Option Premium Guide: Mastering Strategies for 2026

Are you ready to uncover the secrets that drive today’s most successful traders? Understanding the option premium is the first step to gaining a significant advantage in 2026’s rapidly changing markets.

This guide breaks down the option premium for both beginners and experienced traders. You’ll learn what an option premium is, how it’s calculated, the main factors that influence its value, and proven strategies to maximize your returns. We’ll also explore key trends shaping the future of option trading.

Prepare to master the skills top traders use, stay ahead of market shifts, and confidently navigate the evolving world of options.

Understanding Option Premiums: The Foundation

Understanding the option premium is essential for anyone entering the world of options trading. The option premium is the price buyers pay and sellers receive for an options contract, and it forms the backbone of every options transaction. But what makes up this cost, and how does it shift as markets evolve?

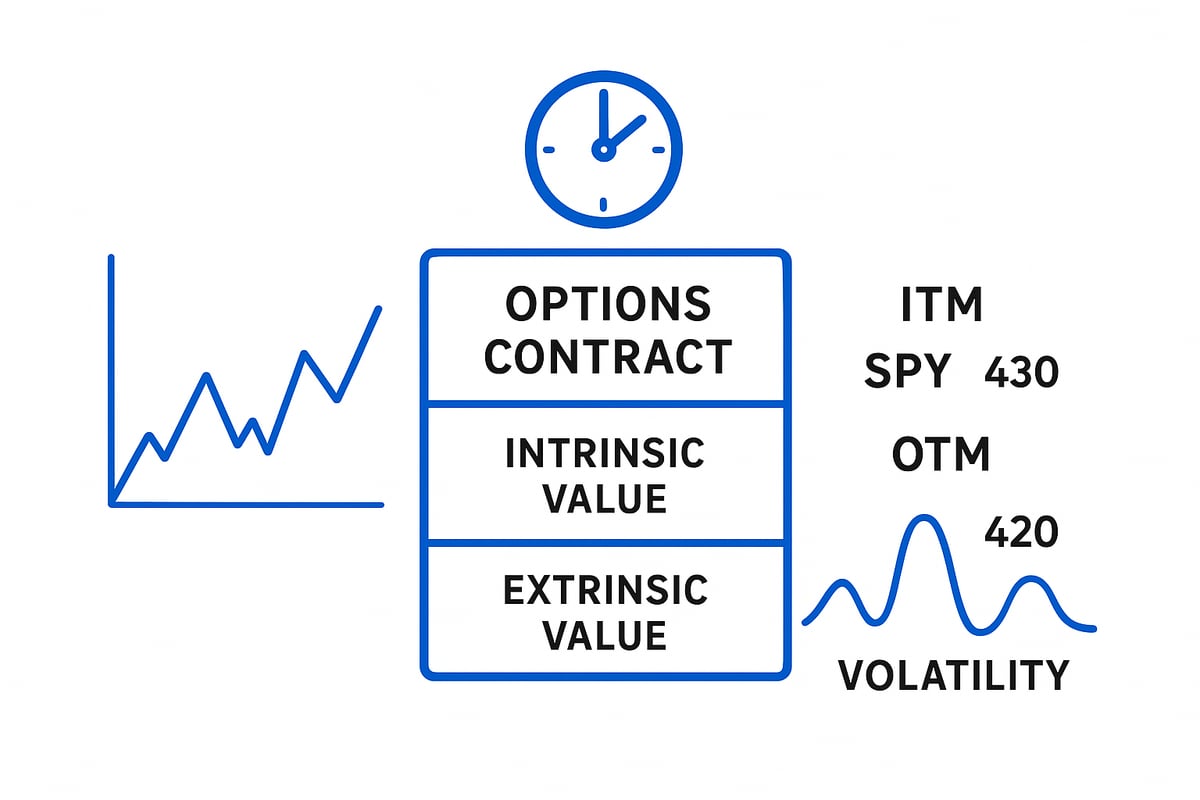

What Is an Option Premium?

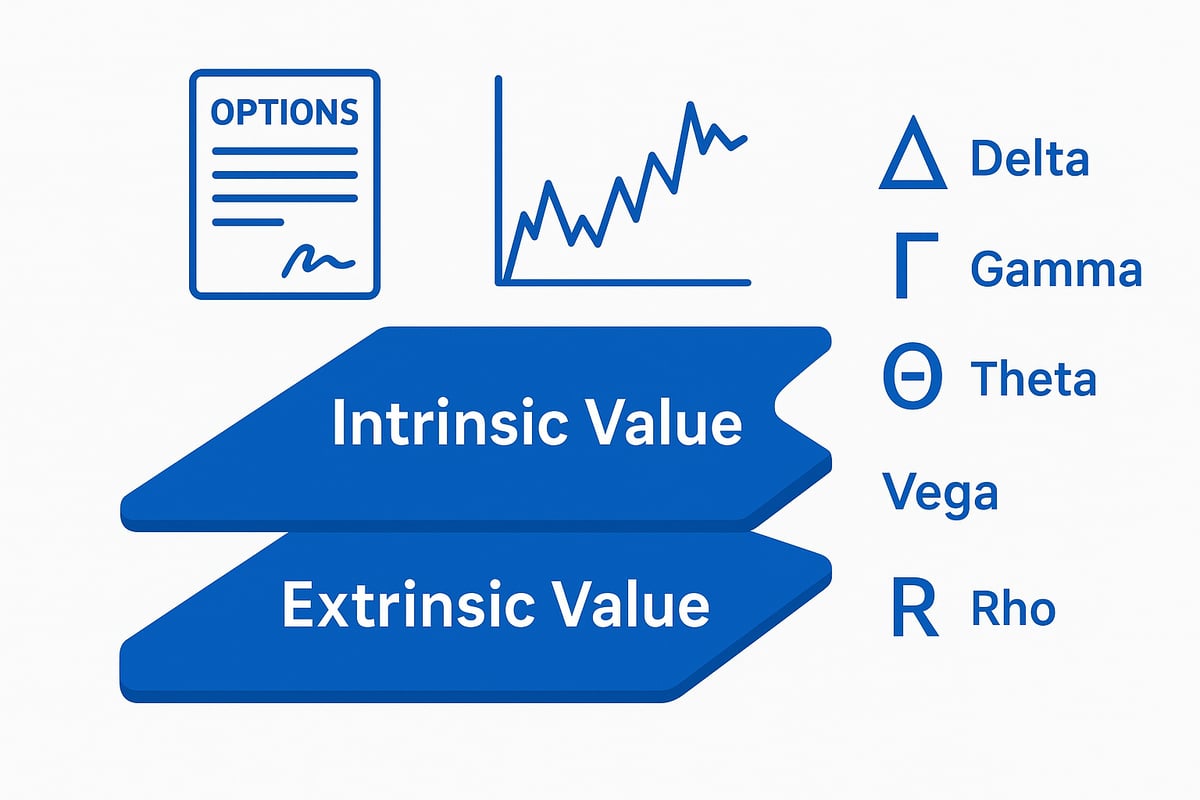

The option premium is the core price tag attached to every options contract. It consists of two main components: intrinsic value, which reflects the immediate value of the contract if exercised, and extrinsic value, which captures time left until expiration and market volatility.

For example, consider SPY call and put options. A call option that is in the money (ITM) with a strike price below the current SPY price will have a higher option premium than a call that is out of the money (OTM). This is because ITM options have intrinsic value, while OTM options rely solely on extrinsic value.

Option premiums are always changing. Unlike fixed prices, they respond to shifts in the underlying asset, time until expiration, and implied volatility. At expiration, the option premium equals the intrinsic value, but before expiration, it includes extrinsic value too.

From a trading perspective, the option premium determines potential profit or loss for both buyers and sellers. Buyers pay a debit to open a position, while sellers receive a credit. Sellers hope the option expires worthless, capturing the full premium, while buyers seek a move in the underlying that makes the premium rise.

As noted in trading communities, such as Reddit, option premiums fluctuate constantly with price, volatility, and time. For a deeper dive into how these components interact, explore this guide on Option Premium Calculation Methods.

Option Premiums and Moneyness

Moneyness describes the relationship between the option’s strike price and the underlying asset’s price. There are three key categories:

| Moneyness | Description | Premium Level | Probability ITM at Expiry |

|---|---|---|---|

| In-the-Money | Strike below (call) or above (put) market | Highest | Highest |

| At-the-Money | Strike equals market price | Moderate | Moderate |

| Out-of-the-Money | Strike above (call) or below (put) market | Lowest | Lowest |

As the strike price moves away from the underlying, the option premium decreases. For instance, viewing a SPY options chain, you’ll see that ITM calls command higher premiums, while OTM calls have lower values, reflecting only extrinsic value.

ITM options always carry higher premiums due to their intrinsic value. However, OTM options still hold value because of the time until expiration and market volatility. The chance for the underlying to move in your favor, even slightly, means there’s always at least some premium until the option expires.

Understanding where your contract sits on the moneyness spectrum is vital for predicting how your option premium may change. Each shift in price, time, or volatility can move an option from OTM to ITM, altering both its value and risk profile.

The Mechanics of Option Premium Calculation

Understanding how an option premium is calculated is essential for successful options trading. Both buyers and sellers need to know what goes into the price of an option and how each piece can impact their returns or risks.

Intrinsic Value Explained

The intrinsic value is the base layer of every option premium. It reflects the real, immediate value an option would have if exercised right now. For call options, the formula is simple: max(0, underlying price – strike price). For puts, it’s max(0, strike price – underlying price).

Let’s look at an example using ABC stock trading at $100 per share:

| Strike Price | Option Type | Premium | Intrinsic Value |

|---|---|---|---|

| $95 | Call | $7 | $5 |

| $100 | Call | $3 | $0 |

| $105 | Call | $1 | $0 |

| $105 | Put | $6 | $5 |

| $100 | Put | $2 | $0 |

Notice that only in-the-money (ITM) options have intrinsic value. Out-of-the-money (OTM) options have $0 intrinsic value, but their option premium still holds value due to other factors. At expiration, the option premium equals intrinsic value, but before that, time and volatility matter, too.

Early exercise decisions, especially with American options, depend on intrinsic value. If an option is deep ITM, the premium becomes almost entirely intrinsic as expiration nears.

Extrinsic Value Unpacked

Extrinsic value is everything in the option premium above intrinsic value. This part includes time value, implied volatility, anticipated dividends, and prevailing interest rates. The further an option is from expiration, the larger its extrinsic value—this is why longer-dated options cost more.

As expiration approaches, extrinsic value decays steadily, a process known as time decay or theta. For example, compare SPY put options with 30 days to expiration versus those with just 2 days left. The 30-day option premium is much higher, primarily due to the extra extrinsic value. By the final days, most OTM options have a zero bid, as extrinsic value vanishes.

Sellers often look to capture high extrinsic value by focusing on periods of increased volatility or longer timeframes. This approach allows them to maximize the option premium received, as more of the price is composed of extrinsic value rather than intrinsic.

Option Pricing Models

Pricing models help traders and institutions determine a fair option premium based on underlying asset price, time, volatility, and other variables. The Black-Scholes model is widely used for European options, providing a mathematical framework for calculating theoretical values. The Binomial model is preferred for American options, as it can account for early exercise features. For more complex derivatives, Monte Carlo simulations are used to estimate potential option premium outcomes.

As an example, SPX (European-style) options are often priced using Black-Scholes, while SPY (American-style) options are frequently modeled with the Binomial Options Pricing Model. Professional traders may prefer European options to avoid early assignment risks, especially when managing large portfolios.

By understanding these models, traders can better anticipate how market changes will influence an option premium and adjust their strategies accordingly.

Key Factors Influencing Option Premiums in 2026

Understanding the key factors that influence option premium is essential for any trader aiming to excel in 2026. As markets evolve, these drivers will shape the opportunities and risks you face when trading options. Let’s break down the core elements that impact option premium and how you can leverage them for smarter trading decisions.

Time Until Expiration (Theta)

Time is a critical component in determining option premium. Every option contract has a limited lifespan, and as the expiration date approaches, its extrinsic value steadily declines. This process, known as time decay (or theta), accelerates in the final weeks before expiration.

For example, a 0DTE (zero days to expiration) SPY option will have a much lower premium than a 30-day contract, even if the strike price is the same. Sellers often target options with 30 to 45 days to expiration, aiming to capture the optimal balance between premium received and manageable risk.

The table below illustrates how option premium decreases as expiration nears:

| Days to Expiry | Extrinsic Value | Option Premium |

|---|---|---|

| 45 | High | $4.50 |

| 15 | Medium | $2.10 |

| 1 | Low | $0.30 |

The key takeaway is that managing time exposure is crucial for both buyers and sellers in the options market.

Implied Volatility (Vega)

Implied volatility (IV) represents the market’s expectations of future price swings. When IV rises, so does the extrinsic value embedded in option premium. This makes volatile stocks or ETFs, such as SPXL, more attractive to premium sellers and buyers alike.

During periods of elevated volatility, option premium can triple compared to calmer markets. For instance, a spike in IV before earnings or major macro events can cause premiums to surge, even if the underlying price stays stable. Traders often monitor volatility to time their trades and maximize profit potential.

For more on how market volatility shapes pricing dynamics, see Exploring market volatility.

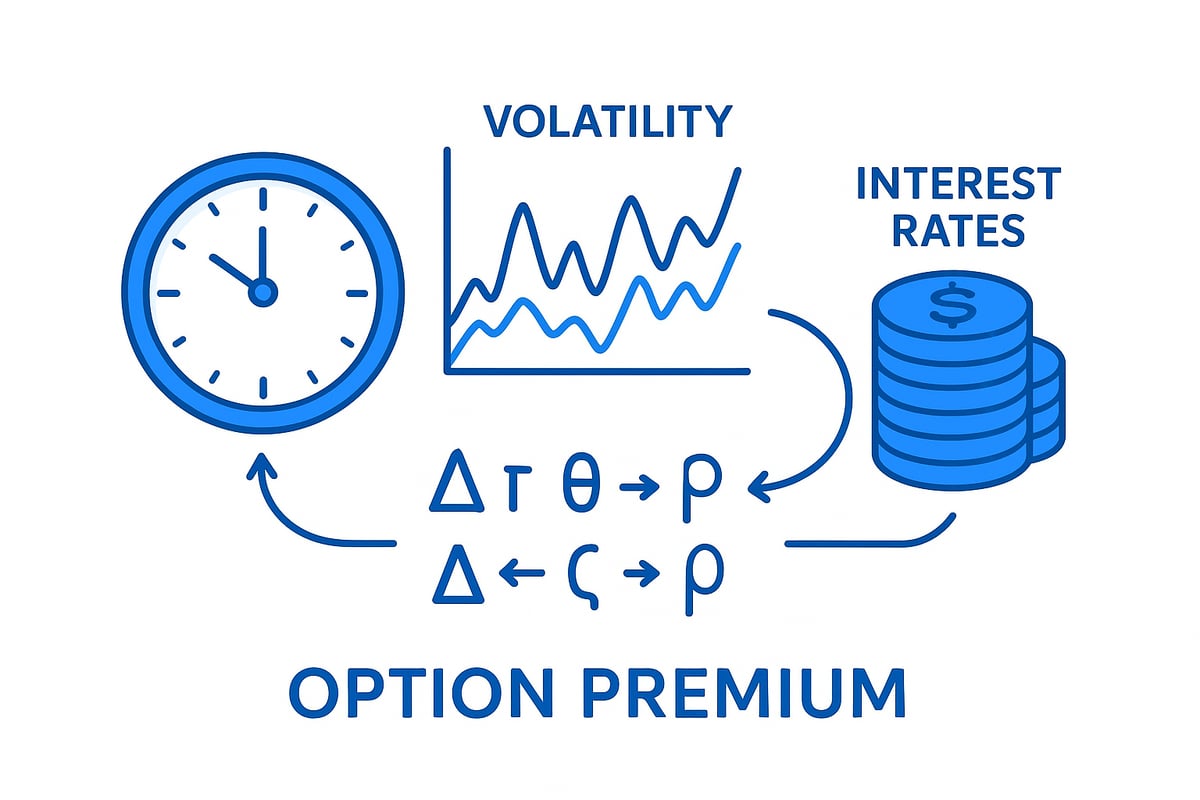

Dividends and Interest Rates (Rho)

Dividends and interest rates also play a direct role in shaping option premium. When a stock is about to pay a dividend, in-the-money call holders may exercise early to capture the payout, which can temporarily raise premiums for those calls.

Interest rates are particularly relevant for long-dated options (LEAPS). As rates climb, so does the opportunity cost of holding an option instead of the underlying asset, increasing the premium for both calls and puts. LEAPS are therefore more sensitive to shifts in rates, making rate forecasts a key consideration for traders in 2026.

Understanding how these macroeconomic factors impact option premium can help you anticipate changes and adjust your strategy accordingly.

The Greeks: Delta, Gamma, Theta, Vega, Rho

The Greeks are a set of metrics that quantify how various factors affect option premium. Each Greek measures a specific sensitivity:

- Delta: Change in option premium per $1 move in the underlying price

- Gamma: Rate of change in delta as the underlying moves

- Theta: Daily time decay impact on premium

- Vega: Sensitivity of premium to changes in IV

- Rho: Premium’s response to shifts in interest rates

For example, if an option has a delta of 0.60, a $1 increase in the underlying should increase the premium by $0.60, all else being equal. Monitoring the Greeks allows traders to manage risk and capitalize on movements that drive option premium in their favor.

Advanced Option Premium Strategies for 2026

Mastering the option premium is essential for traders who want to gain an edge in the 2026 market. Advanced strategies can help you profit in both high and low volatility, control risk, and adapt to changing conditions. Let us break down the top approaches for maximizing your option premium returns.

Buying Premium: Calls and Puts

Buying an option premium gives you the right, but not the obligation, to buy (call) or sell (put) an asset at a fixed price. This approach is favored when you expect a significant price move. For instance, purchasing a call option premium on a stock before an anticipated earnings announcement lets you participate in upside without much capital.

However, the option premium you pay is at risk. If the underlying asset does not move enough to offset the premium and time decay (theta), your option can expire worthless. Consider this scenario:

| Strategy | Premium Paid | Stock Moves Favorably | Profit/Loss |

|---|---|---|---|

| Buy Call | $3.00 | Up $10 | $7 profit (less decay) |

| Buy Put | $2.50 | Down $8 | $5.50 profit (less decay) |

With buying, the option premium acts as your maximum loss, but you need a meaningful move to overcome decay. This is why timing and volatility matter so much.

Selling Premium: Covered Calls, Cash-Secured Puts

Selling option premium is a core strategy for generating income. Covered calls involve holding the underlying stock and selling a call option against it. This lets you collect the option premium up front, but you may have to sell your shares if the stock rises above the strike.

Cash-secured puts work similarly. You sell a put option, promising to buy stock at a lower price if assigned. The premium collected cushions your purchase price and can generate steady returns if the stock stays flat or rises.

Key points to remember when selling option premium:

- You keep the full premium if the option expires worthless.

- Assignment risk means you must be prepared to buy (puts) or sell (calls) at the strike price.

- Sellers often profit most in sideways or slowly moving markets.

Statistic: Most options expire worthless, which benefits sellers who keep the entire option premium.

Multi-Leg Strategies: Spreads, Straddles, Strangles, Condors

Multi-leg strategies use multiple options to balance risk and reward. Spreads, such as vertical or calendar spreads, involve buying one option and selling another. This limits both potential gains and losses, making the option premium more predictable.

Straddles and strangles profit from volatility by buying or selling both call and put option premium contracts. Iron condors and butterflies target range-bound markets by selling multiple out-of-the-money options, aiming to collect as much premium as possible.

Here is a table summarizing common multi-leg strategies:

| Strategy | Market Outlook | Max Risk | Max Reward |

|---|---|---|---|

| Vertical Spread | Directional | Limited | Limited |

| Straddle | Volatile | High | Unlimited |

| Iron Condor | Neutral | Limited | Limited |

For a deep dive into how traders combine these tactics, see Advanced Options Trading Strategies for 2025. Mastering these tools can help you optimize your option premium collection and risk control.

Timing the Market: When to Buy vs. Sell Premium

Timing is everything when trading option premium. High implied volatility (IV) environments, such as before earnings or major news, can inflate premiums. In these periods, selling option premium is often preferred, as IV tends to revert lower and premiums decay quickly.

Conversely, when IV is low, buying option premium may offer better value, especially if you anticipate a volatility spike. Historical cycles, like those seen from 2020 to 2022, show how option premium pricing can swing with market sentiment.

Effective traders monitor macro events, earnings calendars, and volatility indexes to time their option premium trades. By understanding when to buy versus sell, you can capture more value and avoid overpaying for risk.

Risk Management with Option Premiums

Managing risk is crucial in any option premium strategy. Set clear stop-losses and profit targets based on premium movement, not just underlying asset price. Use the Greeks—especially delta and theta—to measure how your position responds to changes in price and time.

As expiration nears, theta accelerates, causing rapid option premium decay. Adjust positions or close trades as this happens to avoid unnecessary losses. Remember, most options expire worthless, so sellers must be vigilant about assignment risk, while buyers should not let time erode their premium investment.

A robust risk management plan ensures your option premium strategies remain profitable and resilient, no matter how the markets evolve.

Real-World Examples and Case Studies

Understanding the option premium in real market scenarios helps traders bridge theory and practice. Let us walk through two practical case studies, highlighting how the option premium behaves under changing market conditions.

Option Premium Fluctuations in Action

Consider this: you buy a call option on ABC stock, which trades at $100 per share. The option premium is $5, with two weeks until expiration. The next day, ABC rises to $103. You check the options chain and see your option premium is now $5.50. It has increased, but not as much as you might expect. Why?

The answer lies in the two main components of the option premium: intrinsic value and extrinsic value. In this case, the intrinsic value increased by $3, but extrinsic value fell due to time decay and a slight drop in implied volatility. For more on how intrinsic value works, see What is intrinsic value.

Here is a simple breakdown:

| Day | Stock Price | Intrinsic Value | Extrinsic Value | Option Premium |

|---|---|---|---|---|

| Purchase | $100 | $0 | $5 | $5 |

| After rise | $103 | $3 | $2.50 | $5.50 |

As time passes and volatility subsides, the option premium can stagnate or even decrease, despite a favorable move in the underlying. A popular Reddit insight summarizes this reality: “Nothing is fixed. The price of the stock is moving, the price of options are moving, time is moving.”

Delta and gamma also play a role. If delta is 0.60, a $1 move in ABC should increase the option premium by $0.60, but changing gamma can accelerate or slow this effect. Tracking these shifts is essential for managing risk and expectations.

Lessons from Recent Market Events

Market volatility in 2022 and 2023 profoundly affected the option premium landscape. For instance, before a major Fed announcement, SPY options exhibited inflated premiums. Implied volatility surged, causing both call and put premiums to triple compared to calmer periods.

During the event, as the market reacted, the option premium on at-the-money contracts changed rapidly. Traders who purchased options before the announcement benefited if the move was significant. However, when the market stabilized afterward, implied volatility dropped sharply, and premiums deflated—even if the underlying price had moved in their favor.

This case highlights the importance of anticipating key events. Earnings releases, central bank decisions, and geopolitical developments can all lead to sudden shifts in the option premium. By monitoring the calendar and implied volatility trends, traders can better position themselves to capitalize on these fluctuations.

Ultimately, these real-world cases underscore that the option premium is never static. It responds to a complex interplay of price, time, and market sentiment. Staying alert to these dynamics is crucial for success in options trading.

Tools, Resources, and Future Trends in Option Premiums

Navigating the modern landscape of option premium trading requires a robust toolkit, reliable resources, and an understanding of emerging trends. As option premium strategies evolve in 2026, traders must leverage technology, data, and community knowledge to stay ahead.

Essential Tools for Tracking and Analyzing Premiums

Mastering option premium analysis starts with the right tools. Options chains are the backbone, providing detailed data on bid-ask spreads, strike prices, and Greeks. Platforms like Thinkorswim, TradingBlock, and Webull offer real-time access to option premium fluctuations, allowing traders to monitor price changes as they happen.

Premium calculators are invaluable for estimating probability of profit, expected value, and key sensitivities. By inputting variables such as volatility, time to expiration, and the underlying asset price, traders can better predict option premium movements. Many advanced platforms visualize these changes, making it easier to spot trends and anomalies.

For those pursuing advanced strategies, options analysis tools can model complex trades like straddles, condors, and even the Iron Butterfly Options Strategy, which is designed to maximize premium collection in neutral markets. These resources equip traders to adapt quickly, ensuring every option premium decision is data-driven.

AI, Data, and the Evolution of Option Premium Strategies

Artificial intelligence is rapidly transforming option premium trading. Machine learning algorithms can process vast datasets, identifying volatility clusters and predicting premium spikes with greater accuracy than ever before. These insights enable traders to refine their strategies, whether buying or selling option premium.

Data visualization tools now display patterns such as implied volatility shifts, time decay acceleration, and unusual volume flows. Algorithmic trading has gained traction, with statistics showing a significant rise in options trades executed by bots designed to optimize premium capture.

AI-powered analytics are not just for institutions. Retail traders increasingly use these innovations to automate trade selection, manage risk, and react to real-time market changes. The evolution of option premium strategies relies on embracing these tools to stay competitive and capitalize on fleeting opportunities.

Education and Community Resources

In-depth knowledge is essential for option premium success. Leading educational hubs like TradingBlock and Investopedia offer comprehensive guides, covering everything from basic terminology to advanced pricing models. Many brokers also provide tutorials tailored to understanding option premium dynamics.

Peer-to-peer learning plays a crucial role. Forums like Reddit’s r/options foster real-world discussion, where traders share experiences and practical tips on how option premium reacts to market shifts. These communities are invaluable for staying current, troubleshooting challenges, and discovering new approaches.

Fundamental analysis of the underlying asset also affects option premium. To deepen your understanding, explore resources like Price to earnings explained, which can help connect company valuation metrics to option premium pricing.

Trends for 2026: What’s Next in Option Premiums?

Looking ahead, several key trends will shape the option premium landscape. Regulatory changes may influence premium pricing and liquidity, especially as market oversight increases. The explosive growth of zero days to expiration (0DTE) options has shifted how premiums are calculated, with more traders seeking short-term opportunities.

Retail participation in option premium trading continues to rise, fueling greater demand for accessible tools and community-driven insights. Short-term contracts are becoming more popular, increasing both risk and reward profiles.

To thrive in 2026, traders must adopt adaptive strategies. As new products and volatility regimes emerge, flexibility and continuous learning will be the cornerstones of long-term success in option premium trading.

As you’ve seen throughout this guide, understanding option premiums means more than just knowing the numbers—it’s about seeing the bigger picture and learning from the past to make smarter decisions in 2026’s dynamic markets. If you want to keep uncovering the stories behind market moves and sharpen your strategies with the power of historical insights, we invite you to be part of something new. Join Our Beta and help shape a platform designed to give you the context, clarity, and tools you need to master the markets with confidence.