Ginnie Mae Guide 2026: Everything You Need to Know

Are you trying to make sense of government-backed mortgages and how they could affect your financial future? Understanding ginnie mae is essential for anyone interested in the U.S. housing market, whether you are a first-time homebuyer or a seasoned investor.

This guide will help you unravel the complexities of ginnie mae, its unique government guarantee, and why it matters for your homeownership journey or investment strategy in 2026.

Discover the history, core functions, key programs, and the evolving role of ginnie mae in making mortgages more affordable and the market more stable. By the end, you will be ready to use this knowledge to make smarter, more informed financial choices.

What is Ginnie Mae? The Basics Explained

Understanding ginnie mae is essential for anyone interested in the U.S. housing market. As the Government National Mortgage Association, ginnie mae operates as a government agency within the Department of Housing and Urban Development (HUD). Unlike Fannie Mae or Freddie Mac, ginnie mae does not lend money or buy loans directly. Instead, its main function is to guarantee the timely payment of principal and interest on mortgage-backed securities (MBS) that are supported by federally insured or guaranteed loans. If you want a comprehensive look at its background and functions, the Ginnie Mae Overview provides helpful context. This guarantee is the cornerstone that sets ginnie mae apart, making it a critical player in the mortgage ecosystem.

What is the Government National Mortgage Association?

Ginnie mae acts as a vital bridge between the U.S. government and the mortgage market. Its guarantee gives lenders the confidence to provide more loans to homebuyers, knowing they will receive payments even if borrowers default. This process channels global investment into American housing by turning pools of government-backed mortgages into MBS. By guaranteeing these securities, ginnie mae ensures that lenders have steady access to capital, which ultimately supports affordable homeownership. For context, ginnie mae consistently holds a significant share of the government-backed MBS market, making it a trusted name among investors and lenders.

How Ginnie Mae Supports the Mortgage Market

The mission of ginnie mae is focused on expanding access to affordable housing, especially for those who might otherwise struggle to qualify for a mortgage. Its beneficiaries include low- and moderate-income families, veterans, first-time homebuyers, and residents of rural or tribal areas. Through partnerships with agencies like the FHA, VA, USDA, and Public and Indian Housing (PIH) programs, ginnie mae amplifies its impact. These collaborations help reduce barriers for underserved communities, increasing the number of people who can achieve homeownership. As a result, ginnie mae plays a pivotal role in making the dream of owning a home more attainable for millions.

Ginnie Mae’s Mission and Beneficiaries

There are several misconceptions about ginnie mae that often cause confusion. First, ginnie mae does not originate, service, or buy loans itself. Instead, it guarantees securities backed by government-insured loans. Another common myth is that ginnie mae, Fannie Mae, and Freddie Mac serve the same purpose, but they have distinct roles and types of loans they support. Lastly, some believe the government guarantee means there is no risk involved, but while the guarantee protects investors, it does not eliminate all risk from the process. By understanding these differences, borrowers and investors can make more informed decisions about ginnie mae.

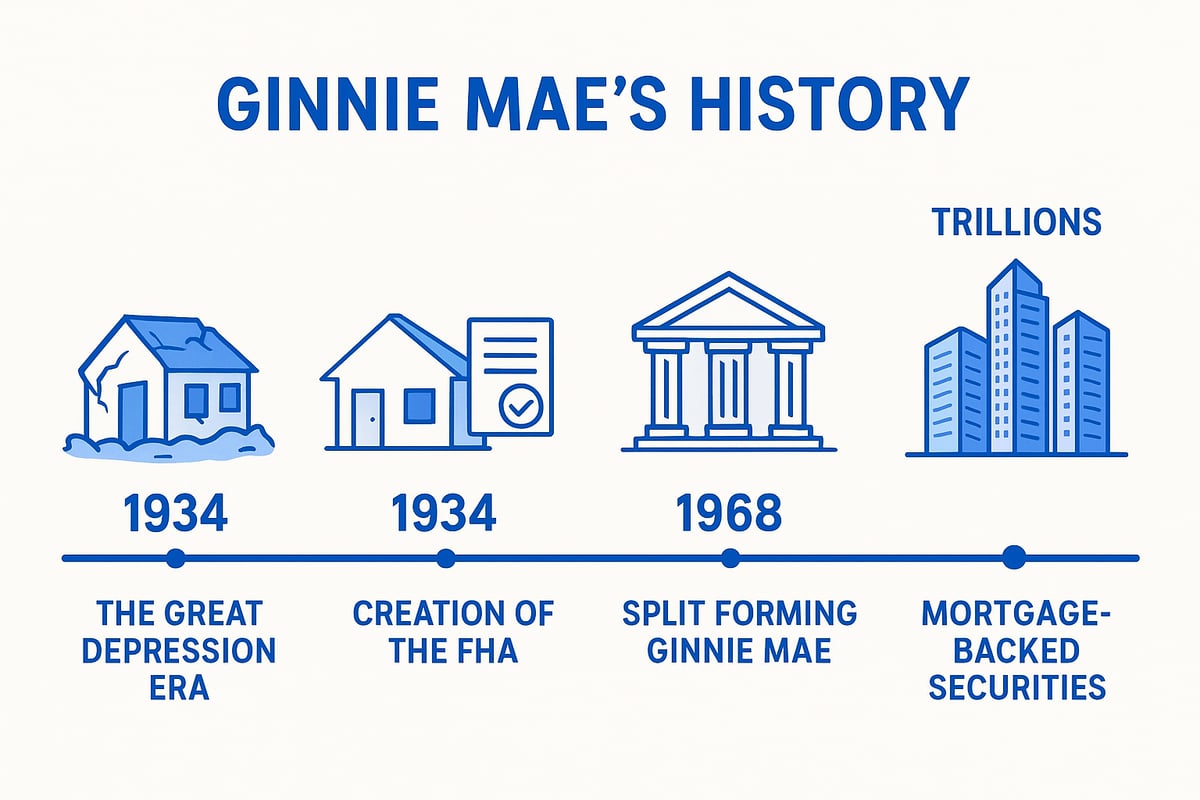

A Brief History of Ginnie Mae

Understanding the history of ginnie mae is essential to see how it became a cornerstone in the U.S. housing market. The agency’s evolution reflects responses to major economic challenges and changing national priorities, shaping how millions access affordable homeownership.

Origins: The Great Depression and the Birth of FHA

The roots of ginnie mae trace back to the 1930s, a time when the U.S. faced widespread foreclosures and a severe housing crisis. With many families losing their homes, restoring public confidence in mortgage lending became crucial.

In response, the federal government established the Federal Housing Administration (FHA) in 1934. The FHA introduced mortgage insurance, allowing banks to lend with less risk. This innovation laid the groundwork for future agencies like ginnie mae, aiming to make homeownership more accessible for Americans.

Evolution: From Fannie Mae to Ginnie Mae

As the housing market evolved, the government created new solutions to expand mortgage availability. In 1938, Fannie Mae was founded to buy FHA-insured loans, injecting liquidity into the mortgage system.

A major shift happened in 1968 with the Housing and Urban Development Act. Fannie Mae was divided into two distinct entities. The new agency, ginnie mae, was tasked with supporting only government-insured or guaranteed loans. This move clarified its mission and allowed ginnie mae to focus on serving borrowers with FHA, VA, and similar loans.

Milestones in Ginnie Mae’s Development

Ginnie mae achieved a landmark in 1970 by issuing the first government-guaranteed mortgage-backed security (MBS). This financial innovation attracted global investors and gave lenders new tools to fund home loans.

Over time, ginnie mae expanded its programs to include loans backed by the Department of Veterans Affairs (VA) and the U.S. Department of Agriculture (USDA). Legislative and regulatory changes throughout the decades strengthened its oversight and broadened its impact on affordable housing.

Ginnie Mae Today: Market Impact and Growth

Today, ginnie mae manages a vast portfolio, with outstanding mortgage-backed securities totaling trillions of dollars. Its guarantee helps keep mortgage rates stable and supports affordable housing for millions.

Recent years have seen ginnie mae play a vital role during financial crises, ensuring the continued flow of credit. For a deeper look at its recent performance and market presence, explore the Ginnie Mae 2024 Annual Report, which details its operations and milestones in the modern era.

How Ginnie Mae Works: Process, Programs, and Participants

Understanding how ginnie mae operates is key to appreciating its unique influence on the mortgage market. This section breaks down the step-by-step process, the main programs, who participates, and how ginnie mae ensures safety and stability for both lenders and investors.

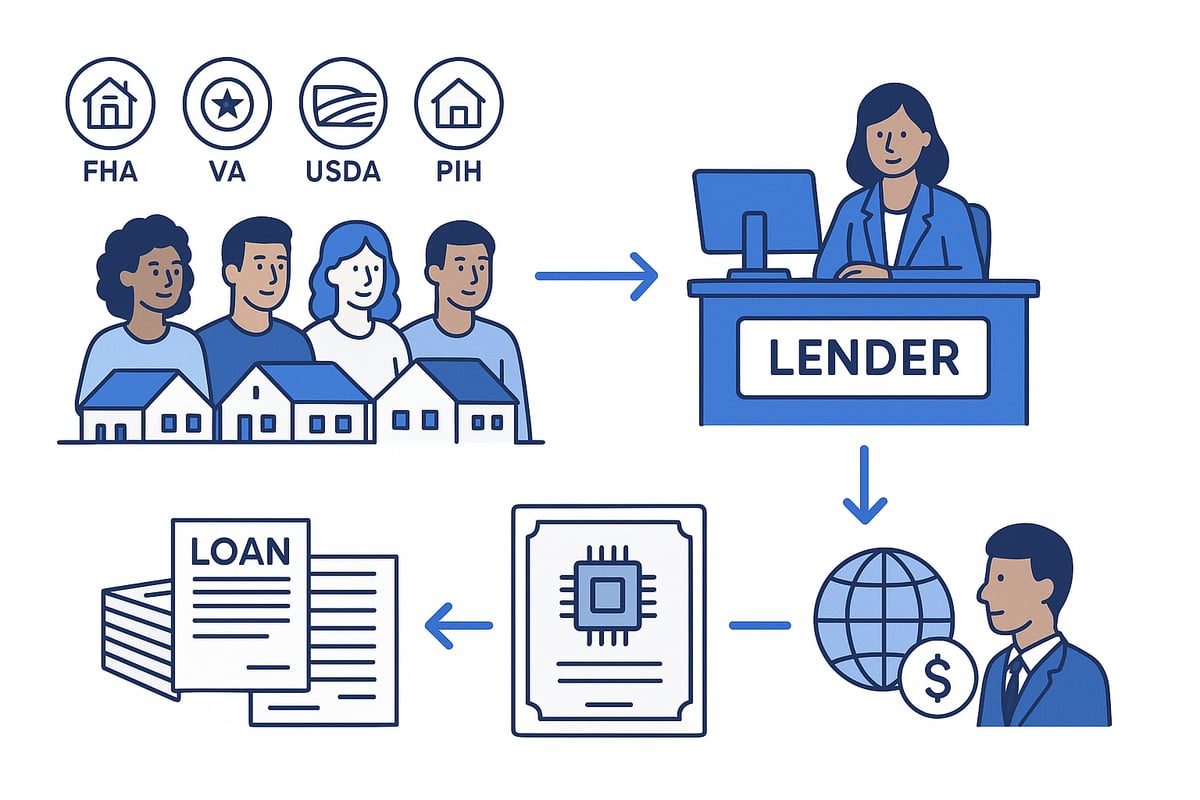

The Ginnie Mae Mortgage-Backed Securities (MBS) Process

At the core of ginnie mae’s work is the creation of mortgage-backed securities, often called MBS. Here’s how the process unfolds: lenders originate government-backed loans, such as FHA, VA, USDA, or PIH mortgages, to eligible homebuyers. These loans are then grouped into pools and transformed into MBS, which are sold to investors around the world.

What makes this system unique is the ginnie mae guarantee. By promising timely payment of principal and interest, ginnie mae gives investors confidence to purchase these securities. This guarantee enables lenders to access global capital, making more funds available for new home loans. For a deeper dive into the basics, see What is an asset-backed security.

Key Ginnie Mae Programs and Loan Types

Ginnie mae offers several major programs tailored to meet a range of housing needs. The Single-Family MBS Program covers most FHA, VA, USDA, and PIH loans for individual homeowners. For larger properties, the Multifamily MBS Program supports apartment buildings and affordable rental housing.

Another important offering is the Home Equity Conversion Mortgage (HECM) MBS, designed for reverse mortgages that help seniors access home equity. Each program is structured to expand mortgage access, with ginnie mae ensuring that even underserved or high-need borrowers have financing options.

| Program | Loan Types Covered | Typical Borrowers |

|---|---|---|

| Single-Family MBS | FHA, VA, USDA, PIH | Homebuyers, first-time buyers |

| Multifamily MBS | FHA, USDA | Developers, renters |

| HECM MBS | FHA Reverse Mortgage | Seniors |

Who Can Issue Ginnie Mae Securities?

Not just any lender can issue ginnie mae securities. Only approved mortgage lenders and financial institutions that meet strict financial and compliance standards are eligible. These issuers must show they have the resources and systems to manage large loan pools responsibly.

Ginnie mae closely monitors its issuers, conducting regular audits and reviews to ensure quality and reduce risk. This oversight protects both investors and borrowers, making ginnie mae programs a reliable choice for a wide range of market participants.

How the Guarantee Works: Safety and Investor Confidence

The ginnie mae guarantee is backed by the full faith and credit of the U.S. government. If a borrower defaults on their loan, ginnie mae steps in to make sure investors still receive their scheduled principal and interest payments.

This guarantee is a major reason why ginnie mae securities are considered among the safest in the mortgage market. High investor demand for these securities helps keep mortgage rates affordable and stable, benefiting both lenders and homebuyers.

Ginnie Mae’s Role in Affordable Housing

Expanding affordable housing is one of ginnie mae’s primary missions. By partnering with federal agencies and local housing authorities, ginnie mae channels funds to first-time homebuyers, veterans, rural residents, and tribal communities.

A significant share of ginnie mae-backed loans go to underserved groups who might struggle to qualify for conventional loans. This focus on inclusivity helps bridge the housing gap and fosters stronger, more stable communities.

Recent Updates and Program Innovations for 2026

Ginnie mae is constantly evolving to meet new challenges. In 2026, the agency is expected to roll out technology upgrades, including greater use of digital securitization and enhanced risk management tools. These improvements aim to make the securitization process faster, safer, and more transparent.

Policy updates may also expand eligibility or strengthen oversight for issuers. As borrower demographics shift, ginnie mae programs are adapting to ensure continued support for affordable housing and market stability.

Investing in Ginnie Mae: Bonds, Risks, and Rewards

Investing in Ginnie Mae offers a unique opportunity for both individual and institutional investors seeking stability and consistent returns. Understanding the features, risks, and rewards of these securities is crucial for making informed decisions in today’s financial landscape.

What are Ginnie Mae Bonds and Securities?

Ginnie Mae mortgage-backed securities (MBS) and bonds are financial instruments backed by pools of government-insured or guaranteed loans. Unlike Treasuries, which are direct obligations of the U.S. government, Ginnie Mae bonds represent claims on cash flows from FHA, VA, USDA, or PIH mortgages.

These securities differ from those issued by Fannie Mae or Freddie Mac, as only Ginnie Mae provides the explicit backing of the federal government. Typical investors include individuals, pension funds, mutual funds, and insurance companies. Ginnie Mae helps connect global capital with U.S. housing, making these investments a cornerstone of the mortgage market.

| Security Type | Backing | Typical Investors |

|---|---|---|

| Ginnie Mae MBS | U.S. Government | Individuals, Funds |

| Fannie/Freddie MBS | GSEs (implicit) | Funds, Banks |

| Treasuries | U.S. Government | All Investor Types |

Safety and Creditworthiness: Is Ginnie Mae a Safe Investment?

Ginnie Mae is widely regarded as one of the safest fixed-income investments due to its “full faith and credit” guarantee from the U.S. government. This assurance means investors receive their principal and interest payments even if borrowers default.

Historically, Ginnie Mae securities have maintained high credit ratings and low default rates. For those interested in examining the organization’s fiscal strength, the Ginnie Mae Financial Statements provide transparency into its balance sheets and risk management practices. This level of safety attracts conservative investors who prioritize capital preservation and steady income.

Risks Associated with Ginnie Mae Investments

While Ginnie Mae investments are considered very safe, they are not without risks. The most common risk is prepayment risk, which occurs when homeowners refinance or pay off their mortgages early. This can impact the timing and amount of returns investors receive.

Another key risk is interest rate risk. When rates rise, the value of existing Ginnie Mae securities may decline, and when rates fall, prepayments may increase. Market liquidity can also fluctuate, sometimes making it harder to sell these securities quickly at a favorable price. Understanding these risks is essential for building a resilient investment portfolio.

Returns and Yield Potential

Yields on Ginnie Mae securities typically fall between those of U.S. Treasuries and conventional mortgage-backed securities. Several factors influence these yields, including prevailing interest rates, prepayment speeds, and market demand.

For example, during periods of low interest rates, Ginnie Mae MBS may see increased prepayments, which can reduce yields. Conversely, in rising rate environments, yields may become more attractive relative to other fixed-income options. Reviewing historical data can help investors set realistic expectations for potential returns and understand how these securities perform in different market cycles.

How to Invest in Ginnie Mae Securities

Investors can access Ginnie Mae securities directly by purchasing MBS or indirectly through mutual funds and exchange-traded funds (ETFs) focused on government-backed mortgages. Retail investors may need to meet minimum investment requirements, while funds offer a lower barrier to entry and professional management.

Considerations when investing include portfolio diversification, risk tolerance, and investment horizon. Ginnie Mae products can complement a balanced portfolio, offering stability and income with the backing of the U.S. government. Consult with a financial advisor to determine the most suitable approach for your goals.

Ginnie Mae vs. Fannie Mae and Freddie Mac: Key Differences

Understanding the distinctions among ginnie mae, Fannie Mae, and Freddie Mac is essential for anyone interested in the U.S. mortgage market. While all three entities play pivotal roles in housing finance, their structures, missions, and levels of government backing differ in ways that shape both borrower experiences and investor confidence.

Structure and Government Involvement

Ginnie mae is a wholly owned government agency operating under the Department of Housing and Urban Development (HUD). This direct federal oversight means its obligations are explicitly backed by the U.S. government. In contrast, Fannie Mae and Freddie Mac are government-sponsored enterprises (GSEs). They are privately owned but chartered and regulated by the federal government, which creates a different risk profile and oversight structure.

| Entity | Structure | Oversight | Government Guarantee |

|---|---|---|---|

| Ginnie Mae | Government Agency | HUD | Explicit |

| Fannie Mae | GSE | FHFA | Implicit |

| Freddie Mac | GSE | FHFA | Implicit |

This unique positioning gives ginnie mae a distinct role in ensuring stability and public trust in mortgage-backed securities.

Types of Loans Backed

The types of loans each entity supports are a key differentiator. Ginnie mae exclusively guarantees securities backed by government-insured or government-guaranteed loans. These include mortgages from programs like FHA, VA, USDA, and Public and Indian Housing (PIH). Fannie Mae and Freddie Mac, on the other hand, focus on conventional loans that lack direct government insurance.

Eligibility for ginnie mae-backed loans often involves meeting specific criteria set by federal programs, making them more accessible to first-time buyers, veterans, and rural households. For a detailed look at how Fannie Mae and Freddie Mac compare to each other, see this Fannie Mae vs. Freddie Mac Comparison.

Guarantee and Investor Protection

Ginnie mae provides an explicit government guarantee for investors in its mortgage-backed securities. This means the U.S. government commits to making timely payments of principal and interest, even if homeowners default. Fannie Mae and Freddie Mac offer only an implicit guarantee, which relies on market perception and past government interventions rather than a formal commitment.

This distinction gives ginnie mae securities a unique appeal for risk-averse investors, as the explicit guarantee reduces uncertainty. The result is higher investor confidence and often more favorable borrowing terms for eligible homeowners.

Impact on Borrowers and Lenders

The influence of ginnie mae, Fannie Mae, and Freddie Mac extends to both borrowers and lenders. By guaranteeing government-backed loans, ginnie mae supports access to credit for underserved markets, including low-to-moderate income families and veterans. Fannie Mae and Freddie Mac, meanwhile, facilitate liquidity for conventional loans, helping to keep rates competitive for a broader segment of the market.

For lenders, ginnie mae’s government guarantee can lower funding costs and reduce risk, while borrowers benefit from expanded mortgage options and potentially lower interest rates. Each entity thus plays a vital but distinct part in shaping the U.S. housing finance system.

How Ginnie Mae Impacts Homebuyers, Lenders, and the Housing Market

Ginnie Mae stands as a cornerstone in the U.S. mortgage landscape. Its influence reaches homebuyers seeking opportunity, lenders striving for stability, and the broader housing market aiming for resilience. Understanding how ginnie mae operates in each of these areas can empower you to make informed decisions, whether you are buying a home, lending, or investing.

Expanding Access to Homeownership

Ginnie mae plays a pivotal role in opening the doors of homeownership to millions. By backing loans insured by agencies like the FHA, VA, and USDA, ginnie mae enables lenders to offer mortgages with lower credit and down payment requirements.

For example, first-time buyers, veterans, and rural families often qualify for home loans with more flexible terms. In recent years, nearly 70 percent of FHA purchase loans have been backed by ginnie mae securities, underscoring its reach.

- Lower barriers to entry for young and low-income buyers

- Special mortgage programs for veterans and rural residents

- Consistent support for underserved populations

This active support means more Americans can achieve the dream of owning a home, even if they face financial hurdles.

Supporting Lender Liquidity and Stability

Lenders rely on ginnie mae to maintain strong liquidity, which is essential for a healthy mortgage market. When a lender originates a government-backed loan, they can pool it into ginnie mae securities and sell it to investors. This process quickly replenishes their capital, allowing them to offer more loans to new borrowers.

For example, during periods of high demand or economic uncertainty, ginnie mae’s guarantee provides confidence that lenders will receive timely payments. This system helps prevent credit shortages and supports a steady flow of mortgage credit.

- Lenders recycle funds efficiently

- Reduced risk of market freezes for lenders

- Greater ability to serve diverse borrowers

By keeping capital flowing, ginnie mae ensures lenders remain active participants in the housing ecosystem.

Stabilizing the U.S. Housing Market

Market stability is a hallmark of ginnie mae’s impact. By guaranteeing timely payments on mortgage-backed securities, ginnie mae cushions the market against shocks, such as recessions or financial crises. During the 2008 crisis and the COVID-19 pandemic, ginnie mae continued to support mortgage lending when private capital pulled back.

A key part of this stability comes from protecting investors against non-performing loans. Even if borrowers default, ginnie mae’s guarantee ensures investors continue to receive payments, preventing a ripple effect through the financial system.

- Steadier mortgage rates

- Reliable credit access during downturns

- Confidence for domestic and global investors

This steadfast support helps maintain trust in the housing market, benefiting both borrowers and lenders.

Ginnie Mae’s Role in Affordable Housing Initiatives

Affordable housing is central to ginnie mae’s mission. The agency partners with HUD, local governments, and non-profits to direct capital toward projects that serve low- and moderate-income families. Specialized programs also target minority, rural, and tribal communities.

For instance, ginnie mae-backed securities help finance multifamily developments and public housing improvements. These efforts result in more affordable rental options and expanded opportunities for homeownership.

- Financing for community-focused projects

- Support for housing authorities and non-profits

- Increased inventory of affordable homes

Through these partnerships, ginnie mae addresses gaps in the housing market and advances inclusive growth.

Challenges and Criticisms

Despite its many strengths, ginnie mae faces ongoing challenges. Some experts express concern about risk concentration, as the agency backs a large share of loans to higher-risk borrowers. This raises questions about taxpayer exposure, especially in periods of rising defaults.

Calls for modernization and stronger oversight are frequent topics of debate. Policymakers and stakeholders discuss how ginnie mae can adapt to evolving market risks while safeguarding public interests.

- Balancing access with financial stability

- Addressing potential vulnerabilities in loan pools

- Responding to changing regulatory expectations

These critiques drive continuous improvement, aiming to strengthen ginnie mae’s long-term resilience.

The Future of Ginnie Mae: Trends to Watch in 2026

Looking ahead, ginnie mae is embracing digital transformation. New technologies, such as digital securitization and advanced risk analytics, are streamlining processes and enhancing transparency. Policy proposals under consideration include credit risk transfer mechanisms and updated capital standards.

Demographic shifts, including more diverse and younger borrowers, are also shaping ginnie mae’s priorities. The agency’s adaptability positions it to meet the evolving needs of the U.S. housing market.

- Adoption of cutting-edge digital tools

- Enhanced risk management strategies

- Ongoing commitment to housing affordability

As 2026 approaches, ginnie mae’s evolution will continue to impact homebuyers, lenders, and the market as a whole.

Step-by-Step Guide: How Ginnie Mae Securitization Works

Understanding how ginnie mae securitization works is essential for anyone interested in the mortgage market. This step-by-step guide will walk you through the entire process, from the initial loan application to the guarantee that protects investors. Each stage plays a vital role in ensuring liquidity, stability, and investor confidence in the U.S. housing finance system.

Step 1: Loan Origination and Underwriting

The ginnie mae securitization journey begins when a borrower applies for a government-backed mortgage, such as those insured by the FHA, VA, USDA, or PIH. The lender evaluates the applicant’s financial profile, creditworthiness, and eligibility based on program guidelines.

A crucial part of this stage is underwriting, where a financial professional assesses the risk of lending to the borrower. If you want to know more, see this Definition of underwriter in finance. For example, FHA loans typically require lower down payments and more flexible credit standards, making them accessible to a broader range of homebuyers.

Once the loan is approved, it is ready to move forward in the ginnie mae process.

Step 2: Pooling Loans for Securitization

After origination, lenders group similar government-backed loans into pools. The ginnie mae process requires that each pool contains loans with comparable features, such as interest rate, loan type, and maturity term, ensuring consistency for investors.

For instance, a single-family MBS pool might include only FHA-insured loans with a fixed interest rate and similar maturity dates. This pooling step is vital, as it sets the stage for creating standardized mortgage-backed securities.

Careful organization during this phase allows ginnie mae to efficiently guarantee and manage large volumes of loans.

Step 3: Ginnie Mae Approval and Pool Issuance

With the loan pools assembled, lenders submit them to ginnie mae for review and approval. Ginnie mae performs compliance checks, verifying documentation, loan eligibility, and adherence to servicing standards.

Once approved, each pool receives a unique identifier for tracking and transparency. This step ensures that only qualified, compliant loans become part of the ginnie mae-backed securities.

By maintaining strict standards, ginnie mae protects both investors and borrowers, reinforcing the integrity of the mortgage market.

Step 4: Guarantee and Sale of MBS to Investors

Following approval, ginnie mae provides its explicit guarantee of timely principal and interest payments on the mortgage-backed securities (MBS). This government-backed assurance is a cornerstone of the ginnie mae process.

The guaranteed MBS are then sold to a wide range of investors, including pension funds, insurance companies, and individuals. The guarantee attracts investors by minimizing risk and promoting confidence in the product.

Investors’ participation provides liquidity to the mortgage market, ensuring lenders can continue making new loans under ginnie mae programs.

Step 5: Ongoing Servicing and Payment Distribution

Once the MBS are sold, servicers manage the underlying loans by collecting monthly payments from borrowers. These payments are aggregated and distributed to investors, typically on a monthly basis.

Ginnie mae oversees the servicing process to ensure accuracy, timeliness, and compliance with program standards. This ongoing management is crucial for maintaining investor trust in ginnie mae securities.

Reliable payment distribution keeps the cycle moving and supports the continuous flow of capital into the housing market.

Step 6: Prepayment, Default, and Guarantee Activation

During the life of ginnie mae-backed loans, borrowers may prepay their mortgages or, in some cases, default. Prepayment usually occurs when homeowners refinance or sell their homes, impacting the cash flow to investors.

If a borrower defaults, ginnie mae’s guarantee is activated. Investors continue to receive timely principal and interest payments, regardless of individual loan performance. This protection is a defining feature of ginnie mae securities.

By upholding its commitments, ginnie mae maintains stability and confidence throughout the mortgage-backed securities market.

As you’ve seen, understanding Ginnie Mae’s unique role in the housing market can make a real difference in how you approach investing or homeownership decisions in 2026 and beyond. If you’re eager to explore these stories further and see the bigger picture behind market movements, you’ll love getting hands-on with interactive charts, AI-powered insights, and historical context tailored just for curious minds like yours. We’re building a platform to help you spot patterns and make smarter choices by learning from the past. If you want to be among the first to experience it, Join Our Beta.