Par Value Guide: Understanding Its Role in Finance 2025

Ever wondered why some stocks list a “par value,” even though it nearly never matches what you see on the trading floor? The concept of par value can seem confusing, but understanding it is crucial for investors, students, and finance professionals in 2025. This guide unpacks par value from its historical roots to its influence on today’s financial decisions. We will clarify its legal and accounting significance, examine its impact on stocks and bonds, and discuss regulatory trends shaping modern markets. Gain actionable insights and confidently interpret par value as you navigate the evolving world of finance.

What is Par Value? Definitions and Historical Context

Understanding par value is crucial for anyone navigating modern finance. At its core, par value is the nominal or assigned value a company gives to each share of stock or bond. While this figure might seem arbitrary, it carries specific legal and accounting implications that have evolved over time.

Defining Par Value: The Basics

Par value refers to the fixed value assigned to a share of stock or a bond by the issuing company. For stocks, this value is often set at a minimal amount, such as $0.01 or $1 per share, and is typically specified in the company’s charter or articles of incorporation. For bonds, par value is the amount the issuer agrees to pay at maturity, usually $1,000.

It is important to distinguish par value from face value and market value. While par value and face value are sometimes used interchangeably for bonds, market value represents the price at which a security trades in the open market, which can differ greatly from its par value. Companies assign par value for legal and accounting reasons, such as establishing a minimum price at which shares can be issued or determining the legal capital of the company.

Common par value amounts for stocks today range from a fraction of a cent to one dollar. However, the majority of corporations now opt for no-par value shares, reflecting a trend toward greater flexibility and simplified capital structures. For example, consider ABC Co., which might assign a $10 par value to its shares, even if the shares are trading at $50 in the market. This demonstrates how par value is often disconnected from actual trading prices.

According to industry statistics, most modern corporations assign either a very low par value or none at all. For a deeper dive into these distinctions and their significance, refer to Par Value of Stocks and Bonds Explained.

The Historical Evolution of Par Value

The origins of par value can be traced back to early corporate law, where it served as a protective mechanism for creditors. Historically, par value was designed to prevent companies from issuing shares below a set minimum price, thereby safeguarding the interests of those lending money to the business. This legal safeguard ensured that companies maintained a basic level of capital, reducing the risk for creditors.

Over time, the practical importance of par value diminished. As financial markets matured and regulations evolved, par value shifted from a meaningful benchmark to a largely symbolic figure. Throughout the 20th century, legal reforms in countries like the United States and Canada facilitated the rise of no-par value shares. This shift allowed companies greater flexibility in setting their capital structure and reduced administrative burdens.

For instance, the transition in North America saw most companies gradually move away from traditional par value concepts, reflecting broader changes in corporate finance. Historical events, such as economic crises and legal modernization, played key roles in shaping how par value is viewed and utilized today. Now, the focus is on transparency and substance over nominal values, aligning financial practices with the realities of modern markets.

Par Value in Stocks: Legal, Accounting, and Practical Implications

Understanding par value in stocks is crucial for anyone navigating corporate finance, equity issuance, or investment analysis. While often overlooked, par value shapes legal obligations, accounting practices, and practical decisions for companies and shareholders alike. This section unpacks its multifaceted role, revealing why par value still matters in 2025.

Legal Significance of Par Value for Shares

Par value began as a statutory requirement, designed to establish a minimum baseline for the value of shares issued by a corporation. In many jurisdictions, companies must specify par value in their articles of incorporation, embedding it in their corporate DNA. This nominal amount, often as low as $0.01 or $1 per share, is more than a formality—it represents the legal capital that cannot be distributed as dividends.

For shareholders, par value provides a measure of liability protection. In the past, it ensured that shares were not issued below a set price, safeguarding creditors from undercapitalized companies. Some countries still enforce minimum capital requirements based on par value, especially for banks and regulated industries.

Consider the following legal implications:

- Par value is recorded in the corporate charter and cannot be arbitrarily changed without shareholder approval.

- It defines the company's legal capital, which may not be returned to shareholders except under strict conditions.

- In cross-border contexts, differences in par value laws can impact mergers and acquisitions.

However, the significance of par value has diminished as many regions have shifted to no-par value shares. Still, understanding par value remains essential for compliance and legal risk management.

Accounting for Par Value: Balance Sheet Entries

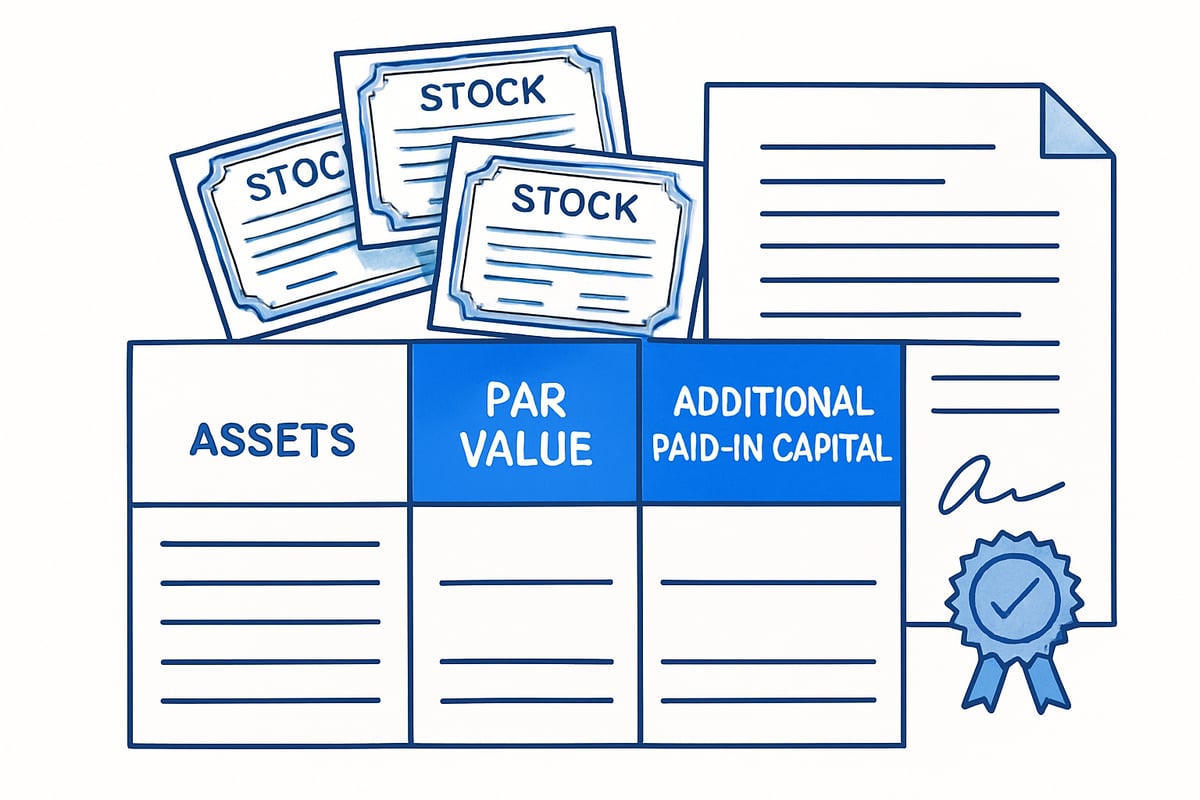

On the balance sheet, par value plays a key role in how a company's equity is structured and reported. When shares are issued, the par value is credited to the "common stock" or "share capital" account, while any amount received above par value is recorded as "additional paid-in capital" or "contributed surplus." This separation is fundamental for clear financial reporting.

For example, if ABC Co. issues 10,000 shares at a $10 market price with a $1 par value, the accounting entries would look like this:

| Account | Amount |

|---|---|

| Common Stock (Par Value) | $10,000 |

| Additional Paid-In Capital | $90,000 |

No-par value shares simplify this process, with all proceeds credited directly to share capital. However, statutory capital rules may still require some disclosure of minimum capital based on par value, especially in regulated sectors.

For a deeper dive into how par value shapes financial statements, see Par Value in Accounting for Stocks and Bonds.

Retained earnings, in contrast, are unaffected by par value and reflect accumulated profits. The distinction between par value, additional paid-in capital, and retained earnings is vital for accurate analysis and regulatory compliance.

Practical Relevance for Investors and Companies

Although par value rarely influences a stock's market price, it still affects key financial decisions. For companies, par value determines how much capital must remain in the business, potentially impacting dividend policies and restrictions on share buybacks.

During mergers or acquisitions, par value guides how shares are exchanged and valued in legal agreements. In buybacks, companies may need to adjust par value—sometimes through a capital reorganization—to facilitate the process. Stock splits also alter par value, typically reducing it in proportion to the increase in outstanding shares.

Investors should note common misconceptions about par value. It does not reflect a stock's intrinsic worth or market potential. Retail investors sometimes mistake high par value for high value, which can lead to poor investment decisions.

Key points to remember:

- Par value is a legal and accounting tool, not a measure of real value.

- Changes in par value can signal corporate restructuring or recapitalization.

- Understanding par value can help investors interpret balance sheets and corporate actions more effectively.

In summary, par value continues to underpin important legal, accounting, and practical frameworks, even as its influence on market price fades.

Par Value in Bonds: Face Value and Redemption

Bond markets use the concept of par value as a foundational reference point for both issuers and investors. Understanding how par value operates in the world of bonds is crucial for anyone analyzing fixed income securities. Let’s break down what par value means for bonds, how it impacts your returns, and what regulatory frameworks govern its use.

Understanding Par Value in Bond Markets

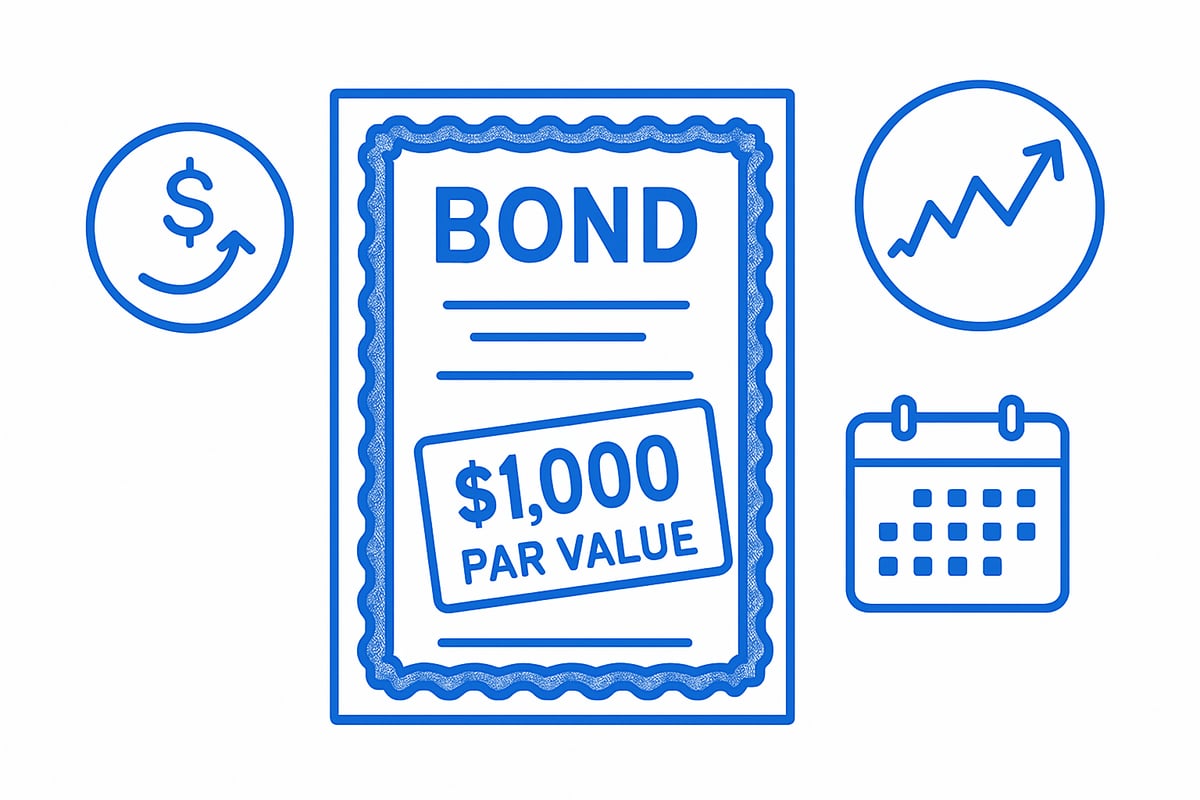

Par value in the bond market refers to the nominal or face value assigned to a bond by its issuer. Most commonly, this amount is set at $1,000 per bond, but it can vary depending on the type of bond or issuing entity. Par value is the amount the bondholder will receive when the bond matures, regardless of its price in the secondary market.

It’s important to distinguish par value from both the issue price and the market price. The issue price is what investors pay when the bond is first sold, while market price fluctuates based on interest rates and market demand. For example, if an investor purchases a $1,000 par value bond at $950, the bond is trading at a discount. If the same bond is bought at $1,050, it is trading at a premium. Despite these changes, par value remains the reference for redemption and interest calculations.

A quick comparison:

| Term | Definition | Example Value |

|---|---|---|

| Par Value | The nominal value repaid at maturity | $1,000 |

| Issue Price | Initial price paid by investor | $980 or $1,020 |

| Market Price | Current trading price | $950 or $1,050 |

Par value serves as the anchor for bond transactions and is mentioned in prospectuses and statements.

Role in Yield Calculations and Investment Decisions

Par value is central to how investors calculate returns from bonds. Coupon payments, or interest, are typically a fixed percentage of par value. For example, a bond with a 5% coupon rate and a $1,000 par value will pay $50 annually, regardless of the bond’s market price. This clarity allows investors to compare bonds with different structures.

Yield to maturity and current yield are both calculated with par value as a reference. When a bond trades below par, the yield to maturity rises, since the investor will receive the full par value at maturity, in addition to the coupon payments. Conversely, if a bond trades above par, the yield to maturity drops, as the investor pays more upfront but still only receives the par value at the end.

Institutional investors and portfolio managers closely monitor the relationship between market price and par value. Premium and discount bonds offer different risk-reward profiles, which are crucial for portfolio strategy. For example, during periods of rising interest rates, many bonds trade below par, creating opportunities for higher yields for new investors.

Regulatory and Disclosure Requirements

Regulators require issuers to disclose par value in bond prospectuses and financial documents. This disclosure ensures transparency for investors, allowing them to assess the promised return and redemption terms. Standardization of par value across global bond markets helps investors compare offerings from different countries and issuers.

In some cases, redemption of bonds involves mechanisms like sinking funds, which are structured plans for repaying bondholders at par value over time. For more detail, see the sinking fund and bond redemption explanation.

Cross-border investing can add complexity, as reporting standards may differ, but par value remains a central concept for understanding bond obligations and investor rights. Knowing where and how par value is disclosed helps investors avoid surprises at maturity.

Par Value and Modern Regulatory Trends (2025 Focus)

Understanding par value in today’s regulatory environment is crucial for anyone tracking global finance. Laws and best practices are evolving quickly, especially as financial markets become more interconnected and digital. Let’s explore how par value is changing, what it means for companies and investors, and where things are headed in 2025.

The Decline of Par Value: Global Perspectives

Recent years have seen a marked decline in the use of par value across major economies. Many countries, including the US and Canada, now allow or even encourage companies to issue no-par value shares. This shift is driven by a desire to modernize financial reporting and reflect the reality that par value rarely aligns with market value.

Some jurisdictions, however, still maintain par value as a legal requirement, particularly in parts of Asia and Europe. For example, certain EU countries require a minimum par value to protect creditors and preserve legal capital. Canada stands out for its flexible approach, allowing both par value and no-par value shares depending on the province. For a deeper dive into the key differences between par value and no-par value shares, see Par Value Stock vs. No-Par Value Stock.

This global patchwork means cross-border companies must carefully navigate local requirements, especially when raising capital or listing shares in multiple countries.

Par Value and Capital Maintenance Rules

Par value still plays a role in capital maintenance rules, which are designed to protect company creditors. Traditionally, par value set a baseline for legal capital, ensuring that companies did not issue shares below a certain amount. This was meant to safeguard creditors by establishing a minimum pool of funds that could not be distributed as dividends.

However, critics argue that par value is now largely symbolic. Modern regulations increasingly favor transparency, requiring companies to disclose actual paid-in capital and retained earnings rather than relying on nominal figures. This trend is particularly relevant for tech start-ups and growth companies, which often raise funds through no-par value shares to maximize flexibility.

Despite these changes, understanding par value remains important for compliance and for assessing a company’s capital structure, especially in regulated industries.

Digital Assets, Tokenization, and Par Value

The rise of digital assets and tokenized securities is reshaping how par value is defined and disclosed. Blockchain-based platforms enable companies to issue digital shares or bonds with customizable features, sometimes including or excluding par value as part of the asset’s metadata.

In these digital environments, par value can serve as a reference point for pricing, redemption, or voting rights, but its legal significance varies by jurisdiction. Best practices for tokenized assets include clear disclosure of par value, if applicable, to enhance investor protection and transparency.

Regulators are closely monitoring these developments, seeking to balance innovation with the need for reliable financial reporting. As digital securities grow in popularity, the treatment of par value will likely continue to evolve.

Future Outlook: What to Expect in 2025 and Beyond

Looking ahead, experts predict that par value requirements will continue to decline globally. More jurisdictions are expected to harmonize regulations, making it easier for companies to issue shares without a fixed par value. This could reduce administrative burdens and promote cross-border investment.

However, par value will not disappear entirely. In some cases, it will retain symbolic importance, serving as a historical or contractual reference. In others, it may still play a practical role in legal capital calculations or regulatory compliance.

For investors and analysts, staying informed about par value remains essential. Understanding how par value is handled in different markets will help you interpret financial statements and assess company risk. As the financial world becomes more digital and interconnected, the meaning of par value will continue to shift, making it a topic worth watching in 2025 and beyond.

Interpreting Par Value: What It Means for Investors and Analysts

Understanding par value is essential for anyone analyzing financial statements or making investment decisions. While it may seem outdated, its presence on balance sheets and in regulatory filings continues to influence how companies are evaluated and compared. Both seasoned analysts and new investors benefit from knowing how par value shapes the numbers behind the scenes.

Why Par Value Still Matters in Financial Analysis

Par value remains a foundational component in assessing a company's capital structure. It represents the minimum value assigned to shares and serves as the baseline for calculating legal capital. Analysts use par value to distinguish between the amount invested by shareholders and the minimum equity a company must maintain to comply with statutory requirements.

For example, book value per share is often calculated using par value data, providing insight into whether shares are trading above or below the company's net asset value. Understanding par value also helps analysts interpret additional paid-in capital and retained earnings, ensuring a clearer picture of shareholder equity.

For a deeper dive into how par value affects financial analysis and reporting, you can refer to this comprehensive Par Value - Definition, Example, Importance resource.

Red Flags and Opportunities: Reading Between the Lines

A sudden change in par value can signal more than just a technical adjustment. It may indicate a company is restructuring, recapitalizing, or preparing for significant corporate actions. For investors and analysts, these changes can reveal both risks and opportunities.

Some common red flags and opportunities include:

- Companies reducing par value to facilitate share buybacks or recapitalizations.

- Increases in par value that may hint at upcoming mergers or capital infusions.

- Unusually high or low par value compared to industry norms, which can suggest unique legal or financial strategies.

Whenever par value shifts, careful scrutiny is warranted. These adjustments can impact shareholder equity and signal deeper changes within a business.

Par Value in Mergers, Acquisitions, and IPOs

Par value plays a practical role in structuring deals during mergers, acquisitions, and initial public offerings. It determines the minimum value of exchanged shares, influencing the terms of share swaps and the overall deal structure.

During due diligence, analysts examine par value disclosures in prospectuses to ensure legal compliance and to evaluate how new shares will affect existing capital. In IPOs, par value must be clearly stated so investors understand the company's capital base and potential dilution risk.

A well-documented par value helps prevent misunderstandings during major corporate events, making it a critical detail for both buyers and sellers.

Investor Education: Avoiding Common Misconceptions

Many retail investors mistakenly believe par value reflects a stock's intrinsic worth. In reality, par value is a nominal figure with little connection to actual market value. It does not determine dividends, voting rights, or the future potential of an investment.

To use par value information wisely, consider these facts:

- Par value is mainly an accounting tool for legal and regulatory purposes.

- Low or no-par value shares are common and do not indicate weakness.

- Changes in par value often relate to administrative or strategic reasons, not sudden shifts in company value.

By understanding the true nature of par value, investors can avoid costly errors and make more informed portfolio decisions.

Par Value in Practice: Case Studies and Real-World Scenarios

Understanding par value in real scenarios sharpens your ability to interpret financial statements and market moves. Let’s break down how par value shapes decisions for startups, bond investors, and corporations in transition.

Case Study 1: Par Value and Share Issuance in a Tech Startup

Imagine a fast-growing tech startup preparing to raise capital. Instead of setting a high par value for its shares, the company opts for no-par value shares. This approach gives management more flexibility when pricing new share issuances. It also simplifies the legal process, as there’s no need to worry about shares being sold below par value.

When the company launched its IPO in 2024, investors focused on the business fundamentals, not the par value. The lack of par value did not hinder capital raising. In fact, it allowed the startup to issue shares at prices that matched market demand, driving a successful offering. This case highlights how par value can be more symbolic than practical in modern equity markets. For startups, no-par value shares often make it easier to attract early-stage investors and respond to market shifts.

Case Study 2: Bond Par Value and Market Volatility

In the bond market, par value plays a central role in how investors evaluate opportunities. For example, during the interest rate swings of 2022 and 2023, many bonds traded at a premium or discount to their par value. A $1,000 par value bond might be bought for $950 or $1,050, depending on market conditions.

Investors used par value as a reference to assess potential returns, knowing that coupon payments and final redemption would be based on this amount. Understanding the relationship between par value and market price helped them navigate risk and reward. To better grasp how par value connects with bond maturity and redemption, see Understanding maturity date in bonds. This knowledge was essential for both institutional and retail investors during volatile periods.

Case Study 3: Par Value Adjustments and Corporate Restructuring

Corporate restructuring often involves changes to par value, especially during recapitalizations or share consolidations. For instance, a manufacturing firm undergoing a turnaround in 2023 chose to reduce its par value per share. This move allowed the company to consolidate shares, shore up its balance sheet, and improve the appearance of shareholder equity.

On the balance sheet, the reduction in par value shifted amounts between common stock and additional paid-in capital accounts. Such adjustments can signal to the market that the company is proactively managing its capital structure. Analysts and investors watch these changes closely, as they may impact perceptions of financial health and future growth.

Lessons for Finance Professionals and Students

These case studies underscore why understanding par value is vital for anyone working in finance. Recognizing how par value affects share issuance, bond pricing, and restructuring can prevent costly misinterpretations. For students and professionals alike, studying par value deepens insight into legal capital and accounting practices.

To further explore definitions and concepts related to par value, visit the Key finance terms glossary. Mastery of par value helps you spot red flags, seize opportunities, and enhance your analytical toolkit.

Frequently Asked Questions About Par Value

Navigating par value can be confusing, especially for those new to investing or corporate finance. Here, we answer common questions to help you understand how par value fits into the bigger financial picture.

What is the difference between par value and market value?

Par value is the nominal amount assigned to a share or bond by the issuing company, often for legal or accounting purposes. Market value, on the other hand, is the current price at which a security trades in the open market. For example, a stock might have a par value of $1 per share but trade at $50. Par value rarely reflects the true worth of a security in today’s markets.

Why do some companies issue no-par value shares?

Companies may issue no-par value shares to gain flexibility in their capital structure and avoid outdated legal restrictions. Assigning no par value can simplify accounting, since there is no need to track a minimum legal capital based on par value. This trend has grown in recent years as regulations evolve and companies seek efficiency.

How does par value impact dividends and voting rights?

Par value itself does not directly determine dividends or voting rights. Instead, these rights are typically set out in a company’s charter or bylaws. However, par value may influence how much capital is legally available for dividends, especially in jurisdictions where legal capital rules are strict. Most modern companies set a low par value to avoid limiting their ability to pay dividends.

Is par value relevant for retail investors in 2025?

For most retail investors, par value is largely symbolic and rarely affects day-to-day investment decisions. However, understanding par value can provide insight into a company’s equity structure and help identify unusual situations, such as share consolidations or recapitalizations. In 2025, par value still appears in prospectuses and statements, so investors should know what it means.

Can par value change after a company is incorporated?

Yes, a company can change its par value after incorporation, but this typically requires shareholder approval and regulatory filings. Companies might reduce par value to facilitate share buybacks or consolidations. Any change in par value must be properly disclosed and reflected in the company’s financial statements.

What are the risks associated with low or high par value?

A very low par value can make it easier for companies to issue shares without breaching legal capital rules, but may raise questions about capital adequacy. Conversely, a high par value can restrict flexibility and complicate future financing. Investors should also consider how par value relates to debt-to-equity ratio and capital structure, as it affects calculations of shareholder equity.

How is par value disclosed in financial statements and prospectuses?

Par value is typically shown in the equity section of a company’s balance sheet, often in a line item such as “Common stock, $0.01 par value.” Prospectuses and annual reports also disclose par value per share for transparency. For bonds, the par value is stated as the principal amount to be repaid at maturity.

What should investors look for regarding par value in IPOs and bond offerings?

When reviewing IPO or bond offering documents, check the par value to understand the company’s capital structure and any legal capital requirements. For bonds, par value determines the amount you will receive at maturity. For stocks, a very high or very low par value may signal unique legal or strategic considerations that warrant further research.

Understanding par value is just one piece of the puzzle when it comes to analyzing financial markets, especially as we move into 2025. By looking at both the historical context and modern implications, you can better interpret market trends and make informed decisions. If you're interested in exploring how shifts like these have shaped finance over time, and want to see market stories come to life with interactive tools and expert insights, I invite you to join our beta and help us bring history to life. Let’s uncover the bigger picture—together.