Basis Point Guide: Understanding BPS in Finance 2025

Ever wondered why a 0.25% rate hike can rock global markets overnight? The answer is hidden in the small but mighty basis point. In finance, even the tiniest changes can trigger big reactions, so understanding basis point is more important than ever. This guide breaks down what a basis point means, how it’s calculated, and why it matters in 2025. We’ll explore real examples, reveal its impact across markets, and share essential tips for students and professionals. Ready to clear up the confusion? Dive in to unlock actionable insights that give you an edge.

What Is a Basis Point? The Fundamentals Explained

Understanding the concept of a basis point is fundamental in modern finance. Small percentage changes can have outsized impacts, so clarity is crucial. Let’s break down what a basis point is and why it matters.

Definition and Mathematical Breakdown

A basis point is a standardized unit in finance, representing one hundredth of a percent (0.01%) or one part per 10,000. In other words, 1 basis point = 0.01% = 0.0001 in decimal form. This small unit removes confusion when discussing rate changes that seem minor but are significant in financial contexts.

Conversions at a Glance:

| Unit | Value of 1 bp |

|---|---|

| Percent | 0.01% |

| Decimal | 0.0001 |

| Per mille (‰) | 0.1‰ |

| Permyriad (‱) | 1‱ |

Common abbreviations include "bp" for singular and "bps" for plural, pronounced as "bip" or "beep." Unicode offers the symbol U+2031 (‱) for permyriad, though it's rarely used in practice.

For example, if an interest rate of 10% increases by 25 basis points, the new rate is 10.25%. The basis point system is especially useful when sub-1% changes matter, such as in interest rates, fund expenses, or yield spreads.

To explore further, you can find a detailed breakdown with real-world examples in this What is a Basis Point? Definition & Examples resource.

Why Use Basis Points in Finance?

The basis point is a critical tool in finance because it eliminates ambiguity. When discussing changes, saying "a 50 basis point increase" always means a 0.5% absolute change, never 50% of the original rate. This precise language prevents costly miscommunication, especially when even small differences can impact millions of dollars.

Financial professionals use basis points as the industry standard for quoting adjustments in interest rates, bond yields, loan spreads, and management fees. For instance, bonds might be described as yielding "150 basis points over Treasuries," and mutual fund fees could differ by just 10 basis points.

Using basis point measurements ensures everyone is on the same page. In regulatory filings, analyst reports, and investment fund documents, basis points are the norm whenever small, but significant, changes are discussed.

Whether you’re working with derivatives, negotiating a loan, or comparing investment products, the basis point offers a level of clarity that percentages alone can’t provide.

The Role of Basis Points in Modern Financial Markets

Understanding the role of the basis point is crucial in today’s fast-moving financial world. Even the smallest rate change, measured in basis points, can ripple through markets and influence everything from central bank policy to the cost of your mortgage.

Application in Interest Rates and Monetary Policy

Central banks set the tone for global markets, and the basis point is their language of precision. When the Federal Reserve, European Central Bank, or Bank of Japan adjusts policy rates, the change is almost always quoted in basis points. For example, a 25 basis point hike means a 0.25% increase—enough to shake up stock, bond, and currency markets.

In 2024, a 25 basis point move by the Fed triggered notable market swings, underscoring just how impactful these small increments can be. Historically, central bank adjustments range from 25 to 50 basis points, but even these "tiny" changes can mean billions in altered borrowing costs across the economy.

Let’s break it down further:

- A loan quoted as “SOFR + 50 basis points” means the interest rate is the Secured Overnight Financing Rate plus 0.50%.

- Mortgage rates shifting by just 10-20 basis points can dramatically affect home affordability for thousands of buyers.

- Central bank announcements often specify basis point changes to avoid confusion, ensuring all market participants interpret the move correctly.

For a real-world example of how a 25 basis point rate cut can move the markets and influence economic decisions, see this Federal Reserve cuts rates by quarter point news story.

Basis Points in Bonds, Loans, and Spreads

The basis point is the backbone of fixed income and lending. Bond traders and analysts rely on basis points to compare yields and spreads efficiently. For instance, if a corporate bond yields 150 basis points over Treasuries, that translates to a 1.50% premium, making it easy to compare risks and returns.

Variable-rate loans are commonly priced using basis points. A bank might offer a loan at “Prime + 100 basis points,” meaning the rate is 1% above the prime rate. Swaps and derivatives also use basis points to express pricing differences, ensuring clarity in complex contracts.

Let’s look at mutual funds and ETFs:

- Expense ratios are often stated in basis points. A fund with a 20 basis point fee charges 0.20% annually.

- Investment funds fiercely compete over fee differences as small as 5-10 basis points, which can add up to substantial investor savings over time.

- In 2024, the average ETF fee stood at 19 basis points, highlighting how cost-conscious the industry has become.

Basis points allow professionals to communicate small but meaningful differences in costs, returns, and risk, making them indispensable across the financial landscape.

Preventing Misunderstandings: Absolute vs. Relative Changes

One of the most valuable aspects of the basis point is its ability to eliminate confusion. A “1% increase” could mean different things: a 1% rise from the original rate, or an increase of 1 percentage point. That’s a recipe for expensive misunderstandings.

Basis points cut through the ambiguity. For example:

- A 100 basis point increase on a 10% rate is always 11%, never 10.1%.

- Industry reports, regulatory filings, and analyst notes standardize on basis points to ensure everyone is on the same page.

- Financial professionals rely on the basis point to make precise statements about rate changes, spreads, and fees.

Here’s a quick reference table:

| Change Description | In Basis Points | In Percent |

|---|---|---|

| 0.25 percentage point change | 25 bp | 0.25% |

| 1 percentage point change | 100 bp | 1% |

| 0.05% change | 5 bp | 0.05% |

By using the basis point, the financial industry avoids costly errors, streamlines communication, and builds trust among all market participants.

Calculating and Converting Basis Points: Step-by-Step Guide

Understanding how to calculate and convert a basis point is essential for anyone in finance. These small units can represent significant changes in rates, fees, and returns. Let’s break down the process step by step, so you can confidently handle basis point math in any situation.

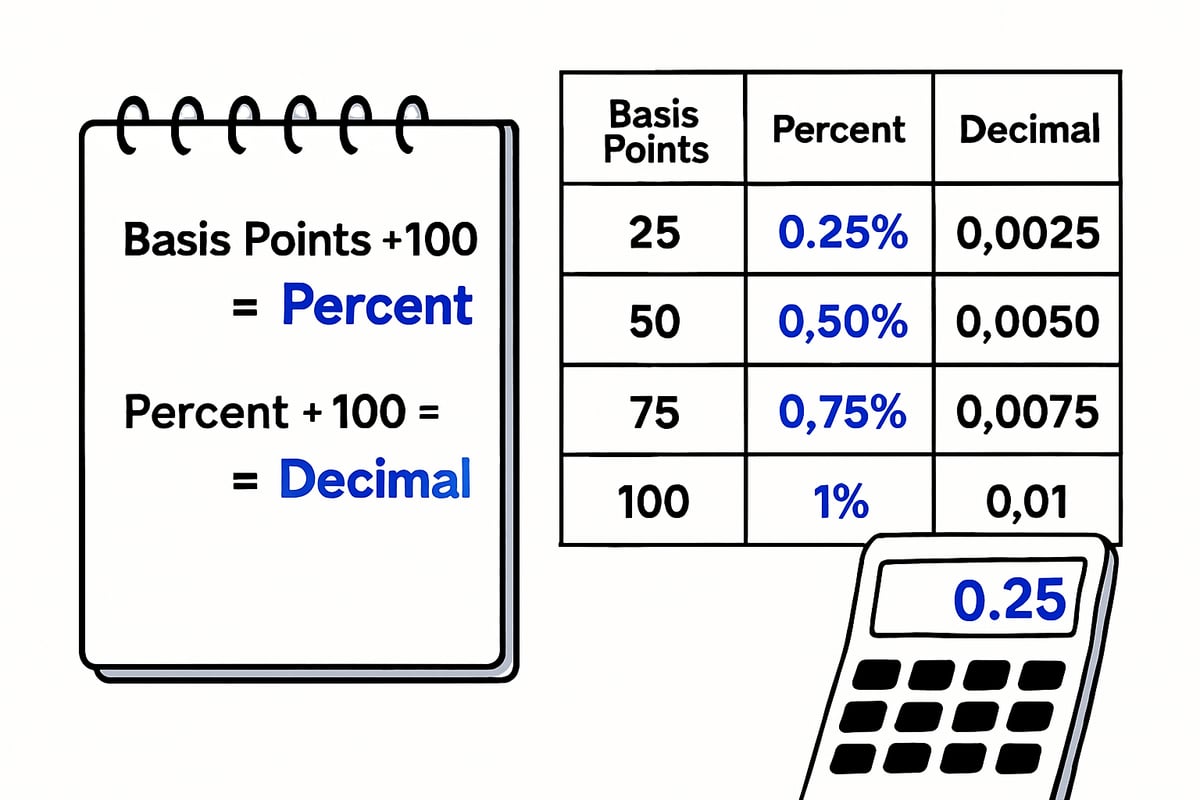

Step 1: Converting Basis Points to Percentage and Decimal

A basis point is equal to 0.01% or 0.0001 in decimal form. This simple conversion lets you quickly translate basis point changes into percentages and decimals for precise calculations.

Here’s a handy reference table:

| Basis Points | Percentage | Decimal |

|---|---|---|

| 1 | 0.01% | 0.0001 |

| 10 | 0.10% | 0.0010 |

| 50 | 0.50% | 0.0050 |

| 100 | 1.00% | 0.0100 |

| 200 | 2.00% | 0.0200 |

To convert basis points to a percentage, multiply by 0.01. For a decimal, multiply by 0.0001. For example, 75 basis points equals 0.75% or 0.0075. This method ensures you always know exactly what a basis point means in any context.

Step 2: Calculating Rate Changes Using BPS

Once you’ve converted a basis point to a percentage or decimal, applying it to real-world scenarios is straightforward. To adjust interest rates, simply add or subtract the basis point change from the original rate.

For example, if a loan’s interest rate is 4.5% and the contract specifies a 30 basis point increase, the new rate is 4.5% + 0.3% = 4.8%. This method is common in variable-rate loans, where rates are often quoted as “index + basis point spread.” You can learn more about this practice in Understanding floating rate loans.

Here’s a quick formula:

New Rate = Original Rate + (Basis Point Change × 0.01%)

This approach is vital for recalculating yields, fees, and returns in everyday finance.

Step 3: Expressing Changes in Financial Statements

Financial reports often express small changes using basis point adjustments for accuracy and clarity. For example, a bank’s income statement might state, “Net interest margin increased by 15 basis points quarter-over-quarter.”

Let’s look at a sample statement:

- “Our fund’s expense ratio dropped by 10 basis points in 2024.”

- “Loan spreads widened by 25 basis points due to market volatility.”

Industry data shows that even a shift of 5 to 10 basis points in fund fees can mean significant savings for investors. This standardized reporting ensures everyone interprets the change in the same way.

Step 4: Tools and Calculators

Modern finance relies on digital tools to streamline basis point calculations. Many online calculators and financial modeling platforms allow users to input basis point changes directly. In Excel, you can use a simple formula:

=Original_Rate + (Bp_Change * 0.0001)

For example, if the original rate is 3.75% and the change is 65 basis points:

=3.75% + (65 * 0.0001) = 4.40%

These tools help professionals and students avoid manual errors and speed up their workflow. Practicing with calculators and spreadsheets builds confidence in handling basis point adjustments.

Real-World Examples: How Basis Points Impact Finance in 2025

Ever wonder how a seemingly tiny basis point shift can trigger seismic changes in finance? Let’s break down how the basis point plays a starring role in the real world of 2025.

Central Bank Policy Announcements

Central banks like the Federal Reserve, ECB, and Bank of Japan set the tone for global markets with their policy statements. They always communicate rate changes using the basis point. In 2025, for example, the FOMC announced a 25 basis point increase, raising the benchmark rate to 5.25%.

This seemingly modest adjustment can send shockwaves through equities, bonds, and currencies. Even a 25 basis point move can alter borrowing costs for businesses and consumers alike. Market volatility often follows, as investors react to new expectations for growth and inflation. For a deeper dive into how these shifts ripple across sectors, see US sectors to watch amid Fed rate cut.

Mortgage and Loan Pricing

When it comes to personal finance, the basis point has a direct impact on affordability. Banks price loans using formulas like “Prime + 100 basis point.” A change of just 10 basis point on a $300,000 mortgage can increase monthly payments by around $25.

Over a 30-year term, that small change can add up to thousands of dollars. Lenders and borrowers closely monitor every basis point, knowing it can influence approval decisions, refinancing options, and overall homeownership costs.

| Mortgage Amount | Rate Increase | Monthly Payment Change |

|---|---|---|

| $300,000 | 10 bp | ~$25 |

| $300,000 | 20 bp | ~$50 |

Investment Fund Fees and Performance

Competition among investment funds is fierce, and the basis point is the standard measure for comparing fees. Exchange-traded funds (ETFs) and mutual funds often tout expense ratios down to the last basis point. In 2024, the average ETF fee hovered around 19 basis point, while some funds undercut rivals by as little as 5 basis point.

These differences matter. Over a decade, a fund charging 10 basis point less than another can mean thousands in extra returns for investors. The focus on the basis point helps investors make informed choices and spot value in a crowded marketplace.

Corporate Finance and M&A Deals

In corporate finance, every basis point can make or break a deal. Debt covenants, credit spreads, and premiums for mergers and acquisitions are quoted in basis points to ensure precision. For example, an acquisition loan might be priced at LIBOR + 250 basis point, affecting the cost of capital and deal structure.

A shift of even 25 basis point can alter the economics of a multi-million-dollar deal. Companies, banks, and investors rely on the basis point to negotiate terms and evaluate risks without ambiguity.

International Currency and Bond Markets

The global stage is filled with transactions where the basis point is the language of choice. Emerging market bonds are typically priced with basis point spreads over US Treasuries, reflecting risk and return. Currency swaps and hedges also use basis point to quantify costs and benefits.

In volatile markets, a few basis point can mean the difference between profit and loss. Financial professionals track every movement, knowing that precision with the basis point is essential for cross-border deals and risk management.

Basis Points vs. Other Units: Permyriad, Percentage Points, and Pips

Understanding the difference between a basis point, permyriad, percentage points, per mille, and pips is essential for anyone delving into finance. While these terms may seem interchangeable at first glance, each serves a unique purpose and is best suited for specific contexts.

A basis point equals 0.01%, or one one-hundredth of a percent. It’s commonly abbreviated as bp or bps and is the go-to unit for expressing small changes in interest rates, yields, and fees. Permyriad (‱) represents one part per 10,000, but is rarely used in practical finance. Percentage points, in contrast, indicate the absolute difference between two percentages: if a rate moves from 5% to 6%, that's a 1 percentage point change, or 100 basis points. Per mille (‰) means one part per thousand (0.1%) and typically appears in scientific or statistical contexts, not finance. Pips, short for "percentage in point," are used primarily in foreign exchange markets to show price movements, with one pip usually equal to 0.0001 in major currency pairs.

For a comprehensive look at these and other terms, check out the Financial terms glossary.

Understanding Related Units

Let’s break down the key units:

- Basis point: 0.01% (1/10,000), used for rate changes.

- Permyriad (‱): 0.01%, same value as a basis point but rarely used in finance.

- Percentage point: The absolute difference between two percentages (e.g., 7% to 8% = 1 percentage point).

- Per mille (‰): 0.1% (1/1,000), more common in demographics or science.

- Pip: 0.0001, standard in FX trading.

Each unit provides clarity in different scenarios. For example, a basis point is ideal when describing small, precise shifts in financial instruments, while percentage points are better when comparing two overall rates.

Comparing Use Cases

When should you use a basis point instead of another unit? Here’s a quick guide:

- Basis point: Quoting interest rate changes, bond spreads, or fund expense ratios.

- Percentage point: Describing changes in inflation or unemployment rates.

- Pip: Expressing FX market movements.

- Permyriad/per mille: Rarely used in mainstream finance.

Using the correct unit prevents costly misunderstandings. For instance, saying a loan rate rose by 100 basis points (not 1 percentage point) avoids confusion about the size of the change.

Industry best practices recommend using a basis point for any change below 1%, especially in regulatory documents and financial news.

Visualizing Differences

To make these differences clear, here’s a quick reference table:

| Unit | Value | Example Use Case |

|---|---|---|

| Basis Point (bp) | 0.01% (1/10,000) | Interest rate changes |

| Permyriad (‱) | 0.01% (1/10,000) | Rare in finance |

| Percentage Point | 1% (1/100) | Inflation change |

| Per Mille (‰) | 0.1% (1/1,000) | Demographic stats |

| Pip | 0.01% or 0.0001 | FX trading |

For example, if a bond yield rises by 25 basis points, that’s a 0.25% increase, while a 25 pip move in EUR/USD means the currency pair shifted by 0.0025. Understanding these distinctions ensures accuracy in financial modeling and reporting.

Basis Points in Financial Modeling, Reporting, and Communication

Financial professionals rely on the basis point for precision in modeling, reporting, and investor communication. With even small changes influencing billion-dollar decisions, using the basis point ensures clarity and consistency across financial documents and models.

Financial Modeling Applications

In financial modeling, the basis point is essential for stress-testing scenarios and building accurate projections. Debt schedules often use the basis point to model interest expense sensitivity. For example, a 25 basis point increase in borrowing costs can significantly impact projected net income.

Scenario analysis in leveraged buyout (LBO) models frequently tests the effect of 25-100 basis point shifts on returns. Sensitivity tables are commonly set in basis point increments to help decision-makers understand risk.

Changes in the debt-to-equity ratio explained are also influenced by movements in rates, which are typically measured in basis point units. This approach allows analysts to quickly gauge the effect of rate changes on leverage and capital structure.

Reporting and Investor Communication

In financial reporting, the basis point standardizes how small changes are communicated. Regulatory filings, like 10-Ks and prospectuses, use the basis point to report changes in yields, fees, and spreads. For example, a mutual fund might announce a 10 basis point reduction in its expense ratio, making the cost difference clear to investors.

Analyst reports routinely highlight basis point changes in margins or yields, allowing readers to compare performance across periods and companies. Fund marketing materials emphasize low fees using the basis point for transparency.

By using the basis point, companies avoid confusion and maintain trust with stakeholders. This standardized language ensures precise, apples-to-apples comparisons in all investor communications.

Avoiding Costly Misunderstandings

Misinterpreting a percentage change versus a basis point adjustment can lead to significant errors. For instance, a "1% increase" in a rate could be read as either a 1 percentage point rise or a 1 percent relative change. Using the basis point eliminates this ambiguity.

Case studies reveal that misunderstanding the basis point has resulted in costly mistakes for firms and clients. To prevent such errors, financial institutions invest in training staff to use the basis point correctly in all discussions and documentation.

Recent surveys indicate 80% of finance professionals prefer the basis point for clarity. Emphasizing the basis point in both written and verbal communication is now best practice across the industry.

The Future of Basis Points: Trends and Best Practices for 2025

The financial world is changing fast, and the basis point is at the center of this transformation. As interest rates hover near historic lows, even a minor shift in basis point can have ripple effects across markets and portfolios. For investors, bankers, and students alike, understanding the evolving role of basis point is crucial for success in 2025.

Increasing Importance in a Low-Rate Environment

In recent years, global central banks have shifted their focus to smaller, more precise adjustments. A change of just 10 or 25 basis point can now trigger significant market movement. With rates staying low, the impact of each basis point is amplified, affecting everything from mortgage costs to investment yields.

For example, a 15 basis point adjustment on a large loan can alter annual interest expense by thousands of dollars. As a result, professionals pay close attention to every basis point, knowing that even the smallest change matters.

Automation and Digital Tools

Technology is reshaping how the basis point is used in finance. Modern trading platforms, portfolio management tools, and even online loan calculators now allow users to input and analyze changes in basis point directly. This automation reduces errors, speeds up calculations, and ensures consistency across financial operations.

Financial modeling software, such as Excel and specialized apps, often features built-in functions for basis point adjustments. These advances help both professionals and students make more informed decisions and adapt quickly to market shifts.

Regulatory and Industry Shifts

Regulators worldwide are emphasizing transparency and consistency in financial reporting. Agencies like the SEC and ESMA now require explicit disclosure of changes in basis point in key documents, ensuring all stakeholders interpret data the same way.

This push for clarity is also driving fee competition among investment funds, with differences of just a few basis point becoming a major selling point. For a deeper explanation of the value and uses of basis point, see Basis Point: Meaning, Value, and Uses.

Education, Professional Development, and Best Practices

Finance education is evolving to meet the demands of this new environment. Programs and certifications, such as the CFA, now place greater emphasis on basis point concepts and calculations. Job interviews and exams often test candidates on their ability to interpret and communicate basis point changes accurately.

Best practices for 2025:

- Always specify if a change is in basis point or percent.

- Use basis point in all financial communication.

- Stay current on regulatory requirements related to basis point disclosure.

| Best Practice | Why It Matters |

|---|---|

| Clarify units (bp vs %) | Prevents costly miscommunication |

| Use bp in reporting | Meets industry and regulatory standards |

| Stay educated on bp trends | Enhances professional credibility |

Mastering the basis point is no longer optional—it's a must-have skill for anyone navigating the future of finance.

Now that you’ve seen how understanding basis points can make sense of even the smallest shifts in the financial markets, imagine exploring the stories behind those movements with real historical context. Whether you’re a student, an investor, or just curious about the forces shaping finance, our new platform lets you interact with charts, dive into AI-powered summaries, and connect the dots between past and present. If you want to spot patterns, learn from history, and see finance through a whole new lens, Join Our Beta and help us shape the future of financial storytelling.