Deferred Revenue Guide: Understanding Recognition in 2025

Deferred revenue isn’t just an accounting technicality, it’s a critical indicator of a company’s future performance and financial health, especially as we move into 2025.

In this guide, we’ll break down what deferred revenue means, why it’s important, and how to recognize it correctly under the latest standards. You’ll learn how it impacts your financial statements, discover up-to-date recognition rules, and get step-by-step strategies for managing it effectively.

Ready to master deferred revenue and drive business success? Let’s get started.

What Is Deferred Revenue?

Understanding the basics of deferred revenue is essential for any business that accepts payments in advance. Deferred revenue refers to money a company receives before it has delivered goods or services, making it fundamentally different from earned revenue. Because the business still owes the customer value, deferred revenue is listed as a liability on the balance sheet, not as income.

For instance, companies like Netflix and SaaS providers often collect subscription fees upfront. Other examples include prepaid gym memberships and annual software licenses. Businesses with recurring or prepayment models rely heavily on deferred revenue to manage their operations and finances. For more definitions of accounting terms, you can check the Finance terms glossary.

Definition and Core Concepts

Deferred revenue is unearned income received in advance for products or services not yet delivered. This means customers have paid, but the company still has an obligation to fulfill. Unlike earned revenue, which reflects completed sales or delivered services, deferred revenue highlights what the business still owes.

The main reason deferred revenue appears as a liability is that the company could be required to refund the money if it fails to deliver. Typical examples include:

- Streaming subscriptions

- SaaS contracts

- Prepaid memberships

- Annual software licenses

Deferred revenue is especially important for companies with recurring or upfront payment models.

Deferred Revenue in Practice

Imagine a software company receives $12,000 upfront for a 12-month subscription. Instead of recognizing the entire amount as revenue immediately, the company records it as deferred revenue and then recognizes $1,000 per month as the service is provided.

This approach ensures revenue is matched to the period when the service is delivered, not when cash is received. While cash flow improves immediately, actual revenue reporting is more gradual. This keeps financial statements accurate and transparent. For example, Netflix and Roblox both show deferred revenue in their reports, reflecting future obligations to customers.

Why Deferred Revenue Matters

Deferred revenue is a key indicator of future obligations and overall financial health. Investors and analysts view a growing deferred revenue balance as a sign of strong customer commitment and a healthy sales pipeline.

It also signals potential future revenue streams, helping businesses forecast income. Accurate deferred revenue tracking boosts liquidity management, ensures compliance, and can positively influence business valuation. Understanding deferred revenue gives stakeholders a clearer picture of a company's stability and growth prospects.

Common Sources of Deferred Revenue

Businesses generate deferred revenue from a wide range of activities, including:

- Prepaid service contracts (subscriptions, retainers, maintenance)

- Sale of gift cards and vouchers

- Advance ticket sales for events

- Long-term projects with milestone billing

Each source creates a liability until the company fully delivers the promised goods or services. Knowing where deferred revenue comes from helps companies manage their cash flow and obligations effectively.

Key Accounting Principles Involved

Deferred revenue accounting relies on the accrual method and the matching principle, which require revenue to be recognized when earned, not when cash is received. The revenue recognition principle under both GAAP and IFRS sets the rules for when and how to move deferred revenue to earned revenue.

Timing is critical: companies must wait until the service or product is delivered before recognizing revenue. This ensures financial statements reflect true performance and obligations, maintaining transparency for all stakeholders.

Deferred Revenue Recognition: Standards and Compliance in 2025

Understanding how to recognize deferred revenue correctly is crucial as accounting standards evolve. For 2025, the rules are clear but require attention to detail. Let's explore the latest standards, compliance requirements, and practical steps for recognizing deferred revenue in your business.

Overview of Revenue Recognition Rules

The foundation for recognizing deferred revenue is set by ASC 606 (US GAAP) and IFRS 15 (international standards). Both frameworks focus on when the "control" of goods or services transfers to the customer, not just when cash is received.

The five-step revenue recognition model guides companies through:

- Identifying the contract with a customer

- Pinpointing performance obligations

- Determining the transaction price

- Allocating the price to obligations

- Recognizing revenue as obligations are satisfied

Deferred revenue sits at the intersection of these steps, requiring businesses to wait until they deliver value before recognizing income.

Deferred Revenue on Financial Statements

On the balance sheet, deferred revenue appears as a liability, signaling an obligation to deliver goods or services in the future. It can be classified as current (due within 12 months) or long-term (over 12 months), depending on the delivery schedule.

When revenue is earned, the liability decreases, and the income statement reflects the earned amount. Here’s a typical journal entry:

When cash is received:

Dr. Cash $12,000

Cr. Deferred Revenue $12,000

As revenue is earned each month:

Dr. Deferred Revenue $1,000

Cr. Revenue $1,000

This process ensures deferred revenue is accurately tracked and recognized over time.

Key Regulatory Updates for 2025

The landscape for deferred revenue recognition continues to adapt, especially with the rise of SaaS and digital business models. Recent updates include FASB’s 2021 rule on acquisition accounting, which clarified how acquirers should recognize an acquiree’s deferred revenue at fair value.

For 2025, regulators emphasize transparent disclosures and real-time tracking, particularly for companies with complex contracts. To stay informed on the latest changes, refer to On the Radar — Revenue Recognition (November 2024), which summarizes the newest guidance impacting deferred revenue.

Tax Implications of Deferred Revenue

Tax treatment of deferred revenue can differ from accounting recognition. In some jurisdictions, deferred revenue is not taxable until it is earned, aligning with the delivery of goods or services. However, others may require tax payment when cash is received, regardless of when revenue is recognized in financial statements.

Careful planning can help businesses defer tax liabilities and optimize cash flow. Understanding local tax regulations is key to managing deferred revenue efficiently and avoiding surprises during tax season.

Audit and Reporting Considerations

Accurate tracking of deferred revenue is essential for audit readiness. Auditors look for clear records showing when and how revenue is recognized. Common issues include timing errors, incomplete documentation, and misclassification of liabilities.

To comply with industry-specific requirements, businesses should maintain detailed supporting documents for each contract and automate reconciliations where possible. Transparent reporting reduces the risk of audit findings and builds trust with stakeholders.

Real-World Example: SaaS Company Deferred Revenue

Consider a SaaS company that receives a $12,000 annual subscription payment upfront. The company records the full amount as deferred revenue at first. Each month, it recognizes $1,000 as revenue as the service is delivered.

Modern tools like Stripe’s revenue waterfall automate this process, ensuring compliance and providing real-time insights. By tracking deferred revenue diligently, the company maintains accurate books and meets both regulatory and customer expectations.

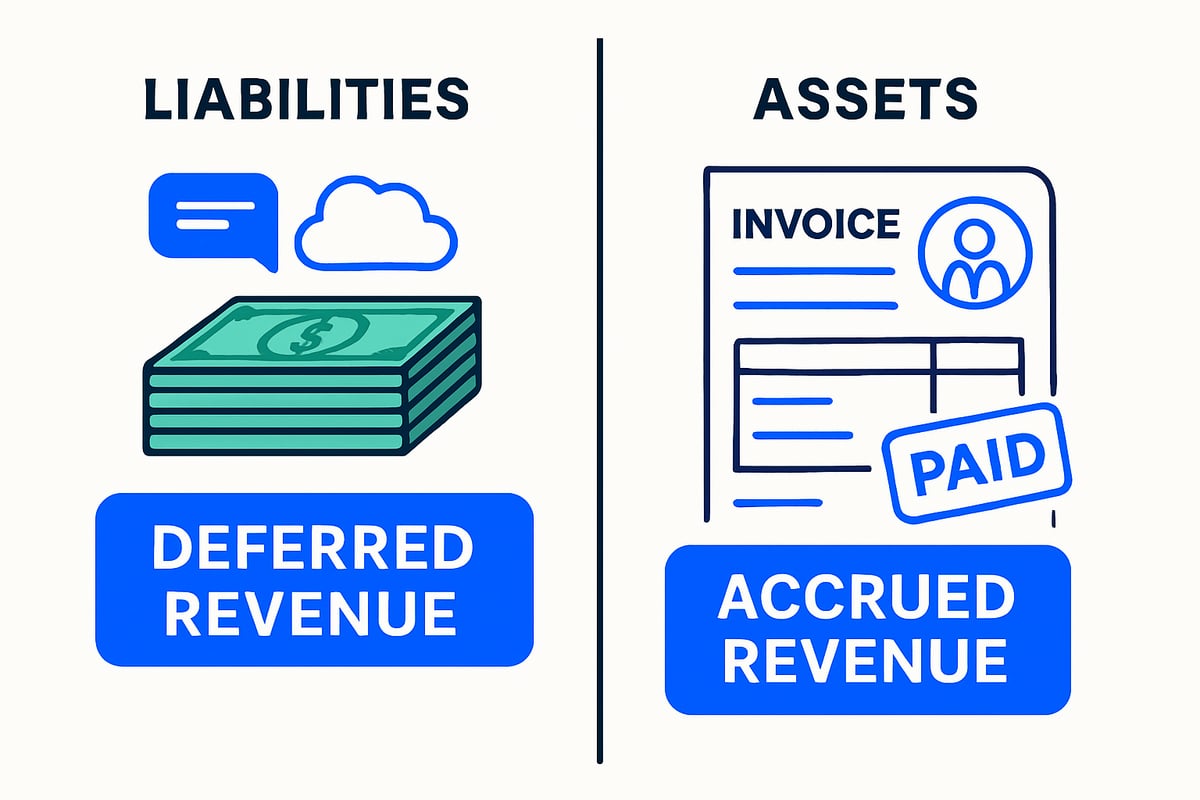

Deferred Revenue vs. Accrued Revenue: Key Differences

Understanding the difference between deferred revenue and accrued revenue is essential for accurate financial reporting. Both terms relate to timing, but they play opposite roles in accounting. Deferred revenue represents money received for goods or services not yet delivered, so it is recorded as a liability. In contrast, accrued revenue is income earned but not yet received, recorded as an asset. On the balance sheet, deferred revenue sits under liabilities, signaling future obligations, while accrued revenue appears as a current asset. These classifications can also affect important financial ratios, such as the debt-to-equity ratio overview, since deferred revenue increases liabilities, impacting how investors and analysts view company leverage.

Definitions and Contrasts

Deferred revenue is cash a business has collected in advance for products or services it has not yet delivered. It is a liability because the company still owes the customer. Accrued revenue, on the other hand, is income a company has earned by delivering goods or services, but the payment has not yet been received. This is recorded as an asset, reflecting the right to future cash. On the balance sheet, deferred revenue lowers owner equity by increasing liabilities, while accrued revenue increases assets. Understanding these definitions helps clarify why deferred revenue must be carefully tracked, as it represents obligations rather than immediate income.

Practical Examples

To illustrate the difference, let’s look at a couple of scenarios. If a customer pays for a full year of a magazine subscription upfront, that payment becomes deferred revenue until each issue is delivered. For accrued revenue, think of a consultant who completes a project and sends an invoice, but the client hasn’t paid yet. That earned but unpaid amount is accrued revenue. Stripe often visualizes this with charts that show deferred revenue as a liability and accrued revenue as an asset, making it easier to see how each impacts the company’s financial position.

Why the Distinction Matters

Distinguishing between deferred revenue and accrued revenue is vital for accurate financial statements. Properly classifying these ensures revenue and expenses are matched to the correct periods, supporting the matching principle in accounting. If deferred revenue is mistaken for earned income, a business could overstate its profitability. Misclassifying accrued revenue can lead to understating assets and revenue. This distinction directly affects how stakeholders interpret a company’s financial health and influences key metrics like liquidity and profitability.

Common Mistakes and How to Avoid Them

Some businesses struggle with recognizing deferred revenue too early, which can overstate income and mislead stakeholders. Others forget to accrue revenue, understating assets and missing out on reflecting true earnings. To avoid these pitfalls, it’s essential to use robust accounting systems that automate tracking and recognition. Regular reviews and reconciliations help ensure deferred revenue and accrued revenue are recorded at the right time, supporting transparency and compliance.

How Deferred Revenue Impacts Financial Statements and KPIs

Understanding how deferred revenue shapes financial statements and KPIs is essential for modern businesses. This section breaks down the specific ways deferred revenue affects your balance sheet, income statement, cash flow, and the performance metrics investors care about. Let’s explore why managing deferred revenue is a cornerstone of financial clarity.

Balance Sheet Implications

Deferred revenue appears on the balance sheet as a liability. This classification signals that your company has collected cash for goods or services not yet delivered. High levels of deferred revenue often indicate strong customer commitment, especially for subscription-based businesses. However, it also means your company has future obligations to fulfill. If those obligations are not met, you risk refund liabilities and potential damage to reputation. Stakeholders closely watch deferred revenue balances, as they reflect both future earnings potential and outstanding commitments.

Income Statement Effects

As your company delivers goods or services over time, deferred revenue moves from the balance sheet to the income statement. Each period, a portion is recognized as earned revenue, directly impacting reported profitability. This transition ensures revenue is matched to the correct period, improving accuracy and transparency. For instance, a SaaS company recognizing monthly revenue from an annual contract will show steady income growth. The process, often managed through a revenue waterfall, keeps earnings aligned with actual service delivery and supports better forecasting.

Cash Flow Considerations

Deferred revenue provides an immediate boost to cash flow when customers pay upfront. However, this cash cannot be recognized as income until services are delivered. This distinction is vital for liquidity planning. Deferred revenue can improve your company’s ability to cover short-term obligations, but it is not included in profit calculations until earned. In many cases, deferred revenue is not taxable until it’s officially recognized, helping businesses manage tax liabilities efficiently across reporting periods.

Influence on Key Performance Indicators

Deferred revenue directly influences several KPIs, including liquidity ratios, working capital, and profitability measures. For example, the quick ratio explained highlights how deferred revenue reduces available liquid assets, impacting a company's ability to meet immediate obligations. Investors and analysts examine deferred revenue trends to assess business health, customer retention, and growth potential. High deferred revenue can increase a company’s valuation by signaling predictable future income, but mismanagement may distort performance metrics.

Compliance and Reporting Standards

Accurate tracking and reporting of deferred revenue is essential for compliance with FASB and IASB standards. Modern accounting rules require transparent disclosures, especially for digital and subscription-based businesses. Companies must ensure that deferred revenue balances are supported by detailed documentation and reconciled regularly. Transparent reporting not only meets regulatory requirements but also builds trust with investors and auditors, strengthening your company’s reputation and financial standing.

Managing and Tracking Deferred Revenue: Step-by-Step Guide for 2025

Effectively managing deferred revenue is essential for accurate financial reporting, compliance, and long-term business success. As accounting standards evolve and subscription models become more prevalent, it’s never been more important to have a clear, actionable process for tracking and recognizing deferred revenue.

Step 1: Identify All Sources of Deferred Revenue

Begin by reviewing every contract, invoice, and payment term to pinpoint all streams that generate deferred revenue. This review is crucial for businesses with diverse offerings such as software-as-a-service (SaaS) subscriptions, prepaid maintenance agreements, and event ticket sales.

Categorize deferred revenue sources by type—recurring subscriptions, one-time prepayments, or milestone-based projects. For example, a SaaS company may receive annual payments upfront, while an event organizer collects ticket fees months in advance.

A comprehensive list ensures you do not miss any income that must be accounted for as deferred revenue. This step lays the groundwork for accurate tracking and compliance.

Step 2: Set Up Proper Accounting Systems

Implementing robust accounting software is vital for managing deferred revenue efficiently. Look for platforms that offer real-time tracking, automated revenue recognition schedules, and seamless integration with billing systems.

Features like dashboards and revenue recognition tools (such as Stripe or NetSuite) help you visualize deferred revenue balances and automate complex calculations. Integration ensures every invoice and payment is captured without manual errors.

Automated systems not only streamline deferred revenue management, they also reduce the risk of misreporting and provide a clear audit trail for every transaction.

Step 3: Apply the Five-Step Revenue Recognition Model

To comply with modern standards, apply the five-step revenue recognition model for each contract involving deferred revenue:

- Identify the contract with the customer.

- Identify separate performance obligations.

- Determine the transaction price.

- Allocate the price to each obligation.

- Recognize revenue as obligations are satisfied.

For instance, a subscription service recognizing deferred revenue would spread a $1,200 annual payment over 12 months, recording $100 as revenue each month as the service is delivered.

This structured approach ensures deferred revenue is recognized in line with GAAP and IFRS requirements.

Step 4: Schedule Revenue Recognition

Once you identify and categorize deferred revenue, create detailed recognition schedules. Depending on the agreement, you might use monthly, quarterly, or milestone-based schedules to transfer deferred revenue into earned revenue.

A revenue recognition calendar helps you visualize when income will be recognized, supporting cash flow planning and forecasting. For example, an annual software license paid upfront should be recognized as revenue in equal monthly installments.

Consistent scheduling ensures deferred revenue transitions accurately, reflecting true business performance.

Step 5: Monitor and Adjust for Changes

Deferred revenue balances can change due to contract modifications, cancellations, or customer refunds. Regularly review contracts for adjustments and update your accounting records accordingly.

Maintain detailed documentation for every change—this supports both audit readiness and transparency. Automated alerts in your accounting system can notify you when deferred revenue schedules need updating.

By actively monitoring deferred revenue, you minimize the risk of errors and ensure your financial statements remain accurate.

Step 6: Ensure Audit Readiness and Compliance

Regular reconciliations of deferred revenue accounts are essential for audit readiness. Cross-check balances with supporting documentation for each transaction, ensuring nothing is missed.

Stay up to date with compliance requirements, especially as new standards emerge. For a detailed overview of recent and upcoming accounting changes affecting deferred revenue, see this Accounting Update — Overview for 2024 and what's coming up in 2025.

Proactive compliance and clear documentation make audits smoother and reduce regulatory risks.

Step 7: Leverage Analytics for Forecasting and Planning

Harness deferred revenue data to improve forecasting and strategic planning. Modern analytics tools can project future income based on current deferred revenue balances, helping you plan budgets, staffing, and investments with greater confidence.

For example, Stripe’s analytics features allow businesses to model how deferred revenue will be recognized over time, supporting more informed decision-making.

By leveraging these insights, you can align operational strategies with expected revenue streams and drive sustainable growth.

Risks, Challenges, and Best Practices in Deferred Revenue Recognition

Managing deferred revenue presents unique challenges that can impact a company’s financial health and reputation if not handled with care. Understanding the most common risks, how to mitigate them, and adopting best practices is essential for accurate reporting and sustainable growth as we move into 2025.

Common Risks and How to Mitigate Them

Companies face several risks when accounting for deferred revenue. Misreporting can distort financial statements, leading to regulatory issues or lost investor trust. Timing errors, such as recognizing deferred revenue too soon, may inflate income inaccurately.

To address these risks:

- Implement automated systems to manage deferred revenue schedules.

- Conduct regular reconciliations of deferred revenue accounts.

- Maintain clear documentation for every contract and payment.

Additionally, cash flow ambiguity is a concern, especially when revenue and cash timing do not align. Using robust tracking tools helps mitigate this challenge, ensuring deferred revenue is recognized only when earned.

Customer Expectations and Relationship Management

Deferred revenue directly affects customer relationships. When businesses receive payments in advance, customers expect timely delivery of goods or services. Failure to fulfill obligations can result in refund liabilities and erode trust.

Clear communication about service periods, renewal policies, and any changes is key. Proactive updates and transparency help prevent misunderstandings related to deferred revenue. Companies should also monitor contract performance to ensure all obligations are met, reducing the risk of disputes or lost business.

Industry-Specific Challenges

Different industries face unique deferred revenue recognition challenges. Subscription-based and SaaS companies must manage high transaction volumes and complex billing cycles. Digital goods providers encounter evolving regulatory standards, while project-based businesses juggle milestone payments and changing contract terms.

For example, new guidance on accounting for deferred revenue in business combinations under ASC 606 impacts how acquired deferred revenue is measured and recognized. Staying informed about industry developments helps companies adapt processes and remain compliant.

Best Practices for 2025

To stay ahead, businesses should prioritize automation and continual learning. Key best practices for deferred revenue in 2025 include:

- Leveraging automated revenue recognition software for accuracy.

- Training finance teams on updated regulations and standards.

- Regularly reviewing compliance tools and processes.

- Monitoring regulatory changes, such as those discussed in Revenue recognition: Time to implement the final regulations.

By integrating these practices, companies can streamline deferred revenue management and reduce the risk of costly errors.

Real-World Case Studies and Lessons Learned

Case studies highlight the impact of effective deferred revenue practices. Some businesses have faced penalties for recognizing deferred revenue too early, resulting in restated earnings and damaged credibility. Others have improved cash flow forecasting by implementing real-time tracking tools, leading to more confident decision-making.

Lessons learned include:

- The importance of accurate scheduling and documentation.

- Regular audits to ensure compliance.

- Leveraging analytics to transform deferred revenue data into actionable business insights.

By learning from both mistakes and success stories, organizations can refine their deferred revenue strategies and foster long-term growth.

Frequently Asked Questions About Deferred Revenue in 2025

Do you have questions about deferred revenue as we head into 2025? You are not alone. Here are answers to the most common queries business owners, accountants, and finance teams ask about deferred revenue, its recognition, and its impact.

What types of businesses are most affected by deferred revenue?

Businesses that receive payment before delivering goods or services are most impacted by deferred revenue. This includes subscription-based companies like streaming services, SaaS providers, gyms, and any business selling prepaid memberships or annual licenses.

Event organizers, consulting firms with retainers, and companies selling gift cards also commonly deal with deferred revenue. If your customers pay upfront, you likely need to track deferred revenue closely.

How do new accounting standards impact deferred revenue recognition in 2025?

In 2025, ASC 606 and IFRS 15 remain the main guides for deferred revenue recognition. These standards require businesses to recognize revenue only as they fulfill performance obligations, not when cash is received.

The latest updates emphasize the “transfer of control” and ensure companies match revenue to when goods or services are delivered. Staying compliant means reviewing contracts and properly documenting performance milestones.

Can deferred revenue ever be considered an asset?

Deferred revenue is always considered a liability on the balance sheet, not an asset. This is because it represents money received for obligations the company still needs to fulfill.

If you are curious about other balance sheet liabilities, such as a sinking fund in finance, understanding their similarities can help clarify why deferred revenue is not recognized as earned income until the service or product is delivered.

How does deferred revenue affect company valuation?

Deferred revenue can positively impact valuation by demonstrating future revenue streams and strong customer commitment. Investors often view a high deferred revenue balance as a sign of business stability and recurring income.

However, if a company cannot fulfill its obligations, large deferred revenue balances may signal risk. Transparent reporting and proper recognition are essential for accurate valuation.

What are the most common mistakes companies make when managing deferred revenue?

Common mistakes include recognizing deferred revenue too early, which overstates income, or failing to adjust balances after cancellations or contract changes. Some companies neglect to update their accounting systems, leading to errors.

To avoid these pitfalls, ensure regular reconciliations and maintain clear documentation for every deferred revenue transaction.

How should refunds or cancellations be handled in deferred revenue accounting?

When customers cancel services or request refunds, you must adjust your deferred revenue balance. Reverse the unearned portion from liabilities and update your records to reflect the change.

Clear communication with customers and prompt updates to your accounting system help prevent revenue recognition errors and maintain trust.

What tools and software are recommended for managing deferred revenue efficiently?

Automated accounting platforms are your best ally for tracking deferred revenue. Consider these tools:

- Stripe for real-time revenue waterfall reporting

- NetSuite for scalable revenue management

- QuickBooks and Xero for small to midsize businesses

Choose solutions that integrate with your billing system and support compliance with the latest standards. These tools help ensure accuracy, save time, and support audit readiness.

Understanding deferred revenue is just one piece of the puzzle when it comes to interpreting the bigger financial picture. If you’re curious about how market history shapes today’s accounting standards or want to see how lessons from the past can help you make smarter decisions in 2025, you’re in good company. We’re building a platform designed for people like you—those who want to connect the dots between historical events and financial trends. Want to help us shape this journey and get early access to powerful tools and insights? Join as a Beta User