Essential Guide to Risk-Weighted Assets for 2025

In 2025, navigating the world of risk-weighted assets is more vital than ever for banks, investors, and regulators. As global rules shift and economic uncertainty rises, understanding these assets can make or break financial strategies.

This guide will demystify risk-weighted assets, showing how they are calculated, why they matter, and what new regulations mean for your decisions.

Want to improve compliance, boost risk management, or plan smarter? Mastering these concepts is the key. Dive in for expert insights and practical tips to stay ahead in the evolving landscape of 2025.

Understanding Risk-Weighted Assets: Core Concepts

Understanding risk-weighted assets is fundamental for anyone navigating today’s financial landscape. At its core, risk-weighted assets represent the total value of a bank’s assets, adjusted for credit, market, and operational risks. This adjustment helps ensure that banks hold enough capital to cover potential losses, safeguarding both the institution and the broader financial system.

Unlike simply measuring assets at face value, risk-weighted assets assign different risk levels to various asset classes. Why? Not all loans or securities carry the same chance of default or loss. By using risk weighting, regulators and banks can better reflect the true risk profile of a bank’s holdings and maintain stability.

This concept didn’t emerge overnight. The journey began with the Basel I Accord in 1988, which introduced the first standardized approach to risk-weighted assets. Since then, Basel II and Basel III have refined these frameworks, expanding the risk types included and tightening capital requirements. The Basel Accords have pushed banks worldwide to adopt more sophisticated risk measurement and management practices.

A critical reason for focusing on risk-weighted assets is their direct link to regulatory capital requirements. Banks must maintain a minimum level of core capital, known as the Common Equity Tier 1 (CET1) ratio, relative to their risk-weighted assets. This ratio ensures that banks can absorb losses without threatening depositors or the financial system.

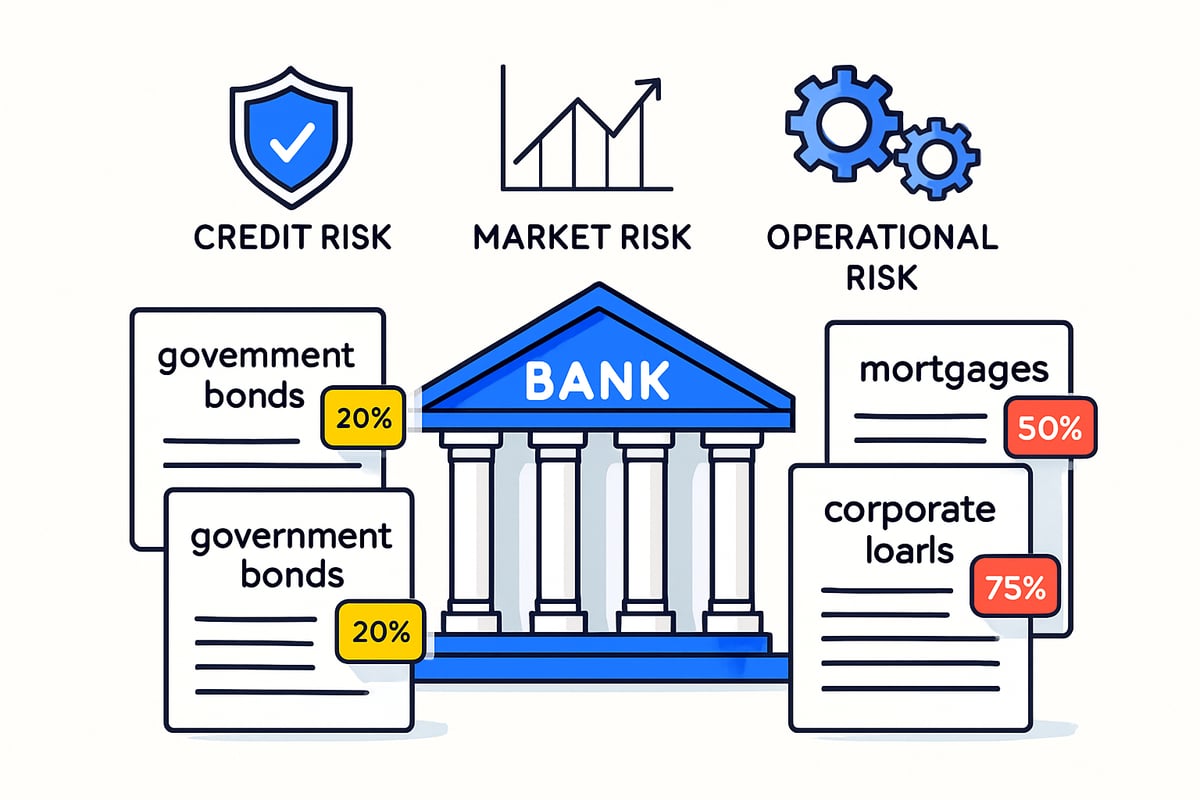

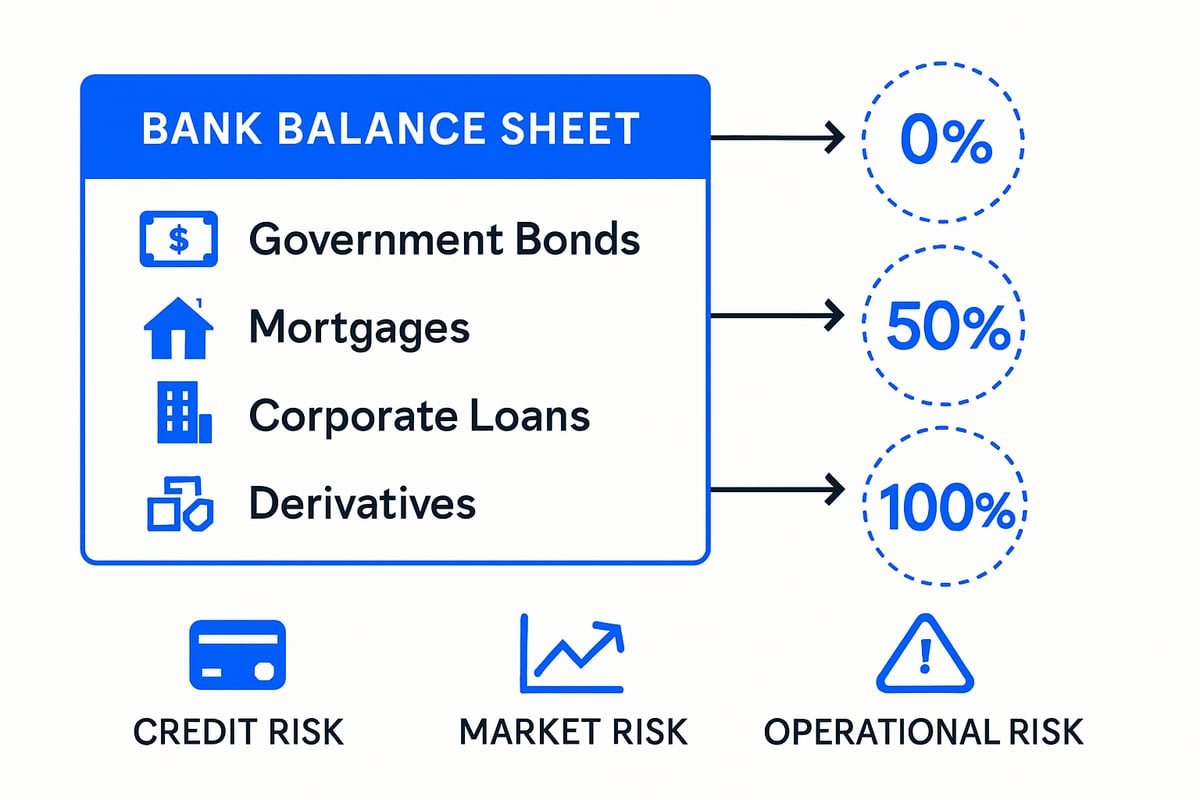

Let’s break down the key risks included in risk-weighted assets:

- Credit risk: The chance that borrowers won’t repay loans.

- Market risk: Potential losses due to changes in market prices.

- Operational risk: Threats from internal failures, systems, or processes.

For readers who want to dive deeper into these finance terms, the Key finance terms glossary provides clear definitions of all the concepts referenced here.

Different types of assets receive different risk weights. For example, government bonds are generally considered very safe, so under Basel III, they often carry a 0% risk weight. In contrast, corporate loans are riskier and usually receive a 100% risk weight. Mortgages typically fall somewhere in between, depending on factors like loan-to-value ratios and borrower creditworthiness.

Here’s a simple table to illustrate typical risk weights:

| Asset Type | Typical Risk Weight (Basel III) |

|---|---|

| Government Bonds | 0% |

| Residential Mortgages | 35% |

| Corporate Loans | 100% |

| Cash | 0% |

| Securitized Assets | 20%-1250% |

Why do these distinctions matter? Risk-weighted assets serve as the foundation for assessing a bank’s solvency and its ability to survive financial shocks. If a bank’s portfolio is heavily weighted toward risky assets, it must hold more capital, which can limit its growth and lending capacity.

Regulatory frameworks like Basel III have set the standard for minimum capital ratios. For instance, banks must maintain a CET1 ratio of at least 4.5% of risk-weighted assets, plus additional buffers for systemic importance or economic uncertainty.

In summary, mastering risk-weighted assets is essential for understanding how banks manage risk, comply with regulations, and protect the financial system. As global standards evolve, staying informed about these core concepts will be crucial for professionals, investors, and regulators alike.

How Risk-Weighted Assets Are Calculated

Calculating risk-weighted assets is a cornerstone of modern banking regulation. This process determines how much capital a bank must hold to cover potential losses, reflecting the true risk profile of its assets. Understanding these calculations is crucial for compliance, stability, and strategic decision-making.

Step-by-Step Overview of the RWA Calculation Process

Banks begin by categorizing all balance sheet and select off-balance sheet items. Each asset is assigned a risk weight, reflecting its credit, market, or operational risk. The total risk-weighted assets figure is the sum of each exposure multiplied by its corresponding risk weight.

For example, government bonds may receive a 0% risk weight, while unsecured corporate loans often carry a 100% risk weight. This approach ensures that safer assets require less capital backing, while riskier ones demand more.

Breaking Down by Risk Type

There are three major categories in risk-weighted assets calculations:

- Credit risk: The risk of borrower default, applied to loans, bonds, and other receivables.

- Market risk: The risk of losses due to market movements, relevant for trading portfolios and securities.

- Operational risk: The risk from internal failures, fraud, or external disruptions.

Each risk type is addressed separately, then aggregated to determine the total risk-weighted assets figure.

Standardized Approach vs. Internal Ratings-Based (IRB) Approach

Banks may use one of two primary methods for calculating risk-weighted assets:

| Approach | Who Uses It | How Risk Weights Are Determined |

|---|---|---|

| Standardized | Most banks | Set by regulators for each asset class |

| IRB | Large, sophisticated banks | Based on bank’s internal risk models, subject to regulatory approval |

The standardized approach applies regulator-assigned risk weights, making it straightforward but sometimes less sensitive to nuanced risk profiles. The IRB approach allows banks to use their own models, often resulting in lower capital requirements for well-managed portfolios.

Sample Calculation: Applying Risk Weights

Suppose a bank holds the following assets:

| Asset Type | Exposure ($) | Risk Weight | RWA ($) |

|---|---|---|---|

| Government Bonds | 100 million | 0% | 0 |

| Residential Mortgages | 200 million | 50% | 100 million |

| Corporate Loans | 150 million | 100% | 150 million |

Total risk-weighted assets: $0 + $100M + $150M = $250 million

This means the bank must hold capital based on $250 million, not the full $450 million in exposures.

Role of Credit Ratings and Internal Models

Assigning risk weights often depends on external credit ratings or internal assessments. For example, a highly rated corporate bond may get a lower risk weight than an unrated one. Under the IRB approach, banks develop sophisticated models to better capture the unique risk characteristics of their portfolios. Regulators require extensive validation of these models to ensure reliability.

Inclusion of Off-Balance Sheet Exposures and Derivatives

Risk-weighted assets calculations are not limited to on-balance sheet items. Off-balance sheet exposures, such as loan commitments or guarantees, are converted into credit equivalent amounts using regulatory conversion factors. Derivatives are assessed for their potential future exposure, which is then risk-weighted accordingly.

Impact on Minimum Capital Requirements

According to the Corporate Finance Institute, risk-weighted assets directly determine the minimum capital a bank must maintain. Regulatory ratios, such as the Common Equity Tier 1 (CET1), are calculated as a percentage of risk-weighted assets, not total assets. For a deeper dive into how regulatory changes are shaping these calculations, see the Basel III endgame: The next generation of risk-weighted assets.

Understanding the methodology behind risk-weighted assets is not just a regulatory requirement, but a strategic advantage. Mastering these calculations enables banks to optimize capital, meet evolving standards, and build resilience for the future.

Regulatory Frameworks and Standards for 2025

Navigating the evolving world of risk-weighted assets requires a clear understanding of the regulatory frameworks shaping global banking in 2025. These frameworks set the rules for how banks assess risk, determine capital reserves, and report their financial strength to regulators and investors.

Global Regulatory Frameworks: Basel III and Basel IV

At the heart of risk-weighted assets regulation are the Basel Accords, which provide international standards for measuring and managing risk in the banking sector. Basel III, finalized after the global financial crisis, introduced stricter definitions for capital, new liquidity requirements, and enhanced risk coverage. These rules require banks to hold a minimum Common Equity Tier 1 (CET1) capital ratio of 4.5% of risk-weighted assets, plus additional buffers for systemic importance and conservation.

Basel IV, often seen as an extension of Basel III, brings even more changes. It recalibrates standardized approaches, introduces output floors to limit the benefits of internal models, and raises the bar for operational risk calculations. The implementation of these frameworks is staggered, with key elements taking effect in 2025 for many major jurisdictions.

| Framework | Key Focus | Minimum CET1 Ratio | Implementation |

|---|---|---|---|

| Basel III | Capital, Liquidity, Risk | 4.5% + buffers | 2013–2025 |

| Basel IV | Standardization, Output Floor | 4.5% + buffers | 2025 onward |

Country-Specific Adaptations

While Basel standards set the global tone, each country tailors the rules to its own financial system. In Australia, APRA (Australian Prudential Regulation Authority) has issued its own guidance, aligning closely with Basel III and IV but adding additional reporting standards and capital buffers for local banks. The European Central Bank (ECB) oversees implementation across the Eurozone, ensuring a level playing field while managing unique regional risks.

In the United States, the Office of the Comptroller of the Currency (OCC) and the Federal Reserve adapt Basel rules to fit the complexities of American banking. Recent proposals, such as those from the FDIC, aim to revise capital requirements for large banks, directly impacting risk-weighted assets calculations and reporting.

Minimum Capital Requirements and Buffers

Risk-weighted assets are central to determining how much capital a bank must maintain to absorb unexpected losses. Regulators require banks to meet not just the minimum CET1 ratio but also to hold additional capital buffers for economic downturns or periods of increased systemic risk. These buffers include the Capital Conservation Buffer and, for the largest banks, the Countercyclical Capital Buffer and G-SIB surcharge.

According to the Basel III risk-based capital ratios increase, major international banks have steadily improved their capital positions, with average CET1 ratios rising as risk-weighted assets frameworks become more robust.

Recent and Forthcoming Regulatory Changes

The regulatory landscape for risk-weighted assets continues to evolve. Basel IV’s 2025 rollout will require banks to reassess their portfolios, update calculation models, and enhance data quality. This includes stricter treatment of credit risk, new operational risk formulas, and limits on the use of internal ratings-based approaches.

National regulators, like APRA, have released updated reporting forms and guidance to help banks transition smoothly. The ECB and OCC are also refining their supervisory approaches, increasing scrutiny on risk data aggregation and disclosure practices.

Stress Testing and Reporting Requirements

Stress testing has become a core part of risk-weighted assets oversight. Banks must regularly simulate adverse scenarios to gauge the impact on their capital ratios and risk-weighted assets. These exercises inform both internal risk management and regulatory reviews, ensuring resilience against shocks.

Transparent reporting is equally vital. Regulators require detailed disclosures on risk-weighted assets composition, methodologies, and any changes in calculation approaches. This transparency supports market discipline and helps investors make informed decisions.

APRA’s Guidance and Global Alignment for 2025

APRA’s 2025 guidance emphasizes accuracy, timeliness, and completeness in risk-weighted assets reporting. Australian banks are expected to align with Basel IV standards while meeting local prudential requirements. Similar efforts are underway in Europe and the US, where regulators are fine-tuning frameworks to reflect local market realities.

As the world heads into 2025, staying abreast of regulatory changes is essential for banks, investors, and policymakers. Understanding risk-weighted assets and their governing frameworks will remain a cornerstone of financial stability and strategic planning.

Practical Implications for Banks, Investors, and Regulators

Understanding risk-weighted assets is central to the daily operations and long-term strategies of banks, investors, and regulators. As financial markets become more complex, risk-weighted assets provide a standardized way to gauge the actual risk exposure of institutions, making them a cornerstone for prudent decision-making.

Banks rely on risk-weighted assets to fine-tune their capital allocation and risk management frameworks. By adjusting their portfolio mix, banks can optimize capital usage and ensure compliance with minimum capital requirements. For example, a shift toward lower-risk assets like government securities can reduce overall risk-weighted assets, freeing up capital for other business lines. Conversely, an increase in high-risk lending, such as unsecured corporate loans, raises risk-weighted assets and demands more capital, potentially constraining lending capacity.

The structure of risk-weighted assets directly influences how banks price their products and manage lending. Higher risk weights mean higher capital charges, which can drive up the cost of loans or limit the volume of lending to riskier sectors. This dynamic often leads banks to favor asset classes with lower regulatory risk weights, such as residential mortgages, over riskier commercial or SME loans. As a result, risk-weighted assets play a significant role in shaping credit availability and the broader economic landscape.

For investors, risk-weighted assets impact how they evaluate bank performance and risk profiles. A bank with a high proportion of risk-weighted assets relative to its total assets may be viewed as riskier, affecting valuations, dividend policies, and investor confidence. Changes in regulatory capital requirements or risk-weighted asset calculations can prompt banks to adjust dividend payouts or retain more earnings to bolster capital ratios, directly influencing shareholder returns.

Regulators use risk-weighted assets as a lens for systemic risk assessment and financial stability. Through stress tests and scenario analysis, supervisors evaluate how banks would fare under adverse economic conditions, focusing on whether capital buffers are sufficient relative to risk-weighted assets. Data from APRA and the Corporate Finance Institute highlight that, globally, average risk-weighted asset densities for large banks have trended between 35% and 55% over the past decade, reflecting evolving risk appetites and regulatory expectations.

Real-world examples show major banks responding to regulatory changes by rebalancing portfolios and strengthening capital positions. For instance, in anticipation of Basel IV, many banks have shifted assets or restructured exposures to optimize their risk-weighted assets and maintain competitive capital ratios. Industry experts have detailed these strategies in resources like Bringing Basel IV into focus, which provides insights into how banks are adapting to new risk-weighted asset frameworks for 2025.

Ultimately, risk-weighted assets serve as a bridge between regulatory compliance and sound financial management. By understanding their calculation and impact, banks can optimize capital use, investors can make informed decisions, and regulators can uphold financial system stability. As 2025 approaches, staying attuned to changes in risk-weighted assets frameworks will be crucial for all stakeholders.

Strategies for Optimizing and Managing Risk-Weighted Assets

Optimizing risk-weighted assets is a top priority for banks and financial institutions in 2025. As regulatory requirements evolve, effective management strategies can drive better capital efficiency, reduce costs, and improve financial resilience. Let’s explore proven approaches to managing risk-weighted assets, integrating technology, and aligning with best practices.

Best Practices for Optimizing Risk-Weighted Assets

Banks can improve risk-weighted assets by strategically managing their asset mix, focusing on risk mitigation, and optimizing capital structure. Careful selection and diversification of assets, such as government bonds, high-quality mortgages, and floating rate loans, can help maintain a healthy risk profile.

Reviewing the balance of fixed and floating rate instruments explained is crucial. Floating rate products often carry different risk weights, impacting the total risk-weighted assets calculation.

Key best practices include:

- Regularly assessing asset quality and risk weights.

- Shifting portfolios toward lower-risk assets where feasible.

- Setting clear risk appetite limits in alignment with business strategy.

By embedding risk-weighted assets analysis into daily decision-making, banks can proactively manage regulatory capital and stay ahead of compliance requirements.

Credit Risk Transfer Tools and Capital Planning

Transferring credit risk is another powerful way to optimize risk-weighted assets. Securitization and credit derivatives allow banks to transfer risk exposures off their balance sheets, directly reducing risk-weighted assets.

Effective capital planning also relies on understanding how changes in asset composition, credit risk transfer, and capital structure influence regulatory ratios. The debt-to-equity ratio overview is often assessed alongside risk-weighted assets to monitor overall capital adequacy.

Consider these strategies:

- Employing securitization to move riskier loans off balance sheets.

- Using credit default swaps to hedge portfolio risk.

- Rebalancing capital structure to maintain strong regulatory ratios.

These tools enable banks to respond flexibly to regulatory changes, optimize their capital base, and support sustainable growth.

Data Governance, ESG Integration, and Performance Metrics

Robust data governance is essential for accurate risk-weighted assets calculation. Banks must invest in data quality, internal controls, and transparent reporting to ensure compliance and avoid regulatory penalties.

Integrating ESG factors into risk assessment is becoming increasingly important. Environmental, social, and governance risks can affect asset quality and risk weights, impacting overall risk-weighted assets.

Performance metrics and benchmarking help track progress. Leading banks monitor:

- RWA density (risk-weighted assets as a percentage of total assets).

- Changes in portfolio composition after optimization efforts.

- Outcomes of ESG integration on risk-weighted assets.

By combining strong data management, ESG integration, and continuous performance review, banks can enhance their risk-weighted assets strategies and position themselves for regulatory and market success.

Frequently Asked Questions About Risk-Weighted Assets

Understanding risk-weighted assets is essential for anyone involved in banking, investment, or financial regulation. Here, we answer the most common questions to help you navigate the evolving landscape of risk-weighted assets in 2025.

What are risk-weighted assets and why do they matter?

Risk-weighted assets are a measurement used by banks and regulators to assess the riskiness of a bank's asset portfolio. Instead of treating all assets equally, each asset is assigned a risk weight based on its potential to cause losses. This approach ensures that banks hold enough capital to cover potential risks and maintain financial stability.

For example, government bonds often have a 0% risk weight, while unsecured corporate loans might have a 100% risk weight. By using risk-weighted assets, banks can better manage risk and regulators can more accurately judge a bank's solvency.

How do risk-weighted assets affect a bank’s capital requirements?

Banks are required to hold a certain amount of capital relative to their risk-weighted assets. This is known as the capital adequacy ratio. The higher the risk-weighted assets, the more capital a bank must set aside to protect against potential losses.

A simplified formula for the capital ratio is:

Capital Ratio = Bank Capital / Risk-Weighted Assets

Regulatory frameworks, such as Basel III, set minimum ratios to ensure banks remain solvent during economic stress.

What are the differences between the standardized and IRB approaches?

There are two main methods for calculating risk-weighted assets:

- Standardized Approach: Banks use fixed risk weights assigned by regulators based on asset type and credit ratings.

- Internal Ratings-Based (IRB) Approach: Banks develop internal models, subject to regulatory approval, to estimate risk weights based on their own risk assessments.

Larger banks often use the IRB approach for more tailored risk measurement, while smaller banks stick to the standardized method due to its simplicity.

How are off-balance sheet items treated in risk-weighted asset calculation?

Off-balance sheet exposures, such as guarantees, letters of credit, or unused loan commitments, must also be included in risk-weighted asset calculations. These items are first converted to credit equivalent amounts using conversion factors, then assigned appropriate risk weights.

This ensures that all potential risks, not just those directly on the balance sheet, are considered in determining the bank’s capital needs.

What changes are expected in risk-weighted asset regulation for 2025?

Significant updates are expected as Basel IV and national regulators revise capital requirements. For example, the FDIC has proposed new rules to revise regulatory capital requirements for large banks, which impact how risk-weighted assets are calculated. You can read more in the Proposal to Revise the Regulatory Capital Requirements for Large Banks.

These changes aim to make risk-weighted asset calculations more consistent and transparent across banks, enhancing financial stability.

How can banks ensure accurate and compliant risk-weighted asset reporting?

Accuracy in risk-weighted asset reporting relies on robust data collection, correct asset classification, and adherence to regulatory standards like those set by APRA and international bodies. Common best practices include:

- Regular internal audits and process reviews

- Detailed documentation of risk models and assumptions

- Ongoing staff training and compliance checks

Mistakes in reporting can result in regulatory penalties and reputational damage, so diligence is key.

What are the implications of risk-weighted assets for investors and market analysts?

Risk-weighted assets influence a bank’s capital strength, lending capacity, and risk profile. For investors, understanding risk-weighted assets helps in assessing a bank’s safety, dividend potential, and growth prospects. Market analysts also use risk-weighted asset trends to compare banks' risk management practices and anticipate regulatory or market shifts.

In summary, risk-weighted assets are a cornerstone of modern banking regulation and financial analysis. Staying informed on their calculation and impact is crucial for all stakeholders.

If you found this guide helpful for making sense of risk weighted assets in 2025, imagine what you could discover by exploring financial markets through a historical lens. We’re building a platform where you can dive into interactive charts, get AI powered summaries, and uncover the stories that shaped today’s market rules—perfect for investors, students, or anyone curious about financial history. Want to be part of this journey and help shape a tool that empowers smarter decisions? Join Our Beta and let’s uncover market insights together.