Unit Investment Trust Guide: Everything You Need to Know 2025

Interest in diversified investments is soaring as more people seek smarter ways to grow their money in 2025. Investors are paying close attention to unique options that offer transparency and cost efficiency.

One such option, the unit investment trust, has been gaining momentum among those looking for stability and clarity in their portfolios. But what exactly is a unit investment trust, and how can it fit into your investment strategy?

This comprehensive guide will break down everything you need to know about UITs. You’ll discover how they work, their advantages and drawbacks, how they compare to mutual funds and ETFs, and the steps to invest confidently.

By the end, you’ll have the knowledge to decide if UITs belong in your portfolio. Let’s dive in and make your investment decisions more informed and effective.

What is a Unit Investment Trust (UIT)?

Understanding a unit investment trust is essential for today’s investors. As one of the three main types of investment companies, a unit investment trust offers a distinctive approach to portfolio management. Unlike mutual funds or ETFs, a unit investment trust comes with a fixed portfolio that typically consists of stocks, bonds, or a blend of both.

A unit investment trust issues redeemable units to investors during a single public offering. The portfolio is not actively managed after the initial selection, so what you buy at inception is what you own until the UIT’s predetermined termination date. If you’re new to these terms, resources like the Finance terms glossary can help clarify the basics.

Definition and Core Structure

A unit investment trust is a pooled investment vehicle that assembles a fixed portfolio of securities. These securities are carefully selected at the outset and remain unchanged throughout the trust’s lifespan.

UITs issue a finite number of units to investors. Each unit represents a proportional share of the trust’s holdings and entitles the investor to receive income and principal as the underlying securities generate returns or mature. The trust is designed to be passive, with no ongoing management or trading after launch.

Every unit investment trust comes with a set start and end date. When the termination date arrives, the trust’s assets are liquidated, and proceeds are distributed to unit holders. This structure offers predictability, so investors know exactly what they own and when they will receive their final payout.

How UITs Work: The Basics

A unit investment trust launches with a single public offering. Investors purchase units during this initial period, locking in their share of the fixed portfolio. After the offering closes, no new securities are added or removed from the trust.

The UIT follows a buy-and-hold strategy, aiming to minimize turnover and reduce transaction costs. Investors benefit from receiving a proportionate share of income generated, such as dividends or interest payments, as well as the return of principal when the trust matures.

For example, imagine a unit investment trust that holds 20 blue-chip stocks for a fixed two-year term. The investor receives all dividends paid during that period and, at maturity, their share of the portfolio’s value.

Types of UITs

There are three primary types of unit investment trust structures:

| Type | Focus | Typical Investor Goal |

|---|---|---|

| Equity UITs | Stocks or equity securities | Growth or sector exposure |

| Bond UITs | Fixed-income securities | Regular income, stability |

| Hybrid UITs | Mix of stocks and bonds | Balanced approach |

Bond UITs are especially popular, accounting for over 60% of UIT assets in 2023 (Investor.gov). Hybrid UITs have also gained traction as investors seek diversified strategies in a single product.

Each type of unit investment trust caters to different investment objectives, allowing flexibility based on risk tolerance and time horizon.

Key Features and Characteristics

A unit investment trust stands out for its transparency. Investors know all portfolio holdings at inception, with no surprises along the way. This predictability is ideal for those who value clarity and reduced uncertainty in their investment choices.

UITs are passively managed, resulting in lower portfolio turnover than mutual funds. This can lead to lower transaction costs and potentially fewer taxable events. Units are redeemable at net asset value (NAV), and some sponsors offer a secondary market for additional liquidity.

Key features include:

- Full disclosure of holdings up front

- Passive, buy-and-hold management

- NAV-based redemption options

- Predictable income and maturity timeline

These characteristics make a unit investment trust an attractive option for investors who prefer a hands-off, transparent approach.

Who Regulates UITs?

Every unit investment trust is overseen by the U.S. Securities and Exchange Commission (SEC) under the Investment Company Act of 1940. The SEC requires UITs to provide a prospectus at the time of offering and to issue regular disclosures throughout the trust’s life.

This regulatory oversight ensures that each unit investment trust operates with a high degree of transparency and investor protection, giving confidence to those considering UITs as part of their portfolio.

Pros and Cons of Investing in UITs

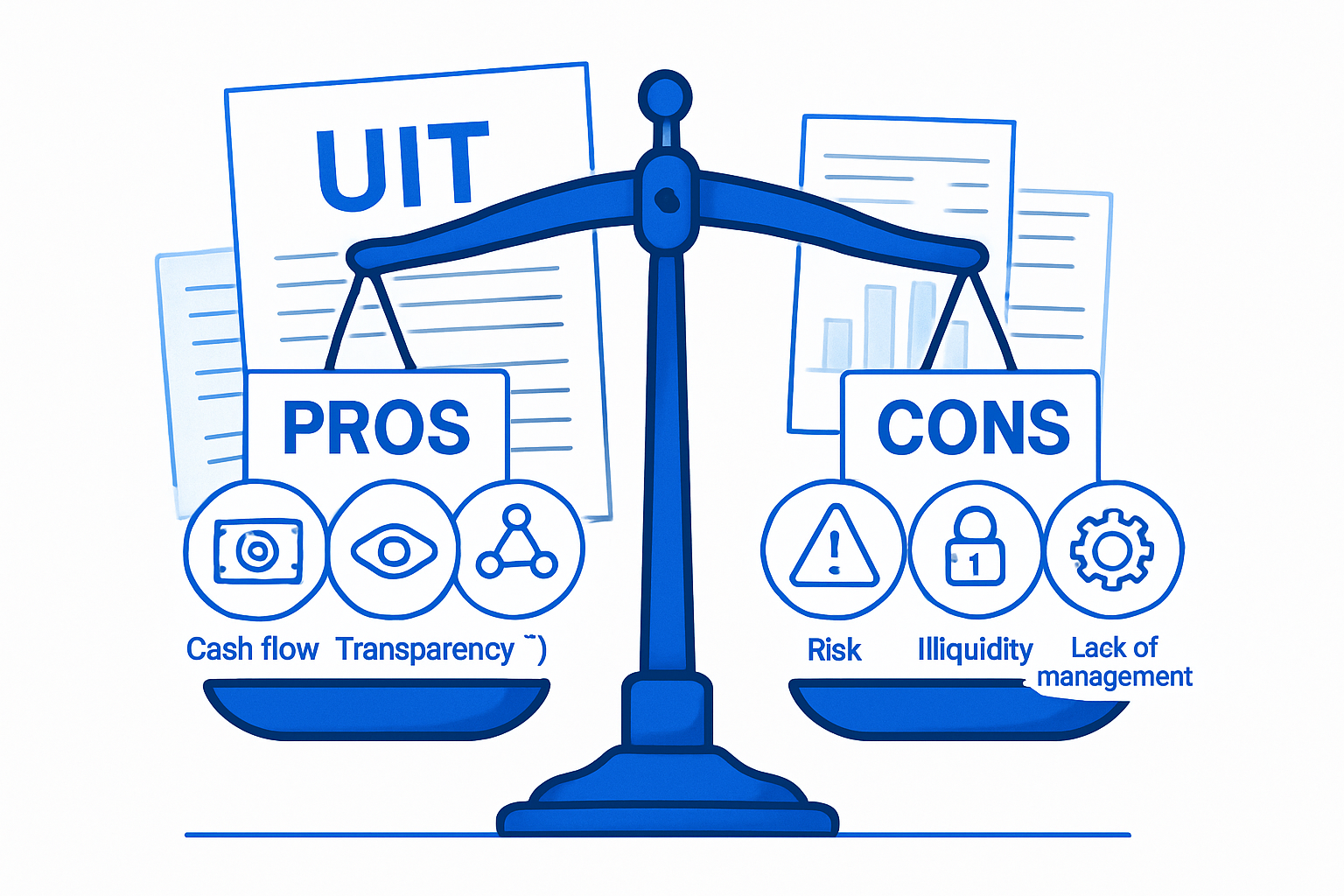

Understanding the pros and cons of a unit investment trust is essential before making any investment decisions. Like any financial product, UITs offer unique benefits but also come with notable risks. Let’s break down the key advantages and potential drawbacks so you can decide if a unit investment trust aligns with your portfolio objectives.

Advantages of UITs

A unit investment trust brings several compelling benefits for investors seeking transparency and stability.

- Predictable Portfolio: Since the holdings are fixed at inception, you know exactly what’s inside your unit investment trust throughout its life. There are no surprises or sudden changes.

- Lower Fees: UITs typically have fewer management expenses than actively managed funds, making them cost-effective for buy-and-hold investors.

- Diversification: By pooling assets into a single package, a unit investment trust can provide exposure to various sectors, asset classes, or geographic regions, which helps spread risk.

- Regular Income: Especially with bond UITs, investors often receive steady income distributions, making these products attractive during volatile or uncertain markets.

For instance, if you want predictable income and limited surprises, a bond-focused unit investment trust can be a smart choice. This structure is particularly appealing for those who value transparency and prefer a hands-off approach.

Drawbacks and Risks

Despite the benefits, a unit investment trust isn’t without its downsides.

- No Active Management: UITs are not actively managed, so the portfolio cannot adapt to changing market conditions. If the market shifts, your holdings remain the same.

- Principal Risk: The value of your investment may decrease if the securities in the UIT underperform.

- Limited Liquidity: After the initial offering, selling your unit investment trust units can be challenging. Secondary markets may be thin, and bid-ask spreads can be wider.

- Early Termination Risk: If underlying securities mature or are called before the UIT’s scheduled end date, the trust could terminate early, affecting your returns.

The average lifespan of a unit investment trust tends to range from 1 to 5 years, which may not fit all investment timelines. According to recent Unit Investment Trust Deposits April 2025 statistics, overall UIT market activity remains steady, but liquidity can still pose challenges for some investors. Always weigh these risks against your personal goals and risk tolerance.

Who Should Consider UITs?

A unit investment trust is best suited for investors who value transparency, predictability, and a passive strategy. If you have a medium-term investment horizon and want to know exactly what you own, a UIT can be a great fit.

UITs are not ideal for active traders or those who may need immediate access to cash. The fixed nature and limited liquidity of a unit investment trust mean you should be comfortable holding your investment until maturity.

If you’re seeking diversification, stable income, and a clear investment plan, a unit investment trust may help you achieve your objectives—just make sure it complements your broader portfolio.

How UITs Compare to Mutual Funds and ETFs

When evaluating investment options, understanding how a unit investment trust stacks up against mutual funds and ETFs is essential. Each structure offers unique features, management styles, and costs, so let’s break down the differences to help you decide which might fit your financial strategy.

UITs vs. Mutual Funds

A unit investment trust is fundamentally different from a mutual fund in several ways. UITs are passively managed, meaning once the portfolio is created, it remains unchanged for the trust’s lifespan. In contrast, mutual funds have active managers who buy and sell securities to achieve the fund’s objectives.

With a mutual fund, investors can buy or sell shares at the fund’s net asset value (NAV) at any time. In comparison, a unit investment trust issues units only during its initial public offering, and the portfolio is fixed from the start. This buy-and-hold approach means UITs typically have lower turnover rates than mutual funds, which may reduce transaction costs and tax consequences.

For example, if you want to avoid ongoing manager-driven changes and prefer knowing exactly what you own, a unit investment trust provides that predictability. Mutual funds, however, offer flexibility and ongoing professional oversight, which some investors may value more.

| Feature | UIT | Mutual Fund |

|---|---|---|

| Management | Passive (fixed portfolio) | Active or passive |

| Purchases | One-time (IPO) | Ongoing |

| Portfolio turnover | Low | Varies (often higher) |

| Transparency | High | Moderate |

UITs vs. ETFs

Both a unit investment trust and an ETF offer investors exposure to diversified portfolios, but their structures and trading mechanisms differ. ETFs are traded on exchanges throughout the day, allowing for real-time pricing and greater liquidity. Most ETFs are passively managed, tracking an index, but some are actively managed.

In contrast, a unit investment trust does not trade on an exchange (except for limited secondary markets). The portfolio in a UIT is always fixed, providing complete transparency from day one. UITs are also generally more tax efficient, as the buy-and-hold structure reduces capital gains distributions.

Market size is another key difference. ETF assets surpassed $7 trillion in 2023, reflecting their popularity and accessibility, while the unit investment trust remains a niche product. For a deeper look at market trends, see the Global Investment Trust Market Forecast 2025-2033.

If you value daily liquidity and trading flexibility, ETFs are likely a better fit. However, a unit investment trust may appeal to those seeking a defined portfolio and a set investment horizon.

Cost and Fee Comparison

Cost is a crucial factor when choosing between a unit investment trust, mutual funds, and ETFs. UITs typically charge a sales load at purchase, along with creation and redemption fees. These fees are upfront and often range from 1% to 4%, depending on the offering and sponsor.

By comparison, mutual funds and ETFs usually charge ongoing management fees, known as expense ratios. While these can add up over time, they pay for active management and administrative costs. For investors with a short- to medium-term, buy-and-hold strategy, a unit investment trust might be more cost-effective, as it avoids the drag of recurring management fees.

Here’s a quick snapshot:

| Cost Element | UIT | Mutual Fund | ETF |

|---|---|---|---|

| Sales load | Yes (usually up front) | Sometimes | Rarely |

| Management fee | Low/none | Ongoing | Ongoing (lower avg.) |

| Turnover costs | Low | Varies | Low |

Always review the prospectus for a full breakdown of costs before committing to any investment product.

Liquidity and Redemption

Liquidity is another key distinction between a unit investment trust, mutual funds, and ETFs. UIT units are redeemable at NAV through the sponsor, but liquidity is generally more limited after the initial offering period. Some sponsors maintain a secondary market for trading units, but prices there may differ from NAV due to supply and demand.

Mutual funds, on the other hand, offer daily liquidity at NAV, making it easy to buy or sell shares at any time. ETFs provide even greater liquidity, as they trade throughout the day on exchanges, often with tight bid-ask spreads.

If you need quick access to your funds or plan to trade frequently, a unit investment trust may not be the best fit. For example, investors may experience wider bid-ask spreads or delays in selling UIT units in the secondary market. Consider your liquidity needs and investment timeline before choosing a unit investment trust as part of your portfolio.

Step-by-Step Guide: How to Invest in UITs in 2025

Thinking about adding a unit investment trust to your portfolio in 2025? Here's a clear, actionable guide to help you get started. Whether you're new to UITs or just want a refresher, follow these steps to invest with confidence.

1. Assess Your Investment Goals

Before selecting any unit investment trust, take a close look at your personal financial objectives. Are you seeking regular income, long-term growth, or portfolio diversification?

Think about your risk tolerance and how much fluctuation you can handle. Consider your investment time frame—UITs are typically best for medium-term horizons, often between one and five years.

Ask yourself:

- Do I need predictable income or capital appreciation?

- How important is transparency in my holdings?

- Will I need access to my money before the UIT matures?

Matching a unit investment trust to your goals creates a foundation for a smoother investment experience.

2. Research Available UIT Offerings

With your goals in mind, explore the range of unit investment trust options on the market. Use sponsor websites, financial news, and your financial advisor to find UITs that fit your needs.

Carefully review each UIT's prospectus. Look at portfolio composition, sector or asset focus, fee structure, and termination date. Compare a technology equity UIT to a municipal bond UIT, for example, to see which better aligns with your objectives.

If you're considering bond UITs, learn about components like floating rate securities, as these can affect income stability and risk. Doing your homework now can help you avoid surprises later.

3. Understand Fees and Expenses

Every unit investment trust comes with costs, so it's essential to know what you'll pay. Common fees include sales charges (typically 1% to 4%), annual operating expenses, and creation/redemption fees.

Unlike mutual funds or ETFs, UITs often have upfront sales loads but generally lower ongoing expenses. Use the table below to compare:

| Fee Type | UITs | Mutual Funds | ETFs |

|---|---|---|---|

| Sales Charge | 1–4% (avg) | Varies | Usually None |

| Annual Expenses | Low | Varies | Low |

| Redemption Fees | Possible | Possible | Possible |

Understanding the cost structure of your chosen unit investment trust lets you make an apples-to-apples comparison with other investments.

4. Purchase Units Through a Broker or Advisor

Once you've chosen your unit investment trust, it's time to buy. UITs are typically purchased through a broker or financial advisor. Some platforms also offer UITs within retirement accounts, adding tax-advantaged flexibility.

Your broker will provide the necessary paperwork and walk you through funding your purchase. Make sure you understand the minimum investment requirement and confirm your order details before finalizing.

This step formalizes your commitment to the unit investment trust and sets the stage for the rest of your investment journey.

5. Monitor Your UIT Investment

After your purchase, don't just set it and forget it. Stay engaged by tracking income distributions, changes in net asset value (NAV), and any updates from your UIT sponsor.

Most unit investment trusts provide regular statements and notifications. Mark your UIT’s termination date on your calendar, as this is when your principal is returned and the trust dissolves.

Monitoring helps you understand how your unit investment trust is performing and keeps you ready for important milestones.

6. Redeem or Sell Units

When your unit investment trust reaches maturity, you'll typically receive your share of the trust's principal. If you need liquidity before then, you can redeem your units at NAV through the sponsor or look for a secondary market sale—though liquidity may be limited and prices can vary.

Consider the tax implications of selling before maturity, as gains or losses may apply. For example, you might sell a UIT unit ahead of schedule if your financial situation changes unexpectedly.

Being familiar with your exit options ensures you can adapt your investment strategy as life unfolds.

Key Trends and Innovations in UITs for 2025

In 2025, the unit investment trust landscape is evolving rapidly, responding to both investor demand and market innovation. Understanding these key trends will help you decide how a unit investment trust could fit into your portfolio this year.

Growth in Thematic and ESG UITs

Environmental, social, and governance (ESG) investing is no longer just a buzzword—it's now a major driver in the unit investment trust world. Thematic UITs, especially those focused on sustainability or social impact, are attracting both institutional and retail investors.

Recent launches include UITs tracking clean energy companies, diversity-focused firms, and sectors like water technology. Investors are drawn to the transparency and fixed nature of these portfolios, which align with their values and long-term goals. In fact, many see a unit investment trust as a way to directly support causes they care about, while still maintaining diversification and potential for steady returns.

Technology’s Impact on UIT Accessibility

Technology is reshaping how investors access and manage unit investment trust products. Digital platforms now offer streamlined research tools, real-time performance tracking, and online prospectuses, making it easier than ever to compare options and understand fee structures.

Mobile apps and robo-advisors also allow for direct purchasing and monitoring of UIT holdings. This increased transparency and ease of access are lowering barriers for first-time investors. As a result, more people can build custom portfolios that include a unit investment trust as a core component, all from their smartphones or laptops.

Regulatory Updates and Industry Changes

Regulation continues to play an important role in the unit investment trust space. Recent SEC guidance has focused on improving disclosure requirements and enhancing investor protection, particularly regarding fees and portfolio transparency.

The industry has seen an 8% increase in new UIT launches in 2024, reflecting both demand and confidence in regulatory oversight. Sponsors are responding by designing UITs with clearer objectives and simplified fee structures. These changes aim to help investors make informed decisions and reduce the risk of hidden costs within their unit investment trust choices.

Shifts in Investor Demographics

A significant shift is underway as millennials and Gen Z investors enter the market. These younger investors are using a unit investment trust to achieve diversification, especially within tax-advantaged accounts like IRAs and Roth IRAs.

They value transparency, predictability, and the ability to align investments with personal values—traits that UITs naturally provide. This demographic shift is pushing sponsors to innovate, offering more thematic and tech-enabled UITs to meet evolving preferences. As a result, the unit investment trust is becoming more mainstream among digital-native investors.

Market Outlook for UITs

Looking ahead, the performance of the unit investment trust sector will likely be influenced by interest rate trends, market volatility, and investor appetite for niche themes. Rising rates may boost demand for fixed-income UITs, while ongoing market uncertainty could drive interest in diversified, transparent portfolios.

To see how specific sectors are performing, check out the Top Performing Investment Trust Sectors H1 2025 for insights. With innovation in both products and accessibility, the unit investment trust remains a compelling option for investors seeking clarity and control in 2025.

Critical Considerations Before Investing in UITs

Before diving into a unit investment trust, it's crucial to take a step back and evaluate a few key areas. Understanding these factors will help you determine if a unit investment trust truly fits your investment strategy and risk tolerance.

Evaluating Portfolio Transparency and Holdings

When considering a unit investment trust, always review the portfolio at inception. UITs offer full transparency, so you know exactly what securities you’re investing in from the start.

Look at the sectors, countries, and issuers represented. Concentration in one area can increase risk. For example, if a UIT is heavy in financial stocks, a downturn in that sector could impact your returns.

It’s also wise to review metrics like the debt-to-equity ratio explained for underlying holdings, especially in equity or bond UITs. This helps gauge the financial health of the companies or issuers inside your UIT.

Assessing Fees, Loads, and Expenses

Fees can eat into your returns, so it’s essential to compare costs before purchasing a unit investment trust. Common expenses include sales loads, annual operating fees, and sometimes creation or redemption charges.

These costs are usually disclosed upfront, making it easier to evaluate whether the UIT is cost-effective. Compare UIT expenses to those of mutual funds and ETFs to see which option aligns best with your financial goals.

A table can help summarize key fee types:

| Fee Type | UITs | Mutual Funds | ETFs |

|---|---|---|---|

| Sales Load | Yes | Sometimes | Rarely |

| Management Fee | Low/None | Yes | Yes |

| Ongoing Expenses | Low | Varies | Low |

Always factor in the impact of fees on your overall investment return.

Understanding Tax Implications

Tax treatment is another important consideration for any unit investment trust. Income distributions from bond UITs may be tax-exempt if they hold municipal bonds, while equity UITs may trigger capital gains at maturity.

Be aware that you could owe taxes on income received throughout the UIT’s life. When the trust terminates, any gains are subject to capital gains tax.

For fixed-income UITs, you may also encounter concepts like a sinking fund, which can influence cash flows and tax timing. Always consult a tax professional to understand how UITs will affect your specific situation.

Liquidity and Exit Strategies

Liquidity is a key factor when investing in a unit investment trust. After the initial offering, some UITs may be harder to sell quickly than mutual funds or ETFs.

You can redeem your units at net asset value (NAV) with the sponsor, but secondary market trading may come with wider bid-ask spreads. It’s important to plan your exit strategy in advance so you’re not caught off guard if you need to access your funds early.

Consider your own liquidity needs and whether the UIT’s structure matches your timeline.

Aligning UITs With Your Broader Investment Plan

A unit investment trust should complement, not duplicate, your existing portfolio. Use UITs to target specific sectors, generate income, or diversify your holdings.

Make sure your UIT selection aligns with your overall goals and risk tolerance. Regularly review your investment mix as market conditions and personal needs evolve.

If you’re eager to really understand UITs—not just the basics, but the stories and historical trends that shape today’s investing landscape—you’re in the right place. We’ve covered the essentials, the pros and cons, and how UITs stack up against other options. Want to dig even deeper and see how history can guide smarter decisions in 2025? We’re building a platform that brings financial markets to life with interactive charts, AI-powered insights, and real context. If you’re curious and want to be part of shaping this experience, Join Our Beta.