Loss Carryforward Guide: Maximize Tax Benefits in 2026

Are you looking for ways to lower your 2026 tax bill? The strategic use of loss carryforward can help you keep more of your hard-earned money. Many taxpayers and investors overlook this powerful tool, missing out on significant savings each year.

Understanding how loss carryforward works can help you offset gains, reduce taxable income, and manage investment volatility. Imagine applying previous years' losses to minimize what you owe this year, giving you more control over your financial future.

This guide will walk you through everything you need to know, from basic definitions and IRS rules to real-world examples and actionable strategies. By the end, you'll know exactly how to leverage loss carryforward for maximum tax benefits in 2026.

Understanding Loss Carryforwards: Definitions and Types

Loss carryforward is a powerful tax concept that allows you to use past losses to reduce future tax bills. Many investors and business owners overlook this essential tool. By understanding loss carryforward, you can smooth out your taxable income and unlock significant long-term tax benefits.

What Is a Loss Carryforward?

A loss carryforward is a tax provision that lets you apply a financial loss from one year to future years. This mechanism is vital for tax planning, as it can reduce your taxable income over time. There are two main types: capital loss carryforwards (typically for individuals and investors) and net operating loss (NOL) carryforwards (mainly for businesses).

The IRS sometimes uses the terms "carryover" and "carryforward" interchangeably, but both refer to moving losses into future tax years. Unlike a "carryback," which applies losses to prior years, a loss carryforward is strictly for upcoming years. For example, if you sell stock at a loss and cannot use the entire loss in the current year, you can carry the remainder forward. This strategy helps smooth out income spikes and dips.

The IRS allows you to use up to $3,000 of capital losses ($1,500 if married filing separately) to offset ordinary income each year. For more definitions on these terms, see the Finance terms glossary.

Types of Loss Carryforwards

There are two primary types of loss carryforward: capital loss carryforwards and net operating loss (NOL) carryforwards. Capital loss carryforwards are most common for individuals and investors who incur losses from selling stocks, bonds, or other investments. These can be used to offset future capital gains and a limited amount of ordinary income.

NOL carryforwards, on the other hand, are typically used by businesses. When a company's business deductions exceed its income, it generates an NOL, which can be carried forward to offset future profits.

Treatment differs: personal capital loss carryforwards are separate from business NOLs, and there are distinctions between short-term and long-term capital losses. Notably, at the federal level, capital loss carryforwards never expire, while NOLs have specific usage rules. Understanding your loss type is crucial for effective tax planning and compliance with IRS regulations.

Key IRS Rules and Limitations

The IRS sets strict rules for using a loss carryforward. For capital losses, you may deduct up to $3,000 ($1,500 if married filing separately) against ordinary income each year. Before applying losses to ordinary income, you must first offset any capital gains.

The wash-sale rule prohibits you from claiming a loss if you buy a substantially identical security within 30 days of selling at a loss. For NOLs, recent tax law changes (such as the Tax Cuts and Jobs Act) restrict carryforward use to 80% of taxable income each year. For example, if you have a $7,000 loss and a $2,000 gain, you must offset the gain first, then apply up to $3,000 to ordinary income, with the remainder carried forward.

By following IRS guidelines, you avoid disallowed deductions or penalties. Always keep accurate records to support your loss carryforward claims.

Short-Term vs. Long-Term Capital Losses

Short-term capital losses come from assets held for one year or less, while long-term losses apply to assets held for more than a year. The IRS requires you to match the type of loss to the same type of gain first, so short-term losses offset short-term gains and long-term losses offset long-term gains.

For instance, if you have both types of gains and losses, you must apply each loss to the corresponding gain before mixing types. This matters because short-term gains are taxed at ordinary income rates, which are generally higher than long-term capital gains rates. Matching loss types correctly can maximize your tax efficiency and ensure optimal use of your loss carryforward.

By understanding the differences and following IRS rules, investors can make smarter decisions and avoid costly mistakes.

How Loss Carryforwards Work: Step-by-Step Process

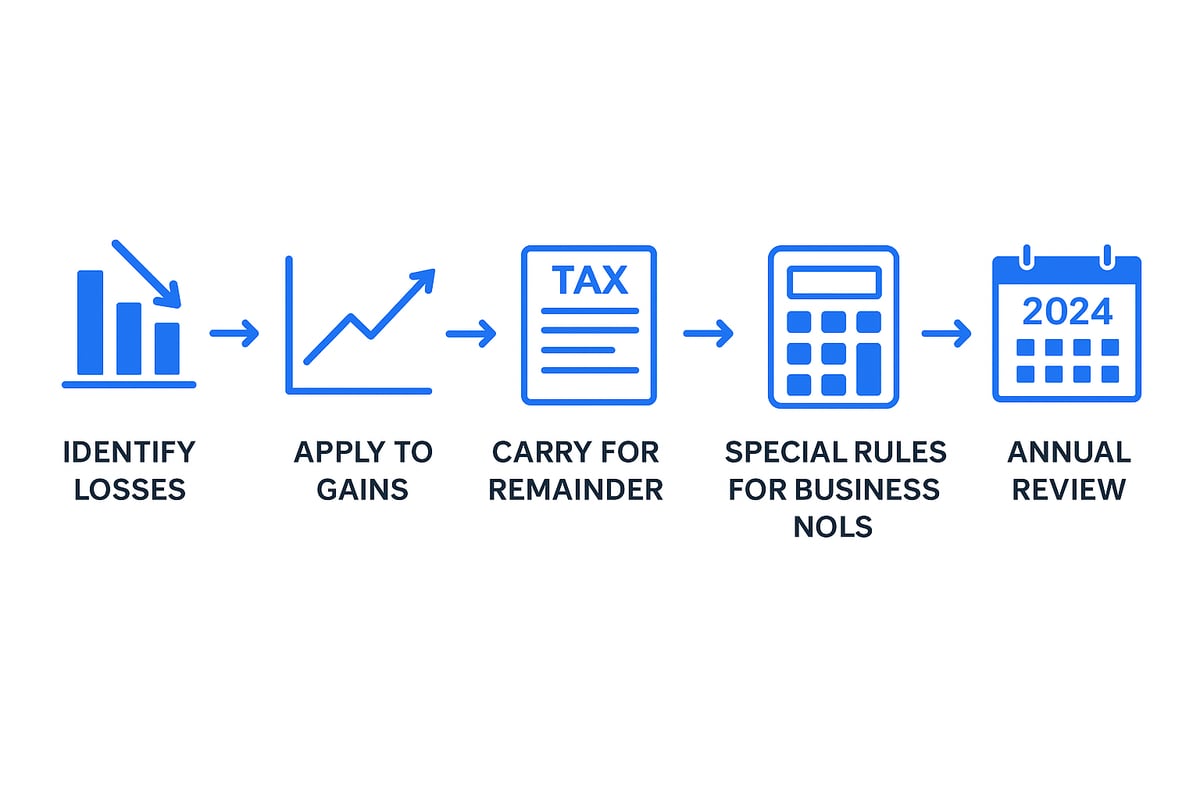

Understanding the mechanics of a loss carryforward is essential for making the most of tax-saving opportunities. The process involves several key steps, each designed to help you accurately capture, report, and utilize your losses over multiple years.

Step 1: Identify and Calculate Eligible Losses

Start by determining which of your losses qualify for a loss carryforward. Only realized losses, such as those from selling an asset at a lower price than you paid, count toward this process. Unrealized losses, where you still own the asset, do not apply.

Use IRS Schedule D to report and calculate your net capital loss for the tax year. For example, if you have a $10,000 loss and a $5,000 gain, your net loss is $5,000. Accurate record-keeping is crucial, as every figure on your tax return must be supported by documentation.

Step 2: Apply Losses to Current Year Gains and Income

Next, apply your losses to any capital gains you realized during the year. The loss carryforward process requires you to offset gains before deducting losses from ordinary income.

If your total losses exceed gains, you can deduct up to $3,000 ($1,500 if married filing separately) from your ordinary income. For instance, with a $7,000 loss and a $2,000 gain, offset the gain first, then apply $3,000 to income, leaving $2,000 for future years. The IRS provides a worksheet to help track your remaining loss carryforward.

Step 3: Carry Forward Remaining Losses

Any unused loss carryforward must be recorded for use in future tax years. Each year, report these amounts on Schedule D and Form 1040, following the same process.

There is currently no expiration for capital loss carryforwards at the federal level, so you can continue using them indefinitely until fully utilized. For example, if you have $2,000 left after this year’s deductions, you’ll repeat the same calculations next year. Proper documentation ensures IRS compliance and prevents costly mistakes.

Step 4: Special Considerations for Net Operating Losses (NOLs)

Businesses have a different set of rules for NOLs. An NOL occurs when your business deductions exceed gross income. Since the Tax Cuts and Jobs Act, NOL carryforwards are limited to 80 percent of taxable income per year, and most carrybacks are disallowed.

For example, if your business has a $100,000 NOL, you can use up to $80,000 to offset future taxable income annually. The reporting process requires different forms and worksheets, such as Form 1045 and Schedule A. For comprehensive guidance, consult IRS Publication 536 on NOLs, which details the latest rules and calculations for NOL loss carryforward.

Step 5: Monitor and Maximize Use Year Over Year

Review your loss carryforward balances annually. Adjust your investment or business strategies to make the most of available losses. For example, plan to realize gains in years when you have large carryforwards remaining.

State rules may differ, so check for potential expiration or deduction limits locally. Staying proactive ensures you get the full benefit from your loss carryforward and avoid missing valuable opportunities.

Tax Benefits of Loss Carryforwards in 2026

Effectively using a loss carryforward can transform your tax strategy in 2026. By understanding how these tax tools reduce taxable income, offset gains, and support planning for both individuals and businesses, you can retain more of your profits. Let’s break down the key benefits in detail.

Reducing Taxable Income and Liability

The primary advantage of a loss carryforward is its ability to lower your taxable income year after year. For example, if you have a $3,000 capital loss carryforward, and you’re in the 22% tax bracket, you could save $660 on your tax bill each year the loss is applied.

This annual deduction adds up, especially if your investments fluctuate. Over several years, the compounding benefit can be substantial. Essentially, a loss carryforward helps smooth out the impact of volatile investment returns, making your tax situation more predictable and manageable.

- Offsets ordinary income when gains are not available

- Reduces overall tax liability

- Provides flexibility in tax planning

Offsetting Capital Gains and Maximizing Investment Returns

A loss carryforward lets you offset future capital gains, lowering the effective tax rate on your profitable investments. If you harvest losses in a down year, you can use them to neutralize gains during a bull market, potentially saving thousands over a decade.

This strategy is especially vital for high-net-worth investors and active traders who regularly realize gains. By integrating loss carryforward planning with your investment approach, you can maximize after-tax returns.

- Offsets gains before applying losses to income

- Delays taxes on future gains

- Creates opportunities for strategic rebalancing

Strategic Planning for Businesses with NOLs

For businesses, a loss carryforward in the form of net operating losses (NOLs) is a critical resource. When a business has more deductions than income, these losses can be used to offset future profits, easing the tax burden during growth years.

Consider a tech startup that generates NOLs in its early stages. As it becomes profitable, the loss carryforward allows it to reinvest more earnings, supporting innovation and expansion. In fact, studies show businesses with NOLs are more likely to invest in research and development, fueling long-term growth.

- Supports cash flow management

- Encourages reinvestment

- Provides a safety net during economic downturns

Implications for Retirement and Estate Planning

A well-managed loss carryforward can be valuable during retirement. By using carryforwards to offset gains from IRA withdrawals or taxable investment sales, retirees can reduce their taxable income and potentially minimize the impact on Social Security and Medicare surcharges.

However, it’s important to remember that a loss carryforward does not transfer to heirs or new owners. Strategic planning is needed to use up these losses before major life events, such as retirement account withdrawals or estate transfers.

- Reduces taxes during retirement drawdown years

- Influences RMD and Social Security taxation

- Must be used by the original taxpayer

Recent and Upcoming Tax Law Changes Impacting 2026

Tax law changes can significantly affect how you use a loss carryforward, especially for businesses. The Tax Cuts and Jobs Act (TCJA) of 2017 and the CARES Act of 2020 both introduced new rules for NOL deductions and carryforwards. For instance, NOLs can now offset only up to 80% of taxable income per year for most businesses.

Looking ahead to 2026, potential legislative updates could alter deduction limits or carryforward periods. Staying updated with IRS guidance and consulting a tax professional is essential. For a detailed overview of recent business tax changes and how they impact loss carryforward rules, see the Tax Cuts and Jobs Act Business Tax Changes.

- Monitor legislative updates

- Use IRS resources for compliance

- Seek professional advice for optimal planning

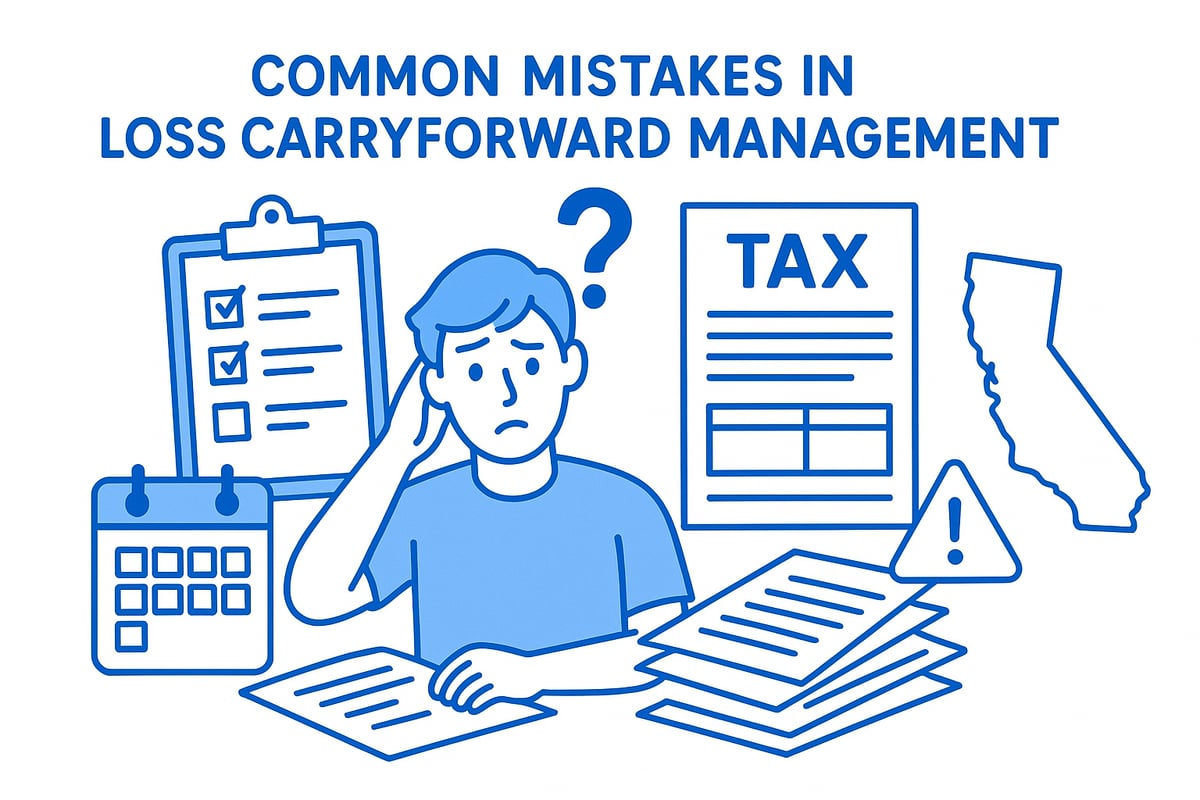

Common Mistakes and How to Avoid Them

Taxpayers and investors often miss out on the full benefits of a loss carryforward due to preventable errors. Recognizing these common pitfalls can help you preserve more of your tax savings and avoid IRS complications. Let's review the most frequent mistakes and how to sidestep them.

Failing to Track and Document Losses Properly

Accurate tracking is essential for leveraging your loss carryforward. Many taxpayers lose valuable deductions simply because they do not maintain adequate records.

- Failing to keep receipts or brokerage statements

- Not updating IRS worksheets each year

- Overlooking losses from prior returns

For example, missing out on a $5,000 loss carryforward due to disorganized files can lead to higher taxes and stress during an audit. Use tax software or spreadsheets to document every transaction, and review your records annually. Thorough documentation ensures you can claim every allowable deduction without hassle.

Misapplying the Wash-Sale Rule

The wash-sale rule is a frequent stumbling block for those using a loss carryforward. If you sell a security at a loss and then buy a substantially identical one within 30 days, the IRS disallows the loss.

Key points to remember:

- The 30-day window applies before and after the sale

- Applies to stocks, ETFs, and options

- Disallowed losses cannot be added to your loss carryforward

For instance, selling and repurchasing the same stock within this period nullifies your tax benefit. Always check transaction dates and avoid automatic reinvestment plans that might trigger a wash sale. Understanding this rule is crucial to protecting your loss carryforward.

Overlooking State Tax Differences

Many filers assume federal and state loss carryforward rules are identical, but this is rarely the case. States often have unique carryforward periods or deduction limits.

- Some states cap the number of years you can carry losses

- Deduction limits may differ from federal law

- State definitions of net operating loss can vary

For example, California allows only a five-year carryforward for NOLs, while other states have their own rules. It's wise to consult updates like the State NOL Provisions Update to stay current. Understanding state-specific requirements ensures you maximize your total loss carryforward potential.

Neglecting to Use Losses Before Death or Business Sale

A loss carryforward cannot be transferred to heirs or new owners if you pass away or sell your business. Any unused balance is lost forever.

- Capital loss carryforwards expire upon death

- NOLs may not transfer in business sales

- Strategic gain realization can help use up losses

For example, if you have a large carryforward and anticipate a major life event, consider realizing gains to offset those losses in advance. Proactive planning ensures your hard-earned tax benefits are not left unused. Always coordinate with your tax advisor before significant personal or business changes.

Advanced Strategies to Maximize Tax Benefits

Unlocking the full advantage of a loss carryforward requires proactive planning and precision. Advanced strategies can help you align losses with gains, coordinate financial moves, and ensure every tax-saving opportunity is realized. Both individuals and businesses benefit from a thoughtful approach. Let us explore the most effective tactics for maximizing your tax benefits.

Tax-Loss Harvesting: Timing and Execution

Tax-loss harvesting is the process of selling investments that have declined in value to realize a loss. This realized loss can then be used as a loss carryforward to offset taxable gains. The timing is critical. Many investors review their portfolios near year-end, identifying underperforming assets to sell and lock in losses.

Steps for effective tax-loss harvesting:

- Review holdings for unrealized losses.

- Sell investments with losses before year-end.

- Avoid the wash-sale rule when repurchasing similar securities.

By harvesting losses in a down market, you create a loss carryforward that can be applied to offset future gains, lowering your overall tax liability. Strategic timing ensures losses are available when most needed.

Coordinating Loss Carryforwards with Investment Strategy

Integrating your loss carryforward into your broader investment plan is key to maximizing tax efficiency. If you have a sizable carryforward, consider timing the sale of appreciated assets to offset gains. This approach can help you rebalance your portfolio without triggering large tax bills.

For example, if you anticipate gains in certain years, plan asset sales accordingly. Use your loss carryforward to “reset” your cost basis, reducing future taxable gains. Regularly review your investment allocations and coordinate them with your available carryforwards.

This synchronization allows you to capture gains when your loss carryforward balance is highest, making your overall investment growth more tax efficient.

Business Planning with NOLs: Mergers, Acquisitions, and IRC Section 382

Businesses with significant net operating losses (NOLs) must consider special rules during mergers and acquisitions. The IRS imposes annual limits on the use of NOLs after a change in ownership, as outlined in Section 382 NOL Limitations.

Key points for business planning:

- Calculate allowable NOL usage after an ownership change.

- Integrate NOL analysis into due diligence processes.

- Structure deals to maximize future NOL utilization.

Understanding how loss carryforward rules apply in these scenarios is crucial. Failing to plan around Section 382 can result in lost tax savings and reduced deal value. Always consult with tax professionals during M&A transactions to ensure compliance and optimal outcomes.

Utilizing Loss Carryforwards for Charitable Giving and Gifting

Charitable giving and gifting strategies can work hand in hand with loss carryforward planning. When you donate appreciated assets, you can offset the resulting capital gains with your carryforwards, effectively reducing your taxable income.

Consider these tactics:

- Donate long-term appreciated securities to maximize deductions.

- Use loss carryforward to neutralize gains from charitable transactions.

- Plan gifts to family members, using up losses before transferring assets.

By coordinating charitable donations with your loss carryforward, you generate double tax benefits. This approach supports your philanthropic goals while optimizing your tax position for the current and future years.

Integrating Loss Carryforwards with Retirement Withdrawals

Loss carryforward strategies are especially valuable during retirement. As you begin regular withdrawals from tax-deferred accounts, realized capital gains can push you into higher tax brackets. By matching gains and withdrawals with available loss carryforwards, you can minimize the tax impact.

Effective planning may include:

- Scheduling asset sales in low-income years.

- Using loss carryforward to offset gains from required minimum distributions.

- Reducing exposure to Social Security and Medicare surcharges.

A well-coordinated approach ensures your retirement income is as tax-efficient as possible, preserving more of your savings for the long term.

Working with Tax Professionals and Using IRS Tools

Maximizing the value of your loss carryforward often requires expert guidance. Tax professionals can help you track balances, interpret IRS rules, and identify optimal strategies. Regular meetings ensure your approach remains aligned with changing laws and life circumstances.

Helpful resources include:

- IRS Schedule D for capital loss reporting.

- Form 1045 for NOL applications.

- Tax software with carryforward tracking features.

By leveraging professional advice and IRS tools, you gain confidence that your loss carryforward strategy is accurate and fully optimized. Annual reviews and smart planning can yield substantial long-term tax savings.

Real-World Examples and Case Studies

Real-world scenarios make understanding loss carryforward much clearer. By exploring how individuals and businesses use loss carryforward, you can see the practical benefits and common challenges. Each example below shows how careful planning can turn potential setbacks into long-term advantages.

Individual Investor: Multi-Year Capital Loss Carryforward

Consider an investor who realized a $15,000 capital loss in 2024. Since the IRS allows only $3,000 per year to offset ordinary income, this loss carryforward is used over five years, from 2025 through 2029.

Each year, $3,000 is deducted, potentially reducing the investor’s tax bill by hundreds annually. Careful documentation ensures every dollar of the loss carryforward is claimed. This patient approach pays off, as the investor smooths out tax liability across several years and maximizes overall savings.

Small Business: Net Operating Loss Carryforward Over Growth Cycle

A small business startup incurs a $200,000 net operating loss (NOL) during its initial years. The business leverages the NOL as a loss carryforward, offsetting up to 80% of taxable income in profitable years, in line with post-TCJA rules. This strategy frees up cash for reinvestment and supports business growth.

Understanding capital expenditures is crucial, since these costs directly impact NOL calculations and the available loss carryforward. For more on this, see the Capital expenditure explained guide. Regularly reviewing NOL balances ensures the business optimizes its tax position.

Active Trader: Tax-Loss Harvesting and Wash-Sale Pitfalls

Active traders often face a mix of gains and losses. Suppose a trader frequently buys and sells small-cap stocks. By harvesting losses, they generate a loss carryforward to offset gains in future years.

However, if the trader violates the wash-sale rule by repurchasing a substantially identical security within 30 days, the loss is disallowed. This mistake highlights the need for vigilance and accurate record-keeping. For those trading volatile assets, the Small-cap stock overview offers insights into common strategies and risks.

Retirement Planning: Using Carryforwards for Tax-Efficient Withdrawals

A retiree with a $25,000 loss carryforward carefully coordinates IRA withdrawals. By timing gains and withdrawals, the retiree uses the loss carryforward to offset taxable income before required minimum distributions increase their tax bracket.

This integrated approach can maximize after-tax retirement income. Strategic use of loss carryforward is especially valuable in retirement years, as it helps manage both tax liability and cash flow.

Business Acquisition: NOL Limitations Post-Merger

Imagine a company acquiring another firm with $1 million in NOLs. Section 382 of the tax code limits how much of the loss carryforward can be used each year post-acquisition, based on the value of the acquired business.

Proper due diligence and post-merger tax planning are vital. Understanding these limitations ensures the acquiring company can utilize as much of the loss carryforward as possible, protecting its future tax savings.

Frequently Asked Questions About Loss Carryforwards

Curious about how loss carryforward rules impact your finances? Here are concise answers to the most common questions from taxpayers and investors.

What is the difference between a capital loss carryforward and an NOL?

A capital loss carryforward allows individuals to apply unused capital losses to future tax years, reducing taxable gains or income. Net operating loss (NOL) carryforwards, on the other hand, are typically available to businesses whose deductions exceed income. The main distinction is that capital loss carryforward applies to investment losses, while NOLs cover wider business losses. Knowing which type you have is crucial for maximizing benefits.

How many years can I carry forward a capital loss or NOL?

At the federal level, capital loss carryforward has no expiration—you can apply unused losses indefinitely until fully used. For NOLs generated after 2017, the IRS also allows indefinite carryforward, but only up to 80% of taxable income per year. However, some states impose their own time limits, so always check your local rules.

Are there limits on how much loss I can use each year?

Yes. For capital loss carryforward, the IRS lets you offset capital gains first, then up to $3,000 ($1,500 if married filing separately) of ordinary income per year. For NOLs, post-2017 rules limit you to 80% of taxable income annually. Accurate record-keeping ensures you do not exceed these caps.

What happens to loss carryforwards if I die or sell my business?

Loss carryforward balances do not transfer to heirs or new owners. If you pass away or sell your business, any unused losses are generally lost. It is wise to plan ahead and use up your loss carryforward before major life events to avoid losing valuable tax benefits.

Can I carry forward losses on rental property or real estate?

Yes, but the rules differ based on whether the loss is passive or active. Passive activity losses, such as those from rental properties, may be subject to special limitations. Only unused passive losses can be carried forward to offset future passive income. Tracking these losses separately is essential for compliance.

How do state tax laws affect my loss carryforward?

State tax rules can differ significantly from federal guidelines. Some states restrict the number of years you can carry forward losses or set lower deduction limits. For example, California limits NOL carryforward to five years. Always review your state’s requirements each year.

What forms and worksheets do I need to file with the IRS?

For capital loss carryforward, use Schedule D with your Form 1040. For NOLs, you may need Form 1045 and the appropriate worksheets. Using IRS-provided forms helps ensure accurate calculation and reporting of your loss carryforward each year.

How do I track my loss carryforwards year to year?

Maintain organized records of all realized losses, gains, and amounts carried forward. Tax software and IRS worksheets can simplify tracking. Each year, update your carryforward balances to make sure you are using losses efficiently and within IRS limits.

Can I use loss carryforwards to offset income other than capital gains?

Capital loss carryforward can offset up to $3,000 of ordinary income annually after offsetting capital gains. NOLs, however, can offset a broad range of business income. For more on how business losses arise, see Net interest margin basics, which explains how profitability and losses are calculated.

What are the most common mistakes to avoid with loss carryforwards?

Common pitfalls include failing to document losses, misapplying the wash-sale rule, and overlooking state-specific deadlines. Missing these details can result in lost deductions or IRS penalties. Careful record-keeping and annual reviews help you avoid these errors and make the most of every loss carryforward opportunity.

As you’ve seen, understanding loss carryforwards can make a real difference in how much you keep from your investments and business activities in 2026. By learning from past market moves and staying on top of IRS rules, you’re positioning yourself for smarter, more informed decisions. At Historic Financial News, we believe that seeing the bigger financial picture—past and present—gives you an edge. If you’re passionate about exploring the stories behind market shifts and want early access to our new platform, I invite you to Join Our Beta. Let’s empower your financial journey together.