Paid-In Capital Guide: Understanding Equity in 2025

Equity is the backbone of every successful business in 2025, but truly understanding paid-in capital is what unlocks its real value. As companies compete for investments and growth, knowing exactly how paid-in capital works can set you apart from the crowd.

Many founders, investors, and finance professionals are confused by the concept or use it interchangeably with other equity terms. This guide will demystify paid-in capital, highlight its importance in today’s market, and provide you with actionable insights to master equity management for the year ahead.

What Is Paid-In Capital? Core Definitions and Concepts

Paid-in capital is a foundational concept in corporate finance, representing the total funds investors supply to a company in exchange for its stock. When a business issues new shares, the money investors pay to acquire those shares becomes paid-in capital. This influx of capital is vital for companies at every stage, from startups seeking seed funding to public corporations raising millions through stock offerings.

Understanding paid-in capital begins by distinguishing it from similar terms. While “contributed capital” and “capital contributions” are often used interchangeably, both refer to the money shareholders provide to a company in return for shares. The term “paid-in capital” commonly appears in financial statements and business discussions. All these terms essentially capture the same core idea: the funding a company receives directly from its owners, rather than from operating profits or loans.

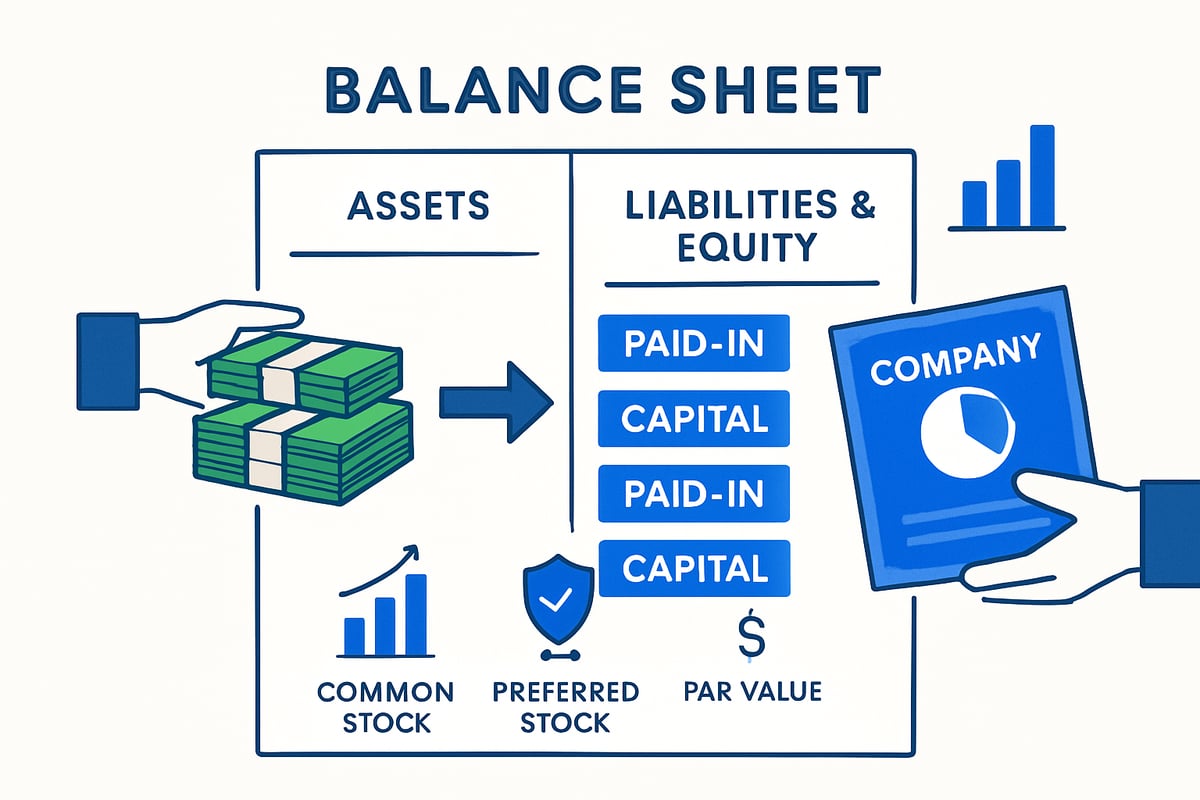

On the balance sheet, paid-in capital is a key component of shareholders’ equity. It appears in the equity section, usually broken down into “common stock,” “preferred stock,” and “additional paid-in capital.” For example, if an investor buys 1,000 shares at $10 per share, the total paid-in capital is $10,000. If the shares have a par value of $1 each, $1,000 is recorded as “common stock,” while the remaining $9,000 is “additional paid-in capital.”

To clarify, common stock and preferred stock represent the types of shares a company can issue, each with different rights and privileges. The par value is a nominal amount assigned to each share, typically very low, serving mainly as a legal formality. Any payment above par value is tracked as additional paid-in capital.

It’s important to differentiate paid-in capital from earned capital, also known as retained earnings. Paid-in capital comes from investors’ direct contributions, while retained earnings reflect profits the company has generated and kept over time. Both are crucial to a company’s equity structure, but they originate from different sources.

In private equity, the process works a bit differently. Paid-in capital is often funded gradually through capital calls, not as a lump sum. Investors commit a certain amount, and the fund manager requests portions over time as needed. This approach allows for flexibility and efficient capital deployment.

For those looking to deepen their understanding, the Paid-in Capital Definition page offers a comprehensive breakdown of the term and its applications in modern finance.

By grasping the basics of paid-in capital and its related concepts, investors and founders can better navigate equity structures, make informed decisions, and unlock greater value in their organizations.

The Role of Paid-In Capital in Equity Structure

Paid-in capital is the lifeblood of a company’s equity structure. Whether you’re a founder, investor, or finance professional, understanding how paid-in capital shapes a business’s financial backbone is essential for navigating today’s fast-paced markets.

Paid-in capital forms the core of shareholders’ equity. When investors purchase stock, the funds they provide become paid-in capital, directly boosting the company’s ability to operate and grow. For startups, this capital is often the first major influx of cash, fueling product development and early expansion. In IPOs, paid-in capital signals public confidence, while for established firms, it reflects ongoing trust from new and existing shareholders.

This capital serves as a vote of confidence. It reassures lenders and other investors that the company has genuine financial backing, not just paper promises. The amount of paid-in capital on the balance sheet can influence how a business is valued, especially in high-growth sectors. In 2025, tech IPOs are reporting record levels of paid-in capital, with the average new listing raising over $200 million in fresh equity. This trend highlights the growing importance of equity financing over debt.

Ownership dilution and voting rights are also shaped by paid-in capital. Issuing new shares increases paid-in capital but can dilute existing ownership unless managed carefully. Founders and early investors must balance the need for fresh capital with the desire to maintain control. Voting power is typically tied to the number of shares held, so each capital raise impacts the distribution of influence within the company.

The role of paid-in capital varies between private and public companies. In private firms, capital is often raised through periodic funding rounds, with ownership stakes negotiated directly. Public companies, on the other hand, can access broader markets through stock exchanges. The table below summarizes key differences:

| Feature | Private Company | Public Company |

|---|---|---|

| Capital Raising | Private placements, rounds | Public share issuance, IPOs |

| Ownership Structure | Concentrated, negotiated | Widely held, traded shares |

| Reporting Requirements | Less frequent, less public | Regulated, frequent disclosure |

Regardless of company type, paid-in capital is a springboard for growth. Companies use this equity to fund acquisitions, invest in R&D, and expand into new markets. In 2025, many firms are leveraging paid-in capital to accelerate digital transformation and sustainability initiatives.

Accurate reporting of paid-in capital is crucial. Both GAAP and IFRS require companies to disclose paid-in capital within the shareholders’ equity section, ensuring transparency for investors and regulators. For a deeper dive into how accounting standards treat paid-in capital, see Paid-In Capital Accounting Standards.

Paid-in capital also plays a key role in determining market capitalization. While market cap reflects the total value of outstanding shares at current prices, paid-in capital shows the actual funds invested by shareholders. Together, these figures provide a clearer picture of a company’s financial health and growth potential.

Looking ahead, the strategic use of paid-in capital will continue to shape how companies compete and thrive in 2025’s dynamic equity landscape.

Calculating and Reporting Paid-In Capital in 2025

Understanding how to calculate and report paid-in capital is foundational for anyone managing or analyzing equity in 2025. With evolving regulations and the growing complexity of equity structures, getting this right can make the difference between transparent, investor-friendly reporting and costly compliance errors.

How to Calculate Paid-In Capital: Step-by-Step

Calculating paid-in capital begins with identifying the total funds investors have contributed in exchange for company stock. The most common method focuses on the sum paid by investors for shares, split into common stock, preferred stock, and additional paid-in capital.

Here’s the basic formula:

Additional Paid-In Capital = (Number of shares issued x issue price) – (Number of shares x par value)

For example, if a company issues 1,000 shares at $10 each with a par value of $1, the additional paid-in capital is $9,000. The total paid-in capital would be $10,000, combining both the par value and excess over par. For a deeper dive, see Additional Paid-In Capital Explained.

Where to Find Paid-In Capital on Financial Statements

Paid-in capital appears in the shareholders’ equity section of the balance sheet. It is typically broken down into line items such as common stock, preferred stock, and additional paid-in capital. Look for these entries under the equity section, usually just after liabilities.

Both GAAP and IFRS require companies to clearly disclose paid-in capital components. This helps investors and auditors quickly assess how much equity funding the company has received from shareholders, separate from retained earnings or other reserves.

Reporting Paid-In Capital: Private Companies and Startups

For private companies and startups, tracking paid-in capital can be more nuanced. Unlike public firms, these entities may have rolling capital contributions, convertible notes, or non-traditional equity instruments. Accurate record-keeping is crucial, including detailed ledgers of every capital inflow, share issuance, and any conversions.

Startups should document each founder and investor contribution, the class of shares issued, and any subsequent equity events. This ensures paid-in capital is transparent during fundraising or due diligence.

Importance for Audits, Fundraising, and Compliance

Accurate reporting of paid-in capital is essential for audit readiness, successful fundraising, and regulatory compliance. Auditors often scrutinize equity accounts to confirm all contributions are properly recorded.

When preparing for an IPO or major investment, clear documentation of paid-in capital reassures investors and regulators. Misstatements can result in delays, penalties, or lost deals.

Common Mistakes in Reporting Paid-In Capital

Companies often make avoidable errors when reporting paid-in capital. Here’s a quick summary:

| Mistake | How to Avoid |

|---|---|

| Mixing up paid-in with retained earnings | Keep separate ledgers for each equity component |

| Ignoring par value in calculations | Always subtract par value from total proceeds |

| Overlooking non-cash contributions | Record all forms of capital, not just cash |

| Failing to update after buybacks | Adjust records promptly after equity changes |

Being meticulous with paid-in capital reporting not only ensures compliance but also builds trust with investors and stakeholders.

Paid-In Capital in Practice: Real-World Examples and Case Studies

Understanding paid-in capital becomes much clearer when we look at real-world scenarios. By examining how startups, private equity funds, and public companies handle paid-in capital, you can see its practical impact on business growth and investment decisions.

Tech Startup Equity Raise: Anatomy of Paid-In Capital

Imagine a tech startup raising $5 million by issuing 500,000 shares at $10 each. Investors’ cash injection is recorded as paid-in capital. If the shares have a par value of $1, then $500,000 goes to common stock, and $4.5 million is additional paid-in capital (APIC). The company’s equity section now shows both these components, along with retained earnings, which track profits over time.

Startups rely on paid-in capital to fund product development, hire talent, and fuel early growth. For founders, structuring the equity raise carefully can help maintain control while attracting top investors. Investors, in turn, assess paid-in capital to gauge the startup’s financial backing and growth potential.

Private Equity Fund Lifecycle: Paid-In Capital in Action

Private equity funds operate differently from startups. Here, investors commit a total amount, but the fund managers call capital gradually as investment opportunities arise. For example, if a fund has €20 million committed and €12 million paid-in capital, the remaining €8 million is still unfunded. The timing of capital calls directly affects fund performance metrics.

Paid-in capital plays a central role in tracking how much has actually been invested. Limited partners (LPs) monitor these figures closely, as their returns, such as IRR and DPI, depend on when and how much capital is deployed. For more on how paid-in capital is managed in private equity, see this Paid-In Capital in Private Equity resource.

Public Company Evolution: Paid-In Capital Over Time

Public companies like Apple and Tesla provide excellent examples of how paid-in capital evolves. Early in their histories, both companies raised substantial funds through stock offerings, creating a strong base of paid-in capital. Over the years, as market capitalizations grew, the proportion of new paid-in capital from additional share issuances shrank compared to retained earnings from profits.

Paid-in capital can also decrease in importance as companies mature and rely more on reinvested earnings. However, during IPOs or secondary offerings, understanding paid-in capital is crucial for investors evaluating a company’s financial health. For definitions of related terms, check out the Key finance terms glossary.

Lessons and Sector Data: Paid-In Capital in 2025

Recent equity market events in 2025 show both successful and failed capital raises. For instance, tech IPOs averaged $200 million in paid-in capital, while biotech firms reported closer to $80 million. Companies use paid-in capital not just for growth, but also to repay debt or return value to shareholders through dividends and buybacks.

Investors care about paid-in capital because it reflects the level of confidence others have in the business. When analyzing sectors, higher paid-in capital can signal robust investor interest, but it’s essential to consider how these funds are used for sustainable growth.

Paid-In Capital Strategies for Investors, Founders, and Finance Teams

Unlocking the full potential of paid-in capital requires a strategic approach from all stakeholders—founders, investors, and finance teams alike. In 2025, a thoughtful plan for managing paid-in capital can be the difference between growth and stagnation.

Structuring Equity Raises: Best Practices for Founders

Founders face critical decisions when structuring equity raises. Setting the right terms for paid-in capital can help retain control and prevent excessive dilution. Key steps include:

- Defining clear share classes, such as common and preferred stock, to align investor interests.

- Setting realistic valuations and par values to ensure transparency in paid-in capital reporting.

- Timing capital infusions to match growth milestones, reducing unnecessary dilution early on.

By carefully managing paid-in capital, founders can maximize long-term influence while still attracting the capital needed for expansion.

Investor Strategies: Evaluating Paid-In Capital and Company Health

For investors, understanding paid-in capital is essential for assessing company risk and potential returns. Paid-in capital shapes ownership percentages, impacts voting rights, and provides insights into how much founders and early backers have invested. One vital metric influenced by paid-in capital is the debt-to-equity ratio explained, which helps investors gauge a company's leverage and financial stability.

Investors often compare paid-in capital levels with retained earnings to determine whether a company relies more on external funding or on sustainable operations. Reviewing trends in paid-in capital over time can also signal company growth or over-reliance on equity raises.

Private Equity LPs: Monitoring Paid-In Capital and Fund Performance

Limited partners (LPs) in private equity funds must track paid-in capital closely. Unlike public companies, private equity funds receive paid-in capital through capital calls over time. Monitoring these contributions helps LPs measure their exposure, forecast future commitments, and track fund performance using metrics like IRR and TVPI.

Staying updated on capital call schedules and understanding the timing of paid-in capital is crucial for optimizing returns and managing liquidity.

Common Pitfalls and Tax Planning for Paid-In Capital

Relying too heavily on paid-in capital, without building strong operating earnings, can weaken a company's foundation. Companies should balance equity infusions with efforts to grow retained earnings. Additionally, founders and investors must consider the tax implications of paid-in capital contributions, as different jurisdictions may treat these inflows differently.

Proper documentation and awareness of local regulations are vital to avoid compliance issues and unexpected tax bills.

Finance Teams: Audits, Due Diligence, and Forecasting

Finance teams play a pivotal role in ensuring paid-in capital is accurately recorded and reported. Preparing for audits means maintaining clear records of share issuances, capital calls, and shareholder agreements. Due diligence processes for fundraising or acquisitions often scrutinize paid-in capital entries for accuracy.

Forecasting future capital needs requires scenario analysis, modeling how additional paid-in capital will affect dilution, control, and financial ratios. This proactive approach helps companies stay agile and prepared for new opportunities.

A robust paid-in capital strategy empowers founders to drive growth, investors to make informed decisions, and finance teams to maintain compliance and transparency. As the landscape evolves in 2025, mastering these strategies ensures all stakeholders can harness the real value of paid-in capital.

Now that you have a clearer picture of paid-in capital and its role in shaping equity strategies for 2025, why not take your understanding one step further? With so many market trends and historical patterns to learn from, having the right tools can make all the difference. If you are curious about how companies like those in our examples have navigated equity challenges or if you want to spot opportunities before they hit the headlines, I invite you to Join Our Beta and be among the first to explore our interactive platform. Let’s decode history to sharpen your edge for the future!