucial for accurately forecasting net interest margin performance in 2025.

Factors Influencing Net Interest Margin: A Deep Dive

Understanding what shapes net interest margin is essential for banks aiming to stay competitive in 2025. Multiple internal and external factors impact this crucial metric, from balance sheet strategies to technological innovation and evolving customer preferences. Let's explore the most influential drivers of net interest margin in today's complex environment.

Asset-Liability Management (ALM) Strategies

Effective asset-liability management sits at the core of optimizing net interest margin. Banks must balance the maturity and repricing of assets and liabilities to minimize interest rate risk and maximize returns. ALM teams use tools like gap analysis, duration matching, and interest rate swaps to manage mismatches that could erode net interest margin.

A key aspect is understanding the maturity date in finance, as it determines when loans and deposits reset or roll off the books. By actively monitoring and adjusting maturity profiles, banks can lock in favorable spreads or hedge against rate shocks. In 2025, best practices include scenario modeling and dynamic stress testing to anticipate potential margin compression during volatile periods. Strong ALM frameworks help ensure stability and resilience in net interest margin across changing market cycles.

Credit Quality, Risk Management, and Loan Loss Provisions

Credit risk directly impacts net interest margin. When delinquencies rise, banks must increase loan loss provisions, reducing reported net interest margin. Proactive risk management—through robust underwriting, portfolio diversification, and early warning systems—helps protect against large swings in credit costs.

For example, in 2024, average provision rates increased by 12 percent as banks anticipated higher defaults, putting downward pressure on net interest margin. By carefully monitoring asset quality and adjusting reserves, banks can maintain healthy margins even in tougher credit environments. Strategic risk management not only preserves earnings but also signals financial strength to regulators and investors.

Technology, Operational Efficiency, and Cost Control

The digital transformation of banking is reshaping the landscape for net interest margin. Automation in credit underwriting, deposit gathering, and treasury management streamlines processes and lowers funding costs. Banks with advanced digital platforms can quickly adjust rates, optimize pricing, and reduce operational overhead.

AI-driven analytics enable real-time monitoring of net interest margin and support smarter asset-liability decisions. In 2024, banks with high digital adoption saw a 0.15 percent higher net interest margin compared to peers. By investing in technology, institutions gain both efficiency and agility, allowing them to respond swiftly to changing market conditions and customer demands.

Customer Behavior and Product Innovation

Customer preferences are evolving, influencing how banks structure their loan and deposit products. A shift toward high-yield savings, bundled accounts, and tiered-rate offerings can affect net interest margin by altering the cost of funds and revenue streams.

Innovative products that appeal to specific customer segments, combined with effective cross-selling and retention strategies, help banks sustain or grow net interest margin. In 2025, understanding these behavioral shifts is more important than ever, as competition from fintechs and digital challengers continues to intensify. Banks that anticipate and adapt to customer needs are better positioned to defend their margins and drive long-term profitability.

How to Analyze and Interpret NIM Data in 2025

Understanding how to properly analyze net interest margin data is essential for financial professionals aiming to stay competitive in 2025. The right approach provides clarity on bank performance, uncovers trends, and informs smarter decisions. Let’s break down the key steps and tools for interpreting net interest margin, using the most current benchmarks and insights.

Key Metrics and Benchmarks

Comparing net interest margin across peer groups and bank sizes is the first step in meaningful analysis. In 2025, analysts look at quarterly and annual NIM figures to spot trends and outliers.

For instance, community banks tend to report higher net interest margin compared to large money center banks due to their focus on relationship lending and lower reliance on wholesale funding. According to the First Quarter 2025 Banking Conditions, top-quartile banks maintained NIMs above 3.2% in 2024, while the industry median was closer to 2.9%.

| Bank Type | Average NIM (2024) |

|---|---|

| Community Banks | 3.3% |

| Large Money Center | 2.7% |

| Industry Median | 2.9% |

Tracking these benchmarks helps identify leaders and laggards. Always consider asset mix, funding strategies, and geographic focus when interpreting net interest margin data.

Tools and Techniques for NIM Analysis

Effective analysis of net interest margin relies on a combination of ratio analysis, trend charts, and scenario modeling. Start by plotting NIM trends over several quarters to visualize stability or volatility.

Scenario modeling is especially useful in today’s shifting rate environment. By simulating net interest margin under various rate or credit scenarios, analysts can stress test a bank’s resilience. For example:

# Simulate NIM under different rate scenarios

base_nim = 0.029

rate_shock = 0.002

new_nim = base_nim + rate_shock

print(f"Adjusted NIM: {new_nim:.3f}")

In addition to NIM, reviewing related metrics such as the debt-to-equity ratio explained provides a more complete picture of a bank’s financial health. Avoid common pitfalls, such as ignoring changes in asset composition or failing to adjust for one-time items.

Insights from Historical NIM Trends

Analyzing historical net interest margin cycles offers critical context for current interpretations. For instance, during the 2008 financial crisis and the 2020 pandemic, NIMs compressed as rates fell and risk aversion spiked. Conversely, tightening cycles have historically led to NIM expansion, though not uniformly across all banks.

When using historical data, adjust for structural changes in banking—such as digital transformation or regulatory shifts—to ensure relevant comparisons. Lessons from past volatility can help anticipate future movements in net interest margin, guiding more informed strategies in 2025.

Ultimately, integrating historical insight with current data allows analysts and investors to spot early warning signs or opportunities, fostering better financial decision-making.

Strategies for Navigating Net Interest Margin Challenges in 2025

Adapting to the evolving financial landscape requires banks and investors to implement robust strategies to safeguard and optimize net interest margin. In 2025, proactive management, data-driven decision-making, and continuous monitoring are essential for success. Let us explore the core approaches to navigate net interest margin challenges effectively.

Proactive NIM Management for Banks

Banks must take a proactive stance to protect net interest margin amid shifting market conditions. Diversifying earning assets and deposit sources helps reduce concentration risk and smooth out fluctuations in income. Dynamic pricing strategies for both loans and deposits allow institutions to respond quickly to interest rate changes and competitive pressures.

Implementing loan maturity laddering is another effective tactic. By staggering loan maturities, banks can manage interest rate risk and maintain stable spreads across different rate environments. Leveraging technology for real-time monitoring of net interest margin empowers decision-makers to adjust strategies promptly. Automated tools, AI-driven analytics, and integrated dashboards provide actionable insights for optimizing margins.

- Diversify asset and deposit portfolios

- Employ dynamic, market-responsive pricing

- Ladder loan maturities to manage risk

- Use digital tools for real-time NIM tracking

These measures form the backbone of resilient net interest margin management.

Investor Approaches to NIM Trends

For investors, understanding net interest margin trends is crucial for identifying banks with strong earnings potential. Screening for institutions with consistent or expanding NIM can highlight those with sound asset-liability management and competitive positioning. Interpreting NIM signals helps refine stock selection and portfolio allocation decisions.

Investors should compare NIM performance across peer groups, considering factors such as loan mix, deposit structure, and market exposure. Banks demonstrating positive momentum in net interest margin often signal effective management and adaptability. For example, World's Largest Lender Expects Net Interest Margin Decline to Slow in 2025, reflecting a potential turning point in global banking profitability.

- Analyze peer-group NIM benchmarks

- Prioritize banks with favorable NIM trends

- Evaluate management’s response to margin pressures

Understanding these dynamics positions investors to capitalize on emerging opportunities in 2025.

Scenario Planning and Stress Testing

Preparing for adverse scenarios is essential to safeguard net interest margin against unexpected shocks. Banks should conduct scenario analysis and stress testing to assess NIM resilience under various economic conditions, such as stagflation or rapid rate hikes. These exercises help institutions build robust capital and liquidity buffers.

Simulating net interest margin under challenging environments enables banks to identify vulnerabilities and adjust strategies in advance. This approach not only supports regulatory compliance but also strengthens stakeholder confidence. By adopting scenario planning as a routine practice, banks can maintain operational stability and protect profitability.

- Conduct regular scenario modeling

- Build capital and liquidity reserves

- Adjust business models based on results

Scenario planning equips banks to navigate uncertainty and sustain net interest margin performance.

Continuous Learning and Market Monitoring

In 2025, ongoing education and vigilant market monitoring are vital for managing net interest margin. Staying updated on regulatory changes, macroeconomic trends, and competitive developments ensures that strategies remain relevant. Engaging with industry reports, financial news, and professional development resources deepens understanding of both net interest margin and related metrics, such as the quick ratio.

Continuous learning allows both banks and investors to anticipate shifts, adapt quickly, and implement best practices. Active monitoring of market signals and peer performance supports timely, informed decision-making.

- Subscribe to industry updates and regulatory alerts

- Participate in professional development programs

- Benchmark against industry leaders

By fostering a culture of learning and awareness, organizations can better navigate net interest margin challenges in the dynamic financial environment.

As you’ve seen, understanding net interest margin is crucial for navigating the financial landscape in 2025—whether you’re an investor, a student, or just someone curious about what drives bank performance. If you’re ready to dive deeper and discover the stories behind the numbers, why not experience financial history in a whole new way? We’re building an interactive platform where you can explore historical trends, access AI-powered insights, and make smarter decisions by learning from the past. If that sounds like something you’d value, Join Our Beta and help us shape the future of financial analysis.