Collateralized Debt Obligation Guide: Insights for 2025

Imagine trying to make sense of today’s financial world without a clear grasp of what a collateralized debt obligation is. In a landscape shaped by volatility and rapid change, understanding this powerful financial instrument is more important than ever.

This guide offers a straightforward look at collateralized debt obligation, cutting through the jargon to explain how they work, where they came from, and why they matter. We will walk you through their structure, history, key types, risk factors, regulatory shifts, and the outlook for 2025.

Structured finance is drawing renewed attention, and collateralized debt obligation stands out both for its controversial past and current resurgence. If you want actionable insights on how to leverage or avoid the risks of these complex products, you are in the right place.

Use this guide as your foundation for smarter financial decisions in an evolving market.

Understanding Collateralized Debt Obligations: Fundamentals and Structures

Navigating the world of structured finance requires a solid grasp of the collateralized debt obligation. These financial instruments have shaped credit markets for decades, offering both innovation and complexity. Let’s break down what a collateralized debt obligation is, how it’s structured, its major types, and the key players involved.

What is a Collateralized Debt Obligation?

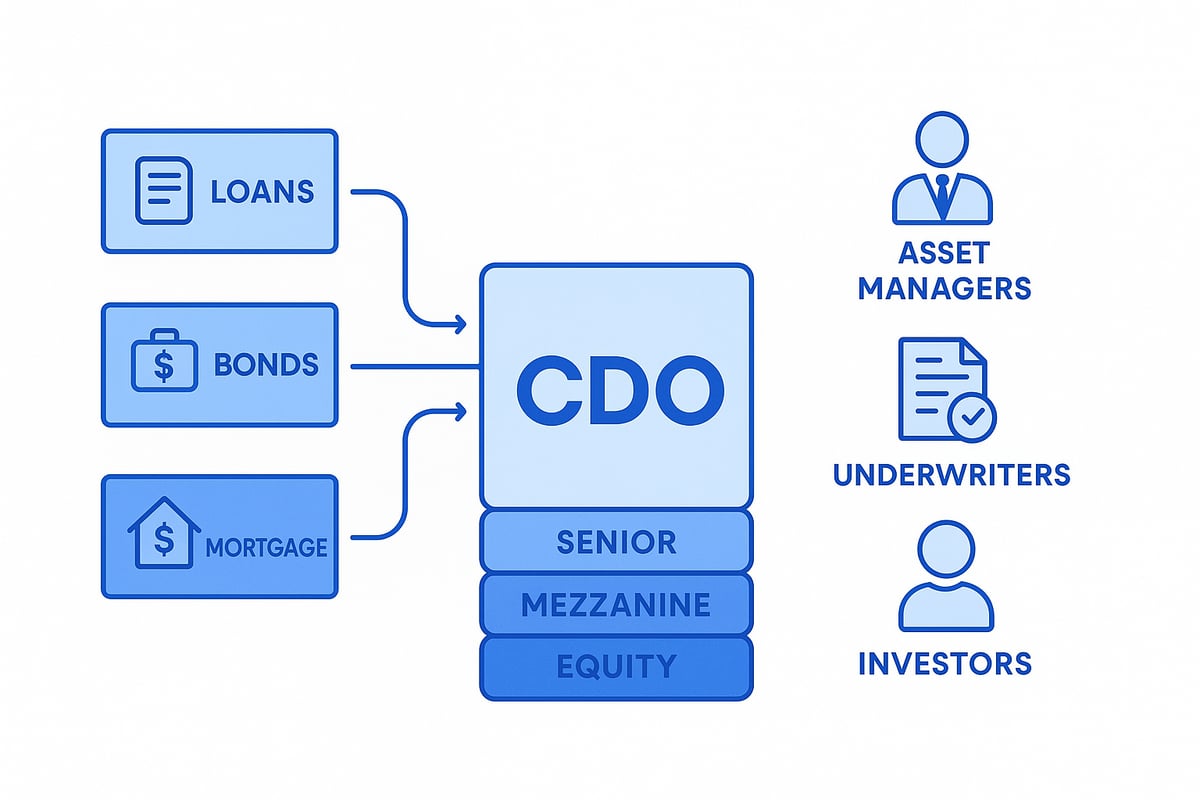

A collateralized debt obligation is a complex financial product that bundles together various debt instruments, such as loans, bonds, or mortgages, into a single security. The main purpose is to redistribute credit risk and offer investors tailored risk-return profiles.

CDOs first appeared in the 1980s, with Drexel Burnham Lambert pioneering early deals. They became popular as a tool for banks and investors to transfer risk and unlock capital. Unlike mortgage-backed or asset-backed securities, a collateralized debt obligation can be composed of diverse debt types, not just mortgages or consumer loans.

Their unique value lies in the ability to repackage risk, enabling investors to select exposures that match their preferences. For example, in 2006, CDO issuance soared to over $500 billion, highlighting their central role in modern finance.

How CDOs are Structured

The structure of a collateralized debt obligation revolves around the concept of “tranches.” Each CDO is divided into layers: senior, mezzanine, and equity. Senior tranches are paid first from the cash flows generated by the underlying assets, making them the safest, while equity tranches absorb initial losses and offer the highest potential returns.

This layering is supported by credit enhancement methods, such as overcollateralization and subordination, which improve the credit quality of the senior tranches. Funds flow through a “waterfall” structure, ensuring that senior investors are prioritized.

Collateral for a collateralized debt obligation typically includes loans, corporate bonds, or mortgages. Asset managers select and monitor these assets, while underwriters help structure and price the CDO. Trustees oversee the cash flow distribution and compliance.

A typical CDO structure allows investors to choose the risk and return profile that fits their goals. Before 2008, senior tranches of many CDOs received AAA ratings, attracting conservative investors but sometimes underestimating true risk.

Types of CDOs

There are several forms of collateralized debt obligation, each with unique features. The two main categories are cash flow CDOs, backed by actual asset payments, and synthetic CDOs, which use credit derivatives to replicate exposure to asset pools.

Further innovation led to CDOs of asset-backed securities (known as CDO^2), where the collateral itself consists of other structured products. Variants such as collateralized loan obligations (CLOs) focus on corporate loans, while collateralized bond obligations (CBOs) are backed by bonds.

For example, a mortgage-backed CDO pools home loans, while a CLO pools leveraged corporate loans. This innovation has increased both the growth and complexity of the market. In 2023, CLOs made up more than 60% of new collateralized debt obligation issuance, reflecting their popularity among institutional investors.

| Type | Collateral | Example Use Case |

|---|---|---|

| Cash Flow CDO | Loans, bonds, mortgages | Corporate lending |

| Synthetic CDO | Credit derivatives | Risk transfer, hedging |

| CDO^2 | Other ABS/CDOs | Advanced structuring |

| CLO | Corporate loans | Bank risk management |

| CBO | Corporate bonds | Yield enhancement |

Key Participants in CDO Transactions

A collateralized debt obligation involves multiple specialized participants. Institutional investors, hedge funds, and banks purchase CDO tranches based on their risk appetite. Asset managers are responsible for selecting and monitoring the underlying assets, applying specific criteria to optimize performance.

Underwriters play a crucial role in structuring the collateralized debt obligation, pricing tranches, and distributing them to investors. Trustees and collateral administrators ensure that cash flows are allocated according to the legal agreements, while accountants and legal advisors support compliance and reporting.

Some notable asset managers, like BlackRock and PGIM, have built reputations in the CDO space. However, interests among parties may not always align perfectly. For example, managers might focus on fee generation, while investors prioritize risk-adjusted returns. This dynamic underscores the importance of transparency and robust governance in the collateralized debt obligation market.

The Evolution and Market History of CDOs

The story of the collateralized debt obligation is a compelling journey through innovation, boom, crisis, and rebirth. Understanding this evolution is key to grasping the forces that shape structured finance today. Let’s trace how the collateralized debt obligation market has transformed over the decades, revealing critical lessons for investors and market participants.

The Rise of CDOs: 1980s to Early 2000s

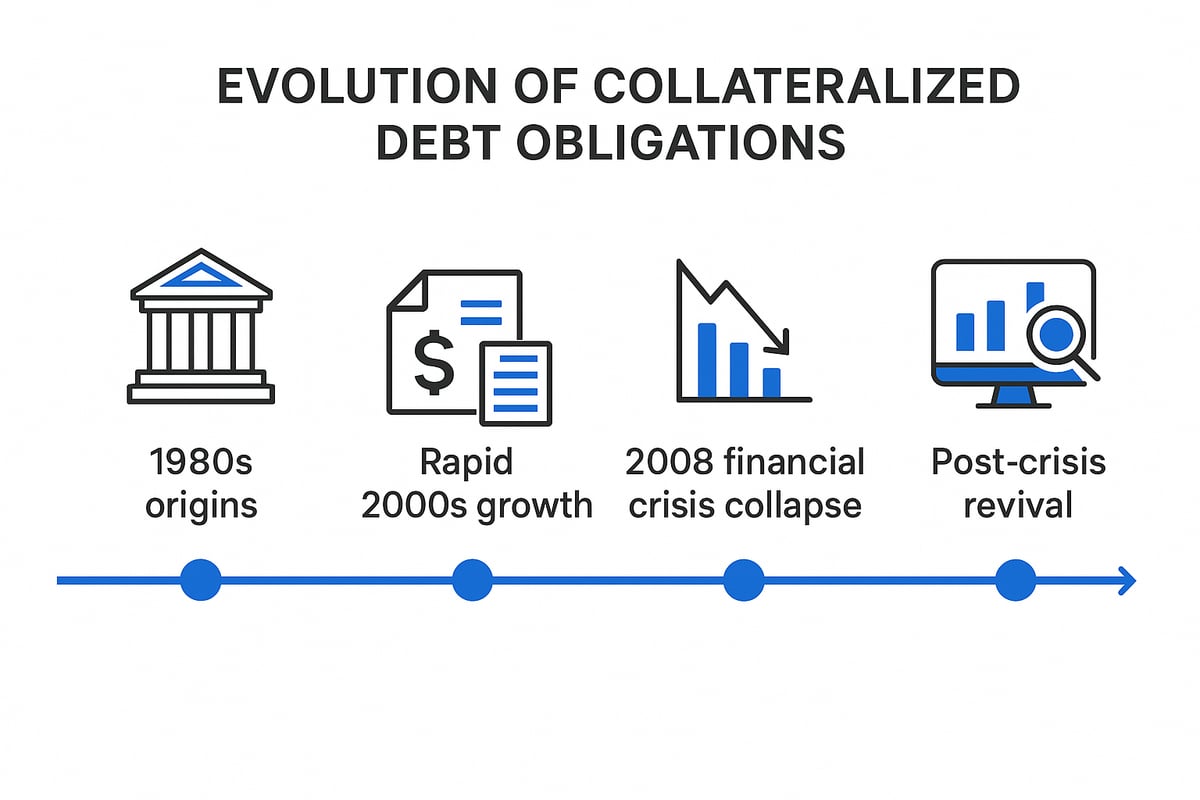

The collateralized debt obligation first appeared in the 1980s, designed as a way for banks and asset managers to repackage pools of loans and bonds. By pooling different assets, the collateralized debt obligation allowed for risk transfer and new investment opportunities.

Early growth was driven by the search for yield and the ability to shift credit risk away from banks’ balance sheets. In 1997, JP Morgan’s BISTRO deal marked a turning point, introducing a synthetic collateralized debt obligation that used derivatives to replicate credit exposure. Between 2000 and 2006, the market exploded from $69 billion to over $500 billion in annual issuance.

- Growth Drivers:

- Investor demand for higher yields

- Regulatory capital relief for banks

- Financial innovation outpacing regulation

This era cemented the collateralized debt obligation as a powerful, if complex, tool in global finance.

The Subprime Mortgage Boom and CDO Proliferation

As the 2000s progressed, the collateralized debt obligation became intertwined with the booming subprime mortgage market. Banks pooled risky mortgages and packaged them into CDOs, often slicing them into tranches to attract a wide range of investors.

Notable deals linked to firms like Countrywide and Lehman Brothers exemplified this trend. In 2006 and 2007, 56% of CDOs issued were backed by subprime mortgages. The thirst for high-yield tranches created a feedback loop, encouraging more origination of lower-quality loans.

- Key Effects:

- Complexity obscured the true level of credit risk

- Investors underestimated the correlation of defaults

- Market confidence soared despite growing vulnerabilities

This period set the stage for a dramatic unraveling.

The 2008 Financial Crisis and CDOs’ Downfall

The 2008 financial crisis exposed the fragility of the collateralized debt obligation market. As mortgage defaults surged, the value of CDO tranches plummeted, triggering massive losses. Bear Stearns’ CDO-heavy hedge funds collapsed, and cascading downgrades hit even the most senior tranches.

Between 2007 and 2010, financial institutions faced $542 billion in CDO-related losses. Public outrage and regulatory scrutiny intensified, with CDOs often blamed as the “villains” of the crisis.

- Key Lessons:

- Transparency and robust risk assessment are essential

- Overreliance on ratings can mislead investors

- Complexity without clarity increases systemic risk

The collateralized debt obligation became a symbol of unchecked financial engineering.

Post-Crisis Reforms and the Return of CDOs

In response, regulators introduced sweeping changes. Dodd-Frank, Basel III, and the Volcker Rule imposed stricter oversight, risk retention requirements, and enhanced disclosure. The collateralized debt obligation market shifted focus, with collateralized loan obligations (CLOs) and “safer” structures gaining ground, especially in Europe.

By 2023, CLO issuance climbed to $130 billion, signaling renewed confidence. Today’s CDOs emphasize transparency, improved analytics, and better alignment of interests. However, complexity and risk remain inherent features.

For a deeper dive into trends shaping the future of structured finance, including the evolving collateralized debt obligation landscape, visit Key trends driving U.S. securitized fixed income in 2025.

The collateralized debt obligation continues to adapt, reflecting both the lessons of history and the demands of a dynamic market.

How CDOs Work: Step-by-Step Process

Understanding the process behind a collateralized debt obligation helps demystify how these complex instruments are created and managed. Each phase is crucial for shaping the risk and return profile of the final product. Let’s break down the workflow into four essential steps, highlighting the roles, mechanics, and decisions involved.

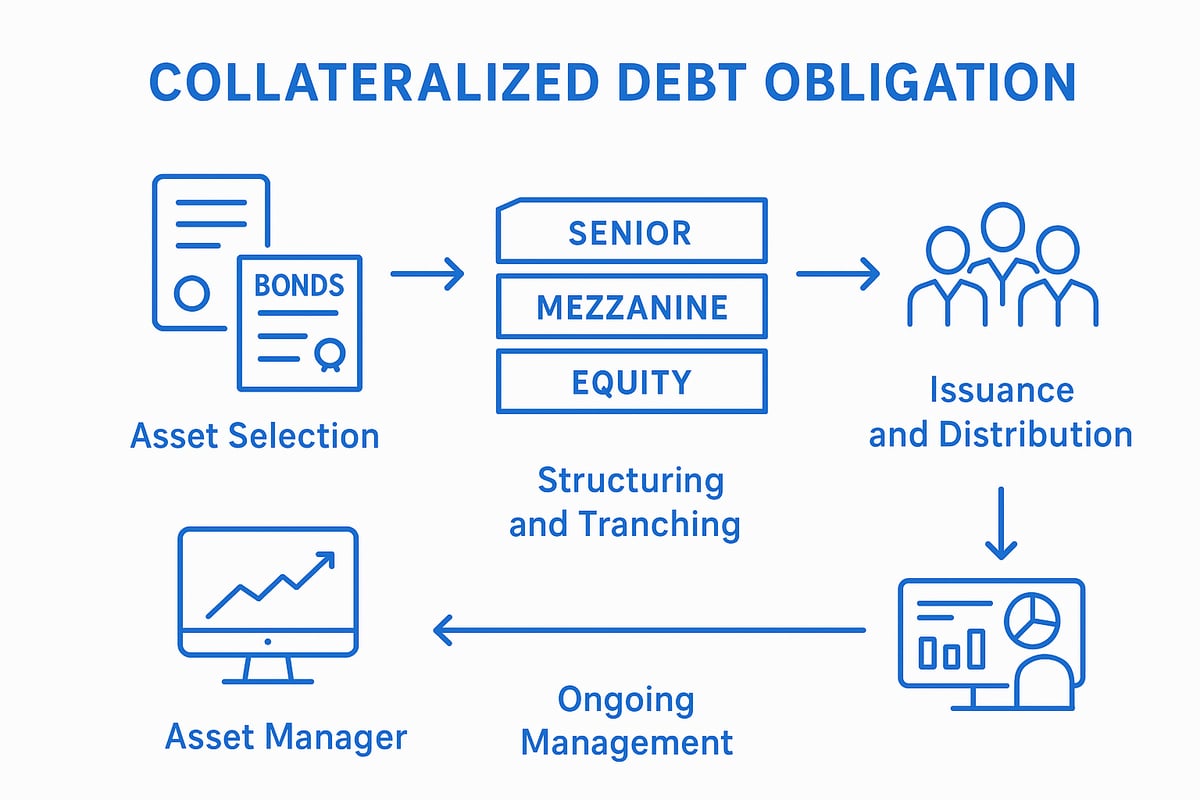

Step 1: Asset Selection and Pooling

The journey of a collateralized debt obligation begins with careful selection of underlying assets. Asset managers identify loans, bonds, or other receivables that will serve as collateral. Due diligence is paramount, focusing on credit quality, diversification, and historical performance.

For example, a CLO (collateralized loan obligation) pools corporate loans, while a traditional CDO might use mortgages. Asset selection directly influences the risk and return of the final structure. In 2023, the average pool size for CLOs reached $500 million, underscoring the scale of these deals.

The integrity of the asset pool is the foundation for everything that follows. Without strong collateral, a collateralized debt obligation cannot deliver reliable returns or attract investor confidence.

Step 2: Structuring and Tranching

Once suitable assets are pooled, the next step is structuring the collateralized debt obligation. The asset pool is divided into tranches, each representing a slice with distinct risk and return characteristics. Tranches are typically categorized as senior, mezzanine, or equity.

Credit enhancement methods, such as overcollateralization and subordination, help protect more senior tranches from losses. For instance, senior tranches carry the least risk and are paid first, while equity tranches absorb initial losses but offer higher potential returns.

Rating agencies evaluate each tranche, assigning credit ratings that influence investor demand. Tranching is a powerful tool, allowing the collateralized debt obligation to appeal to a wide range of investors with different risk appetites.

Step 3: Issuance and Distribution

With structure in place, the collateralized debt obligation moves to the issuance and distribution phase. Underwriters play a pivotal role in this stage, coordinating syndication and marketing efforts to attract institutional investors. Their expertise helps determine pricing, which reflects the risk profile of each tranche.

Senior tranches, for example, are often priced at LIBOR plus 100 basis points, attracting conservative investors. Typical investor profiles vary, with pension funds and insurance companies favoring safer tranches, while hedge funds may pursue riskier equity slices.

To learn more about the responsibilities of underwriters in this context, see the role of underwriters in finance. The success of this step hinges on matching the right investors to each tranche of the collateralized debt obligation.

Step 4: Ongoing Management and Monitoring

After issuance, the collateralized debt obligation requires active management to ensure performance. Asset managers oversee the collateral, monitor payments, and manage cash flows according to the waterfall structure, which dictates the order in which investors are paid.

If defaults occur or assets underperform, managers may substitute collateral when allowed, aiming to protect investor interests. Transparent reporting and compliance with regulatory requirements are also essential.

Active management can mitigate risks or, if handled poorly, amplify them. The ongoing oversight of a collateralized debt obligation is as critical as its initial structuring, supporting both long-term value and investor trust.

Risks, Rewards, and Criticisms of CDOs

Collateralized debt obligations occupy a unique space in the financial world. They promise attractive returns and diversification, yet also carry hidden dangers that have shaped entire markets. Understanding both the rewards and pitfalls of a collateralized debt obligation is essential for anyone considering these complex instruments.

Potential Returns and Investor Appeal

The allure of a collateralized debt obligation lies in its potential to deliver higher yields than traditional bonds. By pooling diverse assets and slicing them into tranches, CDOs offer investors a way to access risk-adjusted returns that often outperform similar credit products.

Institutional investors, like pension funds and insurance firms, have historically sought AAA-rated tranches for their safety and slight yield premium. Before the 2008 crisis, senior tranches of a collateralized debt obligation typically yielded 20 to 40 basis points above comparable Treasuries, offering a tempting blend of safety and income.

Beyond yield, CDOs also provide portfolio diversification. Investors can gain exposure to different asset classes and industries, reducing the impact of individual defaults. However, these benefits depend on the quality of the underlying collateral and the structure of each deal.

Key Risks: Credit, Market, and Structural

Despite their appeal, each collateralized debt obligation exposes investors to several layers of risk. The most prominent is credit risk—the chance that loans or bonds in the collateral pool default. When defaults spike, losses cascade through the tranches, with junior investors absorbing the first hits.

Market risk is another factor. Interest rate swings and widening credit spreads can erode the value of a collateralized debt obligation, especially for lower-rated tranches. The complexity of these products can also mask risks, making it difficult to assess true exposure.

Structural risk may be the most difficult to gauge. The intricate design of CDOs, with multiple tranches and payment waterfalls, can result in unexpected outcomes during periods of market stress. For example, in 2008, over 80 percent of subprime-backed CDO tranches were downgraded, catching many investors off guard.

Banks and investors must also consider how CDOs affect risk-weighted assets in banking, since capital requirements are closely tied to the assessed risk of these instruments. This regulatory aspect adds another dimension to the risk profile of any collateralized debt obligation.

Criticisms and Controversies

A collateralized debt obligation has faced criticism for its lack of transparency and valuation challenges. Investors often struggled to understand what assets backed their tranches, and how those assets might perform under stress.

Misaligned incentives have also been a problem. Originators and managers might prioritize deal volume or fees over asset quality, leading to conflicts with investors' interests. High-profile lawsuits by the SEC against major banks for misrepresenting CDO risks highlight these issues.

Public perception remains cautious. After 2008, CDOs were often labeled "financial weapons of mass destruction." While their design can serve useful economic purposes, skepticism persists regarding their social utility and the potential for future systemic risks.

Regulatory Oversight and Reforms

The evolution of collateralized debt obligation regulation has been significant since the global financial crisis. Laws like Dodd-Frank in the US and Basel III internationally have imposed stricter controls, including risk retention rules that require issuers to keep "skin in the game."

Enhanced disclosure and reporting standards now demand more transparency from CDO managers. The Volcker Rule, for example, restricts proprietary trading of CDOs by banks, aiming to reduce conflicts of interest and speculative risks.

In the European Union, the Securitization Regulation has further tightened oversight of structured finance products. CLOs, a major subset of the collateralized debt obligation market, are now subject to stricter risk retention and ongoing due diligence requirements.

While these steps have improved accountability, loopholes and challenges remain. As innovation in CDO structures continues, regulators and investors must adapt quickly to ensure that new risks do not undermine financial stability.

The Role of CDOs in Modern Financial Markets and Outlook for 2025

Understanding the evolving role of the collateralized debt obligation in today’s financial markets is essential for investors, risk managers, and policymakers. The landscape continues to shift, with new products, technologies, and market participants shaping opportunities and risks.

Current State of the CDO Market

The collateralized debt obligation market has experienced a significant resurgence in recent years. CLOs (collateralized loan obligations) and synthetic CDOs now dominate issuance, reflecting a shift toward higher-quality and more transparent structures.

A notable trend is the rise of ESG-linked CLOs, which integrate environmental, social, and governance criteria into deal structures. In 2024, the global CDO and CLO market size is estimated at $1 trillion, signaling robust investor demand and a broadening product mix.

For a comprehensive market analysis and forecast, including segmentation and regional outlooks, see the Collateralized Debt Obligation Market Report | Global Forecast From 2025 To 2033. The collateralized debt obligation remains a core tool for credit risk transfer and portfolio diversification.

Technological and Analytical Advances

Technology is redefining how collateralized debt obligation portfolios are analyzed and managed. Asset managers increasingly rely on AI and big data to assess collateral pools, model risk, and run scenario analyses. Advanced risk modeling tools allow for more precise measurement of default probabilities and stress testing of complex structures.

A recent industry survey found that 40 percent of asset managers now use machine learning for structured finance, underscoring the rapid pace of adoption. These platforms can identify correlations, spot anomalies, and enhance due diligence, giving managers a competitive edge.

However, increased automation can also introduce new layers of complexity, making it vital for investors to understand the models driving investment decisions within each collateralized debt obligation.

Evolving Investor Landscape

The investor base for the collateralized debt obligation has evolved, with both institutional and retail participation rising. Traditionally, banks, insurance companies, and pension funds dominated the space. In recent years, alternative investment funds and ETFs holding CDO tranches have become more prominent.

Pension funds, in particular, are increasing their CLO allocations to enhance yield and diversify portfolios. Retail investors now access the market indirectly through structured funds and ETFs, although direct exposure remains limited due to regulatory constraints.

This diversification of participants contributes to market liquidity, but also requires careful scrutiny of risk profiles and investment objectives when evaluating any collateralized debt obligation.

Key Trends and Predictions for 2025

Looking ahead, several trends are shaping the future of the collateralized debt obligation market. Growth in synthetic and ESG-linked CDOs is expected to accelerate, driven by investor demand for innovation and sustainability. Regulatory frameworks are also adapting to address emerging risks, such as those related to crypto assets and climate change.

According to projections, the global CLO market is set for a 10 percent annual growth rate through 2025, with new issuance volumes reaching record highs. For further insight into the factors driving this expansion and what it means for investors, explore the CLO market set for growth in 2025.

Market participants should remain vigilant, as innovation can both create opportunities and introduce new forms of risk in each collateralized debt obligation.

Lessons from History: Navigating the Future

History provides crucial lessons for anyone engaging with the collateralized debt obligation. The 2008 financial crisis highlighted the dangers of opacity, inadequate due diligence, and unchecked complexity. Today’s CDO structures are more transparent, with enhanced reporting and risk retention requirements.

Comparing pre-crisis and current CDO markets, improvements in oversight and analytics are evident. However, ongoing vigilance is necessary, as market cycles and product innovations can reintroduce old vulnerabilities.

Investors should prioritize transparency, rigorous analysis, and a healthy skepticism when assessing any collateralized debt obligation. Learning from the past helps market participants anticipate risks and make informed decisions as these products continue to evolve.

CDOs in Practice: Case Studies and Real-World Applications

Collateralized debt obligation structures have shaped modern finance through real-world deals, institutional strategies, and ongoing innovation. By examining case studies, portfolio applications, and analytical tools, we can see how the collateralized debt obligation continues to evolve and impact investment decisions.

Notable CDO Deals and Their Outcomes

Some of the most influential collateralized debt obligation deals have left a lasting mark on financial markets. JP Morgan’s BISTRO, launched in 1997, is often cited as the first true synthetic CDO, enabling banks to transfer credit risk without selling the underlying loans.

Magnetar Capital’s strategy before 2008 demonstrated how an opportunistic approach to CDO tranches could outperform the market. Magnetar’s funds, focused on equity tranches, managed to avoid the worst losses and even posted above-average results after the financial crisis.

These case studies highlight that the structure and timing of a collateralized debt obligation can be as critical as the underlying assets. Learning from both successes and failures is key for investors navigating this complex space.

The Role of CDOs in Institutional Portfolios

Institutional investors, such as pension funds, insurers, and banks, have long turned to the collateralized debt obligation for yield and diversification. In 2023, large European insurers increased allocations to CLOs, seeking stable cash flows and higher returns compared to traditional bonds.

A survey in 2024 found that 30% of large pension funds held CLOs in their portfolios. Due diligence and risk controls remain crucial, as the complexity of a collateralized debt obligation can mask underlying risks. For those considering new allocations, What CLO investors should know in 2025 offers timely insights on evaluating opportunities and risks.

Institutional adoption underscores the importance of robust analysis and a clear understanding of structured products’ risk-return profiles.

Innovations: ESG, Green, and Synthetic CDOs

The collateralized debt obligation market continues to innovate, especially with the rise of ESG-linked and green CLOs. The first green CLO, issued in 2022, aimed to finance environmentally sustainable projects while delivering competitive returns.

Synthetic CDOs have also evolved, allowing investors to hedge or speculate on credit risk without direct exposure to the underlying assets. In 2023, ESG-linked CDO issuance grew by 25%, reflecting growing demand for responsible investment options.

These innovations bring new opportunities but also introduce fresh layers of complexity. Investors must stay informed and adapt as the collateralized debt obligation landscape shifts toward sustainable finance and advanced risk management.

Tools and Resources for CDO Analysis

Access to reliable data and robust analytical tools is essential for anyone analyzing a collateralized debt obligation. Platforms like Bloomberg, Intex, and S&P Global provide detailed performance data, scenario analysis, and cash flow modeling for CDO portfolios.

Professional certifications, such as FMVA® and CMSA®, help analysts deepen their expertise and stay current with evolving market standards. Transparent reporting and scenario planning tools allow investors to assess risks and returns more effectively.

In an increasingly data-driven world, leveraging the right resources is vital for making informed collateralized debt obligation investment decisions.

As we’ve explored the evolving landscape of collateralized debt obligations and their impact on today’s markets, it’s clear that understanding financial history is essential for making smarter decisions in 2025 and beyond. If you’re ready to dig deeper and see how past market movements can inform your next steps, I invite you to experience our platform firsthand. Explore interactive charts, original news, and AI-powered insights designed to help you see the bigger picture. Let’s unlock the stories behind the numbers together—Join Our Beta.