GNMA Guide 2025: Understanding Government Mortgage Securities

Unlock the secrets behind one of the safest investment options in the U.S. housing market: gnma securities. These government-backed assets play a vital role in promoting affordable homeownership while offering stability to investors.

This GNMA Guide 2025 will demystify the Government National Mortgage Association, showing how gnma connects global investors to American mortgages and supports key borrower groups. You will discover the agency’s unique structure, how mortgage-backed securities work, and why gnma bonds are considered a gold standard for safety.

Ready to make informed decisions? Read on for a step-by-step guide to understanding and leveraging gnma this year.

What is GNMA (Ginnie Mae)?

The Government National Mortgage Association, better known as gnma or Ginnie Mae, is a cornerstone of the United States housing finance system. As a government agency operating within the Department of Housing and Urban Development (HUD), gnma plays a pivotal role in expanding access to affordable homeownership.

Established to support the flow of capital into the housing market, gnma guarantees timely payment of principal and interest on certain mortgage-backed securities. This guarantee does not mean gnma lends money directly. Instead, gnma ensures that investors who purchase securities backed by government-insured loans receive their payments on time, regardless of economic conditions.

GNMA’s Mission and Role in U.S. Housing

At its core, gnma exists to make homeownership more attainable for millions of Americans. The agency achieves this by guaranteeing mortgage-backed securities (MBS) that are supported by loans from federal programs such as the Federal Housing Administration (FHA), the Department of Veterans Affairs (VA), and the U.S. Department of Agriculture (USDA).

Unlike banks or other mortgage lenders, gnma does not originate or issue loans. Instead, it acts as a guarantor, promising investors that payments on these securities will be made promptly and in full. This government-backed guarantee makes gnma MBS extremely attractive to a wide range of investors, both in the U.S. and internationally.

By increasing investor confidence, gnma connects global capital markets with American mortgages. This connection provides crucial liquidity for lenders, allowing them to offer more loans with favorable terms. For example, nonbank lenders can reach low- and moderate-income borrowers who might otherwise be overlooked by traditional institutions.

The types of loans gnma guarantees include:

- FHA-insured loans for first-time and moderate-income buyers

- VA loans for veterans and military families

- USDA loans for rural and suburban borrowers

- Special programs such as Section 184 for tribal members

For those new to mortgage-backed securities, a helpful resource is this Asset-backed security explained guide, which outlines the fundamental structure underlying gnma’s guarantees.

In 2025, gnma’s mission remains sharply focused on serving underserved markets and first-time homebuyers, helping bridge the homeownership gap across the country.

GNMA’s Impact on Borrowers and Lenders

The impact of gnma extends beyond its guarantee. By backing MBS, gnma enables lenders to offer lower interest rates and more flexible qualification standards than many conventional loan programs. This is especially important for groups such as veterans, rural residents, tribal communities, and those purchasing a home for the first time.

During times of economic stress, gnma’s role becomes even more critical. Its guarantee ensures that capital continues to flow to lenders, supporting the stability of the housing market. After the 2008 financial crisis, for example, gnma-backed securities were instrumental in restoring confidence and liquidity.

The benefits for borrowers are substantial:

- Access to lower rates and smaller down payments

- Flexible credit requirements

- Targeted support for specific populations

Lenders also benefit from the ability to sell loans into the secondary market, freeing up capital to fund additional mortgages. This process helps keep housing affordable and accessible, even in challenging times.

As of 2025, gnma guarantees over $2 trillion in mortgage-backed securities, reflecting its scale and importance in the housing finance landscape. Its continued focus on underserved borrowers ensures that a broader range of Americans have the opportunity to achieve homeownership.

The History and Evolution of GNMA

The story of gnma is inseparable from the evolution of the American housing market. As the landscape of homeownership shifted over decades, gnma emerged as a cornerstone in providing affordable mortgage options and stability for both borrowers and investors.

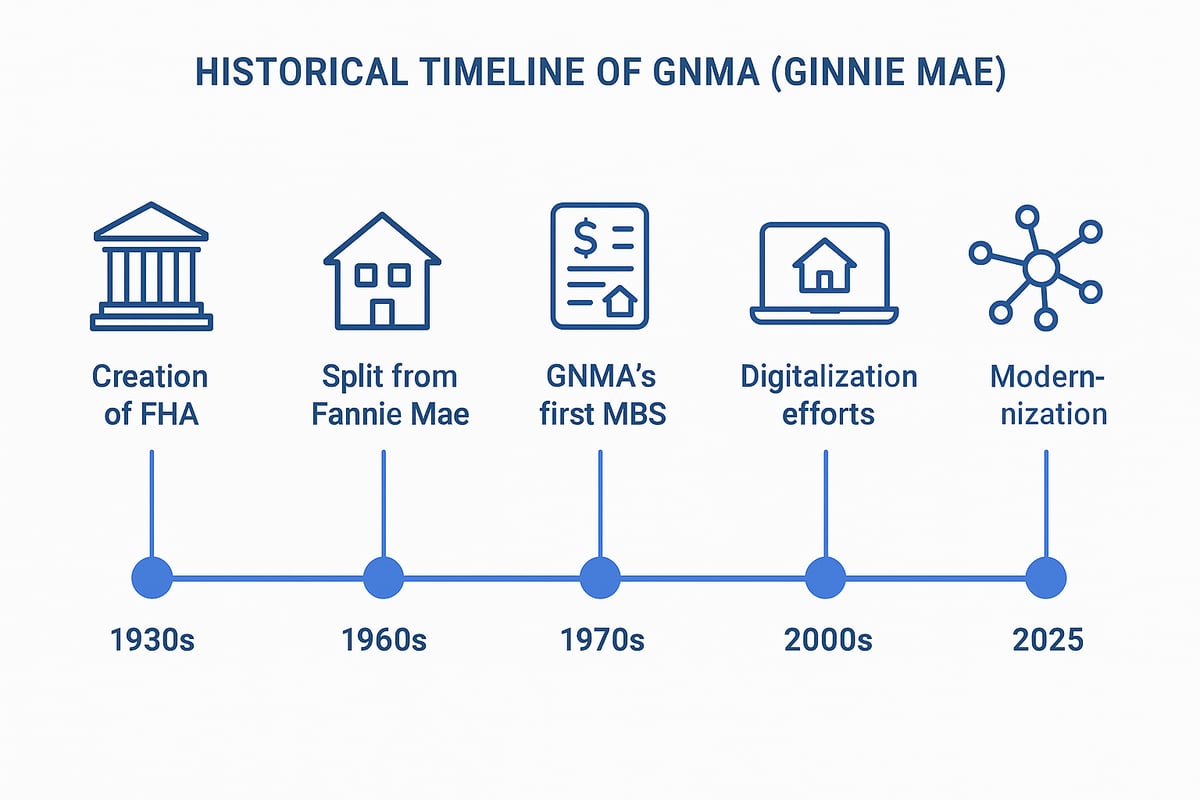

Origins and Key Milestones

The origins of gnma trace back to the economic turmoil of the Great Depression. In 1934, the Federal Housing Administration (FHA) was created to insure mortgages and restore confidence in the housing sector. Four years later, Fannie Mae was established to buy FHA-insured loans, helping lenders manage risk and freeing up capital.

A pivotal moment came in 1968 with the Housing and Urban Development Act. This legislation split Fannie Mae into two distinct entities: Fannie Mae, focusing on conventional loans, and gnma, tasked with supporting government-insured mortgages. Shortly after, the first gnma-guaranteed mortgage-backed securities (MBS) were introduced, offering investors a new, reliable asset class.

The gnma guarantee transformed MBS into a global investment vehicle. By ensuring the timely payment of principal and interest, gnma attracted institutional and international investors, fueling growth in the U.S. mortgage market.

GNMA’s Role in Expanding Homeownership

Over time, gnma has played a critical role in expanding homeownership, particularly for low- and moderate-income families. By backing loans insured by FHA, VA, and USDA, gnma enabled millions to access affordable mortgages, including first-time buyers and residents in rural communities.

The reach of gnma-backed lending is evident in the growth of government-insured loan programs. Notably, MBS issuance doubled between 2010 and 2025, underscoring the agency’s impact. For recent data and in-depth analysis of these trends, the Urban Institute's Housing Finance Policy Center April 2025 Chartbook provides a comprehensive overview of gnma's expanding footprint and its importance in the broader housing finance ecosystem.

This growth has made gnma a trusted partner for lenders and a lifeline for underserved borrowers seeking a path to homeownership.

Adapting to Market Changes

gnma’s resilience is evident in how it has navigated major market shifts. During the 2008 financial crisis, gnma responded by strengthening oversight and enhancing risk management protocols, ensuring the continued stability of its MBS.

In recent years, gnma has embraced digital transformation, streamlining processes and increasing transparency for issuers and investors. Digital tools now enable faster securitization and improved data accuracy. Looking ahead to 2025, gnma is prioritizing Environmental, Social, and Governance (ESG) standards, reflecting a commitment to sustainable and responsible lending.

These ongoing adaptations position gnma at the forefront of innovation in the mortgage market, ensuring its relevance and reliability for years to come.

How GNMA Mortgage-Backed Securities Work

Understanding how gnma mortgage-backed securities (MBS) function is fundamental for borrowers, lenders, and investors. These securities form the backbone of affordable housing finance in the United States, and their structure is both innovative and robust.

Structure and Process of GNMA MBS

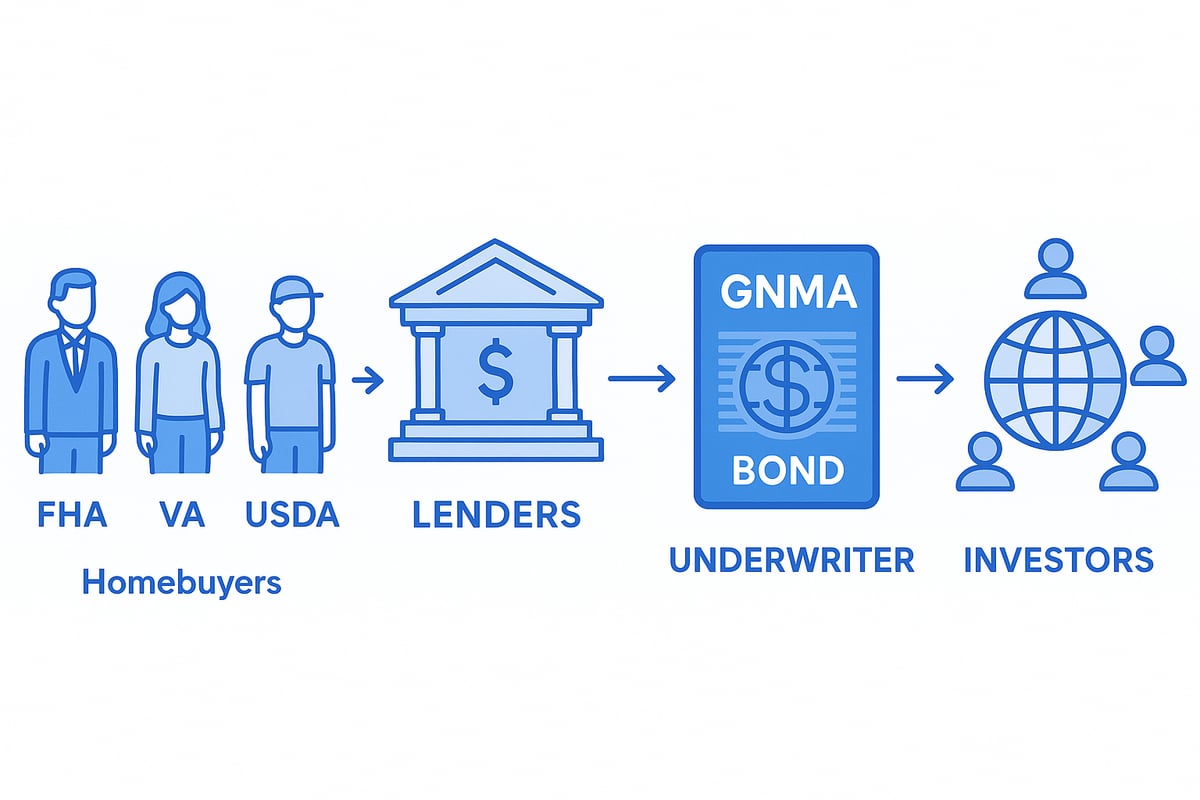

The gnma MBS process begins when approved lenders originate government-backed mortgages, such as FHA, VA, or USDA loans. Instead of holding these loans on their books, lenders pool them together to create a diversified collection of mortgages.

Next, the pooled loans are evaluated and structured for securitization. An essential step in this process involves an underwriter, whose role is to assess the quality and compliance of the loan pool. For more details, see the role of underwriters. Once the loans are approved, they are packaged into a gnma MBS.

Gnma’s critical function is to guarantee the timely payment of principal and interest on these securities. This guarantee, backed by the full faith and credit of the U.S. government, transforms the pooled mortgages into highly secure investments. Institutional and retail investors worldwide can then purchase these securities, injecting capital back into the mortgage market.

This cycle ensures a steady flow of funds, supporting ongoing mortgage lending and homeownership opportunities.

Benefits for Borrowers and Lenders

Gnma-backed MBS offer tangible advantages for both borrowers and lenders. For lenders, the ability to sell loans as securities creates immediate liquidity. This allows them to fund new loans without waiting for existing ones to be repaid.

Borrowers benefit from the increased availability of credit, which translates into lower interest rates and more flexible qualification standards. Gnma’s guarantee enables lenders to confidently serve a broader range of applicants, including first-time homebuyers and those with moderate incomes.

In practice, gnma MBS help stabilize the housing finance system, keeping mortgage rates competitive and supporting economic growth.

Investor Perspective: Why Buy GNMA MBS?

Investors are drawn to gnma MBS for several reasons. The most prominent is the full faith and credit guarantee by the U.S. government, which makes these securities among the safest fixed-income investments available.

Gnma MBS typically offer yields that are higher than Treasuries but lower than most corporate bonds, striking a balance between safety and return. This yield advantage appeals to conservative investors, pension funds, and retirement plans seeking dependable income streams.

Another benefit is liquidity. Gnma MBS are actively traded in global markets, allowing investors to buy and sell with relative ease. Many bond funds and institutional portfolios include gnma securities as a core holding, recognizing their role in risk management and income generation.

Risks and Prepayment Considerations

While gnma MBS are considered safe, investors must be aware of certain risks. The primary risk is prepayment, where homeowners refinance or pay off their mortgages early. This can affect the predictability of cash flows and the overall return on investment.

Interest rate risk is another factor. When market rates rise, the value of existing gnma MBS may decline, impacting their market price. Gnma addresses these risks by setting strict requirements for issuers and maintaining oversight of the securitization process.

To summarize, gnma MBS are robust, but investors should evaluate prepayment trends and interest rate outlooks before committing capital. Understanding these factors helps investors balance security with performance in their portfolios.

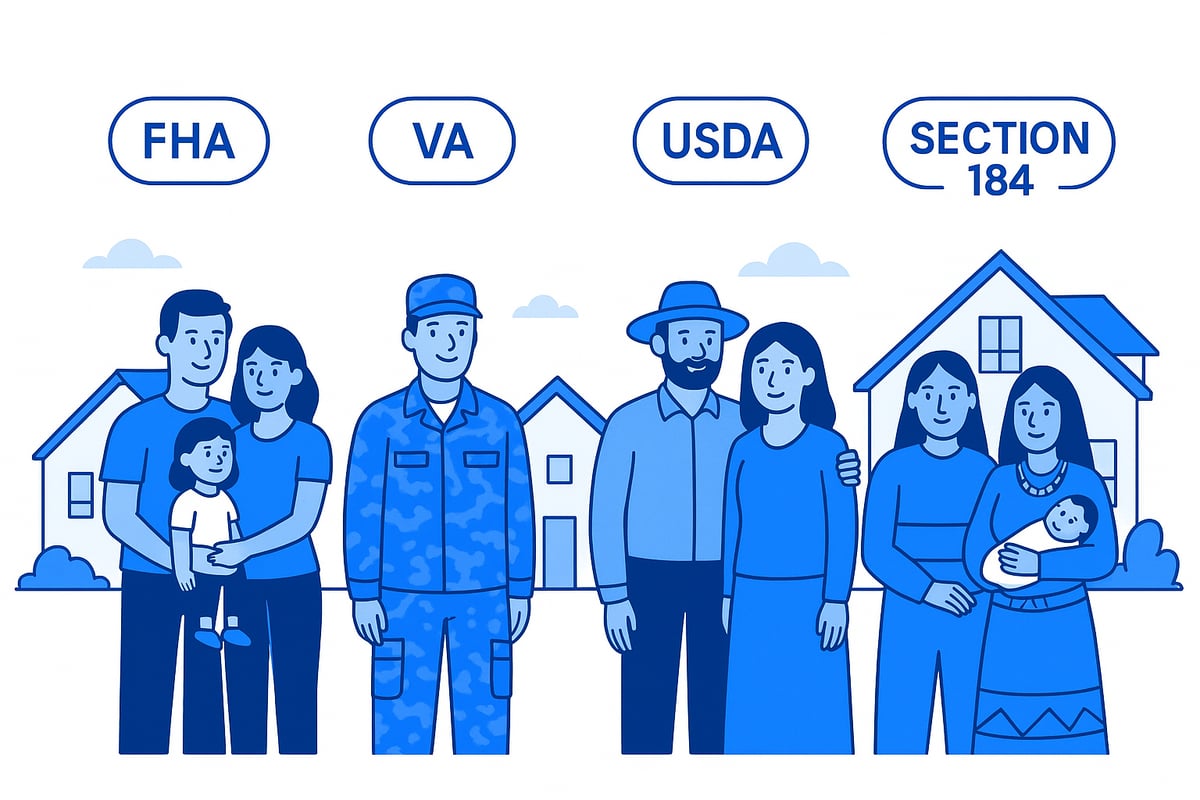

Types of Loans Backed by GNMA

Homeownership in the United States is possible for many thanks to the diverse range of loans backed by gnma. By guaranteeing mortgage-backed securities for government-insured loans, gnma enables lenders to offer accessible financing to various borrower groups. Let’s explore the primary types of loans supported by gnma and how they impact today’s housing market.

FHA Loans

FHA loans are designed for low and moderate-income borrowers who may not qualify for conventional mortgages. With gnma’s guarantee, lenders can offer reduced down payments, sometimes as low as 3.5 percent, and flexible credit requirements. This makes homeownership more attainable for those with limited savings or credit challenges.

Key features of FHA loans include:

- Low down payment options

- Lenient credit score standards

- Competitive interest rates

Many first-time buyers rely on gnma-backed FHA loans to purchase their first homes, benefiting from the program’s accessibility and support.

VA Loans

VA loans are reserved for veterans, active-duty service members, and eligible surviving spouses. These loans, guaranteed by gnma, provide significant benefits such as no required down payment and no private mortgage insurance.

Key aspects of VA loans:

- Zero down payment required

- No monthly mortgage insurance

- Favorable terms for military families

The gnma guarantee ensures that lenders can confidently extend credit to those who have served, making homeownership more achievable for the military community.

USDA Loans

USDA loans, also backed by gnma, support rural and some suburban homebuyers. These loans are ideal for households that meet income limits and wish to purchase in eligible areas.

Advantages of USDA loans include:

- No down payment needed

- Reduced mortgage insurance costs

- Focus on rural development

Thanks to gnma, lenders are able to offer USDA loans to families who might otherwise face barriers to securing a mortgage in less populated regions.

Other Government-Backed Loans

In addition to the major programs above, gnma also guarantees other specialized government loans. The Section 184 Indian Home Loan Guarantee Program, for example, is tailored for Native American and Alaska Native families, tribes, and tribal housing entities. HUD also supports loans for disaster recovery and affordable housing initiatives.

These programs expand gnma’s impact, ensuring that unique borrower groups receive the support they need for homeownership.

GNMA’s Role in Expanding Access

Gnma plays a vital role in keeping these government-backed loan programs viable and attractive for lenders. By providing a government guarantee, gnma encourages lenders to participate in FHA, VA, USDA, and other programs, ensuring a steady flow of capital for underserved and first-time homebuyers.

In fact, over 70 percent of FHA, VA, and USDA loans are securitized through gnma. For the most recent data and analysis on gnma’s activities and market trends, see the Ginnie Mae's April 2025 Global Markets Analysis Report.

Are GNMA Securities Safe? Investment Considerations for 2025

When evaluating the safety of mortgage-backed securities, gnma stands out as a benchmark for reliability in fixed-income investing. Investors often turn to gnma securities for stable income and peace of mind, especially during periods of economic uncertainty.

Safety and Credit Quality

The core strength of gnma securities lies in their explicit guarantee by the U.S. government. This guarantee covers both principal and interest payments, regardless of borrower defaults. As a result, gnma mortgage-backed securities (MBS) consistently receive AAA ratings from major credit agencies.

Unlike Fannie Mae or Freddie Mac, which have only implicit government backing, gnma MBS are considered virtually risk-free in terms of credit quality. For institutional investors and risk-averse portfolios, this assurance makes gnma a foundational holding. During past financial crises, gnma's full faith and credit guarantee helped stabilize the housing market and maintain investor confidence.

Yield, Liquidity, and Market Demand

Gnma securities provide a unique balance of yield and safety. They typically offer higher yields than U.S. Treasuries, yet slightly lower yields than comparable corporate bonds. This makes gnma MBS attractive for those seeking a safe yet rewarding income stream.

Liquidity is another key advantage. Gnma MBS are actively traded in global markets, ensuring investors can buy or sell positions efficiently. High demand from pension funds, mutual funds, and foreign investors helps keep spreads tight and prices stable. As of 2025, gnma MBS remain a staple in retirement and income-focused portfolios.

Risks and Return Factors

While gnma securities are safe from credit risk, investors should be aware of other factors. Prepayment risk is significant, as borrowers may refinance or pay off loans early, affecting cash flow timing. Interest rate risk is also present, since rising rates can reduce the market value of gnma MBS.

Extension risk can emerge if interest rates rise quickly, slowing prepayments and locking investors into lower yields. To navigate these challenges, gnma imposes strict requirements on issuers, enhancing transparency and risk management. Understanding the maturity date in bonds is crucial for aligning gnma investments with personal financial goals.

Who Should Invest in GNMA?

Gnma securities are best suited for conservative investors who prioritize safety and reliable income. They appeal to retirees, pension funds, and those managing risk-averse portfolios. The predictable payment structure of gnma MBS makes them a core holding for investors seeking to preserve capital while generating steady cash flow.

Financial advisors often recommend gnma as a diversification tool, especially in uncertain markets. The government guarantee offers peace of mind that few other fixed-income products can match. For those focused on income with minimal credit risk, gnma is a logical choice.

2025 Trends and Outlook

Looking ahead, gnma is expected to see sustained demand amid global economic uncertainty. Digitalization is transforming the gnma market, with improved transparency and efficiency for issuers and investors alike. Environmental, Social, and Governance (ESG) criteria are increasingly integrated into gnma MBS pools, reflecting broader investor priorities.

According to Payden & Rygel's GNMA Market Commentary September 2025, digital adoption and ESG initiatives are driving innovation and expanding the appeal of gnma securities. As regulatory standards evolve and technology advances, gnma's role in supporting affordable homeownership and stable investments is likely to grow even stronger.

GNMA vs. Fannie Mae and Freddie Mac: Key Differences

Understanding the distinctions between GNMA, Fannie Mae, and Freddie Mac is essential for anyone involved in mortgage securities. Each plays a unique role in the U.S. housing market, influencing everything from loan types to investment safety. This section breaks down the core differences, helping you navigate the world of mortgage-backed securities with confidence.

Agency Structure and Government Backing

GNMA is a government agency operating under the Department of Housing and Urban Development. This means GNMA securities are fully backed by the U.S. government, ensuring timely payments to investors. In contrast, Fannie Mae and Freddie Mac are government-sponsored enterprises, or GSEs. Their mortgage-backed securities carry only an implicit guarantee, not the full faith and credit of the government. This structural difference is central to understanding the varying risk profiles among these entities.

| Feature | GNMA | Fannie Mae/Freddie Mac |

|---|---|---|

| Agency Type | Government | Government-Sponsored |

| Guarantee | Explicit | Implicit |

Types of Loans and Borrowers Served

The types of loans securitized by GNMA differ from those handled by Fannie Mae and Freddie Mac. GNMA exclusively backs loans insured or guaranteed by government agencies, such as FHA, VA, and USDA loans. These programs target borrowers with lower incomes, limited down payments, or specific needs. Fannie Mae and Freddie Mac, on the other hand, support conventional loans, which generally require higher credit scores and larger down payments. This distinction shapes the borrower base for each entity.

MBS Structure and Investor Considerations

GNMA mortgage-backed securities are known for their low credit risk, thanks to the explicit government guarantee. Investors seeking security often choose GNMA MBS for this reason. Fannie Mae and Freddie Mac MBS, while still considered high-quality, carry a slightly higher credit risk due to their implicit backing. Yields for GNMA MBS are typically a bit lower, reflecting their safety. The broader loan pools of Fannie Mae and Freddie Mac may appeal to investors seeking more variety in their holdings.

Market Impact and Policy Differences

GNMA plays a critical role in promoting affordable housing, especially for underserved and first-time homebuyers. Its focus is on supporting government loan programs that expand access to homeownership. Fannie Mae and Freddie Mac influence the conventional mortgage market, setting standards for creditworthiness and loan limits. Policy differences between these institutions impact lending rates, underwriting guidelines, and the overall stability of the housing finance system.

Example and Data

As of 2025, GNMA guarantees over $2 trillion in mortgage-backed securities, serving a vital segment of the market. In comparison, Fannie Mae and Freddie Mac collectively have even larger volumes, but their focus is on different borrower groups. To understand the broader context, you can refer to Fannie Mae's April 2025 Economic and Housing Outlook, which provides key insights into market trends affecting all three agencies. This data underscores how each entity responds to changing economic conditions, ensuring a resilient mortgage landscape.

Key Trends and Future Outlook for GNMA in 2025

The landscape for gnma is rapidly evolving as the housing finance industry embraces new technologies, regulatory updates, and shifting market demands. Looking ahead to 2025, several key trends are set to shape the future of gnma securities and their role in the U.S. mortgage market.

Digital Transformation and Technology Adoption

Digital transformation is at the heart of gnma’s 2025 strategy. The agency is rolling out digital mortgage-backed securities issuance and exploring blockchain pilots to enhance transparency.

These initiatives allow real-time reporting and data sharing, making processes more efficient for issuers and investors. By leveraging technology, gnma aims to reduce costs, minimize errors, and increase the speed of transactions.

Issuers are adapting to new digital standards, which is expected to boost participation from non-bank lenders and fintech firms. This focus on innovation positions gnma as a leader in modernizing mortgage securitization.

Policy and Regulatory Changes

In 2025, gnma is navigating several policy and regulatory updates that affect loan eligibility and credit score requirements. HUD and Congressional actions are shaping how gnma programs serve first-time and underserved homebuyers.

Recent changes aim to streamline approval processes and expand access to affordable financing. These adjustments help gnma remain responsive to evolving borrower needs and market conditions.

As regulatory oversight grows, issuers face new compliance standards, but the net result is a safer, more resilient mortgage-backed securities market.

Market Dynamics and Investor Demand

Global capital flows are increasingly directed toward safe U.S. assets, with gnma securities in high demand during periods of economic uncertainty. Investors are drawn to the full government guarantee and the relative stability gnma offers compared to other fixed-income options.

A growing number of income-focused portfolios and retirement plans now include gnma MBS as core holdings. For those interested in how investors manage risk and principal repayment, understanding what is a sinking fund? can provide valuable context.

The liquidity of gnma securities ensures that both institutional and retail investors can access and trade these assets efficiently.

Affordable Housing Initiatives

A central mission for gnma in 2025 is expanding affordable housing opportunities. The agency supports new projects targeting first-time buyers and minority communities, using innovative programs to address persistent housing shortages.

Gnma’s guarantee plays a crucial role in making low-down-payment and flexible-credit loans viable for lenders. The result is a broader reach for FHA, VA, and USDA loan programs, particularly in rural and underserved regions.

As affordability remains a national concern, gnma’s efforts are vital for millions seeking homeownership.

ESG and Sustainable Investing

Environmental, Social, and Governance (ESG) factors are becoming integral to gnma’s strategy. The agency is integrating ESG criteria into its MBS pools, including launching green MBS initiatives that support energy-efficient homes.

Investors are increasingly seeking gnma securities that align with their sustainability goals. This shift encourages lenders to finance properties with lower environmental impact and higher community benefits.

ESG integration positions gnma as a forward-thinking leader in responsible investing within the mortgage sector.

Challenges and Opportunities

Despite its strengths, gnma faces challenges in 2025. Managing prepayment risk and interest rate volatility remains a priority, especially as rates fluctuate and borrowers refinance.

Housing affordability and supply constraints also create headwinds. However, gnma’s commitment to innovation and responsive policy offers new opportunities for growth and impact.

Data shows gnma’s MBS issuance is projected to grow, with digital adoption and global participation on the rise. By addressing these challenges, gnma is well positioned to support both investors and homebuyers in the years ahead.

As you’ve seen, understanding GNMA securities is key to navigating both the past and future of U S housing finance. If you’re fascinated by how government-backed mortgages shape markets and want to explore more stories behind major financial events, I invite you to experience a new way of learning with us. Our platform brings history to life with interactive charts, AI-powered summaries, and in depth news coverage—perfect for investors and lifelong learners alike. Ready to dive deeper and help shape this unique resource? Join our beta and help us bring history to life