Accrual Accounting Guide: Mastering Financial Reporting 2025

Unlock the potential of accurate financial reporting in 2025 by embracing accrual accounting, a critical tool for any business aiming for clarity and compliance. As financial landscapes become more complex, understanding accrual accounting is essential for making informed decisions and meeting regulatory standards.

This guide offers a clear roadmap to mastering accrual accounting, ensuring your financial reports truly reflect your company’s performance. You will explore core principles, advantages over cash accounting, the latest regulatory updates, and strategies to optimize your reporting.

Ready to elevate your financial transparency? Discover actionable steps and expert insights to transform your accrual accounting practices for success in 2025.

Understanding Accrual Accounting: The Foundation of Modern Financial Reporting

Accrual accounting is the backbone of transparent financial reporting. It provides a precise snapshot of a company's financial health by capturing the true timing of business transactions. Understanding this method is essential for anyone aiming to master financial reporting in 2025.

Defining Accrual Accounting

Accrual accounting records revenues and expenses when they are earned or incurred, regardless of when cash is exchanged. Unlike cash accounting, which only tracks transactions when money changes hands, accrual accounting captures the economic reality of business activities.

For example, if your business delivers a product in December but receives payment in January, accrual accounting recognizes the revenue in December. This method ensures that financial statements reflect what actually happened within each period, offering a more accurate view of business performance.

Harvard Business School Online highlights that accrual accounting provides a clearer picture of profitability and obligations than cash methods.

Core Principles of Accrual Accounting

The foundation of accrual accounting rests on two main principles:

- Revenue Recognition Principle: Record revenue when it is earned, not when cash is received.

- Matching Principle: Match expenses to the revenues they help generate in the same period.

These principles impact financial statements by ensuring income and costs align with the correct periods. For instance, prepaid expenses or deferred revenue in accrual accounting are recognized over time, not just when paid or received. This alignment ensures comparability across periods and prevents misleading spikes or drops in reported profits.

Why Accrual Accounting Matters in 2025

Business transactions are growing more complex, with multi-stage sales, subscriptions, and global operations becoming the norm. Regulatory bodies like the SEC and IFRS increasingly demand transparency, making accrual accounting indispensable.

By tracking earned revenue and incurred expenses, accrual accounting enables better forecasting, resource allocation, and compliance. Public companies, as well as many growing SMEs, are required to use this method. According to Harvard Business School Online, over 90% of large firms rely on accrual accounting for their financial reporting.

Key Differences: Accrual vs. Cash Accounting

Understanding the distinctions between accrual accounting and cash accounting is crucial. The table below summarizes the main differences:

| Aspect | Accrual Accounting | Cash Accounting |

|---|---|---|

| Revenue Recognition | When earned | When cash is received |

| Expense Recognition | When incurred | When cash is paid |

| Impact on Profit Reporting | Reflects actual business activity | May misalign income and costs |

| Suitability | Medium/Large, complex businesses | Small, simple operations |

| Compliance | Often required by law | Limited to small businesses |

For example, a service business may recognize income when services are delivered, even if payment arrives later, which is only possible with accrual accounting.

Real-World Example: Accrual Accounting in Action

Consider a tech company offering annual subscriptions. With accrual accounting, it records revenue monthly as the service is provided, not all at once when payment is received. This approach ensures financial statements accurately reflect performance and improves investor confidence.

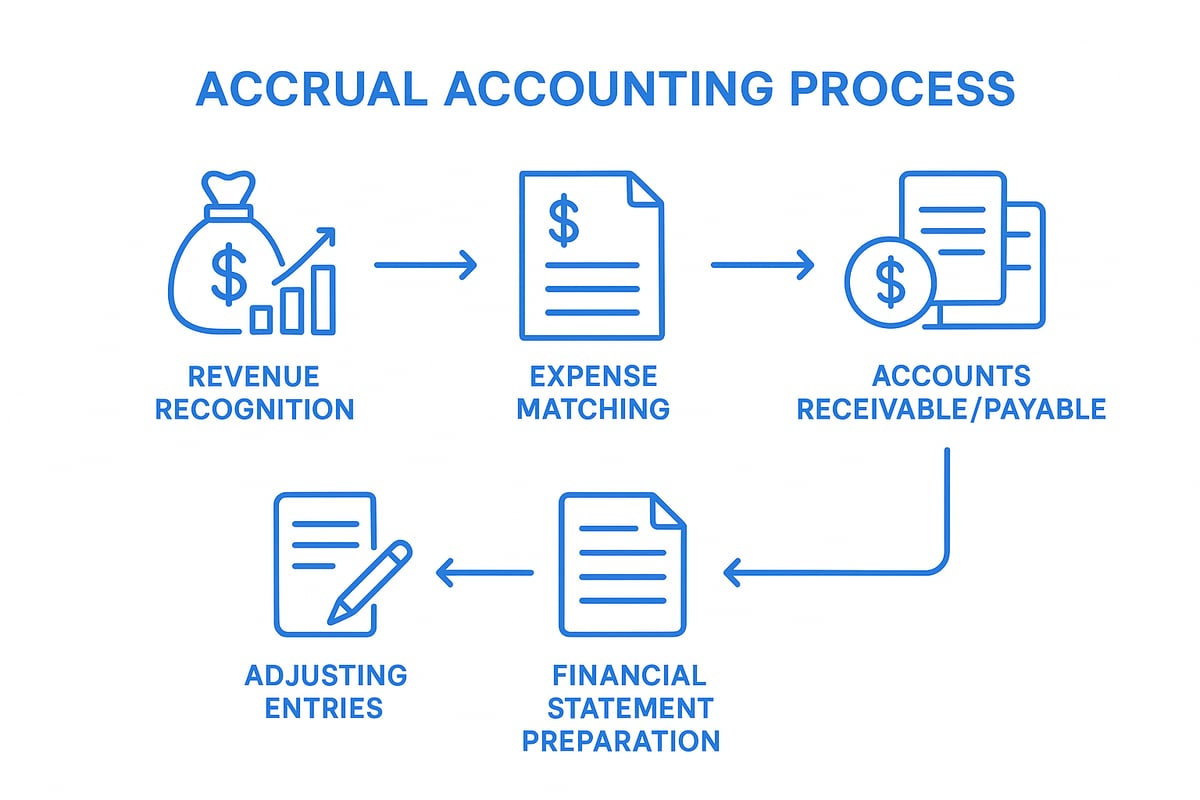

The Mechanics of Accrual Accounting: Step-by-Step Guide

Unlocking the full potential of accrual accounting requires a solid grasp of its mechanics. By following a systematic approach, you can ensure your financial data reflects the true economic activity of your business. Let us walk through each essential step to master this process.

Step 1: Identify and Record Revenue

The first step in accrual accounting is to recognize revenue as soon as it is earned, not when cash is received. This means tracking sales when goods are delivered or services are performed, even if payment arrives later.

For example, if your consulting firm completes a project in March but receives payment in April, the revenue is recorded in March. This approach allows your financial statements to present a clear picture of operational performance.

To implement this, maintain detailed records of all contracts, delivery dates, and billing cycles. Many businesses use invoicing software to automate the tracking of earned but unpaid revenue, ensuring nothing is missed during the period.

Step 2: Track and Match Expenses

Accrual accounting demands that expenses are recorded when incurred, regardless of payment timing. This aligns with the matching principle, which matches each expense to the revenue it helped generate.

Suppose your company uses electricity in December but pays the bill in January. Under accrual accounting, the expense is recorded in December, matching it to the period when the benefit was received. This method impacts earnings before interest and taxes (EBIT), as explained in the Matching principle and expense timing resource.

Tracking expenses accurately requires diligent recordkeeping and periodic reviews of outstanding bills. This ensures your profit calculations are reliable and reflect the true cost of doing business.

Step 3: Manage Accounts Receivable and Payable

Managing accounts receivable and payable is central to accrual accounting. Accounts receivable (AR) tracks money owed to your business, while accounts payable (AP) monitors amounts you owe to suppliers.

Set up AR and AP ledgers to monitor outstanding invoices and bills in real time. This improves cash flow management and helps you prioritize payments or collections. Regularly review these ledgers to identify overdue accounts and take timely action.

Best practices include setting clear payment terms, sending reminders for unpaid invoices, and negotiating favorable terms with vendors. These steps help minimize late payments and maintain healthy working capital.

Step 4: Adjusting Entries and Period-End Close

At the end of each accounting period, adjusting entries are essential for accuracy. These include accruals, deferrals, and depreciation, which ensure all revenues and expenses are recorded in the correct period.

For instance, if you accrue interest expense at year-end for a loan not yet paid, this entry aligns your financial data with actual obligations. The period-end close process involves reviewing all accounts, posting adjustments, and verifying completeness.

A monthly or quarterly closing checklist is invaluable. It ensures no transactions are overlooked and that your financial records are up to date, supporting informed decision-making and compliance.

Step 5: Prepare Accurate Financial Statements

The final step in accrual accounting is preparing financial statements that reflect economic reality. This includes the income statement, balance sheet, and cash flow statement.

Use accounting software to automate report generation and ensure compliance with GAAP or IFRS standards. Review each statement for accuracy, confirming that all revenues, expenses, assets, and liabilities are properly accounted for.

Accurate financial statements provide stakeholders with a transparent view of business performance. This level of detail is critical for regulatory compliance, investor confidence, and strategic planning.

Benefits of Accrual Accounting for Businesses in 2025

Unlocking the full potential of your business starts with transparent and accurate financial reporting. Adopting accrual accounting in 2025 offers a range of powerful benefits that help organizations of all sizes navigate an increasingly complex financial landscape. Let us explore why moving to accrual accounting is a strategic decision for growth, compliance, and financial clarity.

Improved Financial Accuracy and Insights

Accrual accounting provides a comprehensive view of your company’s financial health by capturing revenues and expenses when they are earned or incurred. This method ensures that financial statements reflect the true economic activity of your business, not just cash movements.

For example, with accrual accounting, you can identify declining sales trends before they impact your cash flow. This early warning system supports proactive decision-making. By leveraging this approach, management can spot issues and opportunities swiftly, leading to better outcomes. If you want to clarify key concepts as you review your reports, consult helpful resources like Financial terms for business reporting to strengthen your understanding.

Enhanced Compliance and Credibility

Regulatory bodies require public companies and many medium-sized enterprises to use accrual accounting for transparent reporting. This method helps your organization fulfill legal obligations, reducing the risk of audits and penalties.

Accrual accounting also builds trust with investors, lenders, and other stakeholders. Accurate records show that your business meets industry standards and is prepared for scrutiny. In fact, public companies in the United States must use this method as mandated by the SEC. Demonstrating compliance enhances your credibility and opens doors to additional growth opportunities.

Facilitates Business Growth and Scalability

As your business expands, transactions become more complex and may span multiple locations, currencies, or entities. Accrual accounting is designed to handle this complexity, making it easier to manage growth and streamline operations.

For instance, e-commerce businesses benefit from accrual accounting by accurately tracking global sales, managing inventory, and consolidating financial data. This method supports mergers, acquisitions, and new market entries, ensuring your financial systems keep pace with your ambitions. The scalability of accrual accounting makes it a strong foundation for long-term success.

Better Cash Flow Management and Planning

Effective cash flow management is essential for sustainability. Accrual accounting enables more accurate forecasting and budgeting by aligning income and expenses with the periods in which they occur.

With this system, businesses can identify upcoming cash needs and surpluses more precisely. For example, planning for large inventory purchases becomes straightforward, as you have a clear picture of future obligations and receivables. This foresight empowers you to make informed decisions, allocate resources wisely, and avoid unexpected shortfalls.

Key Challenges and Solutions in Implementing Accrual Accounting

Implementing accrual accounting can transform financial reporting accuracy, but the transition is not without challenges. Businesses often encounter hurdles related to processes, systems, and compliance. Understanding these obstacles and applying targeted solutions ensures a smoother path to reliable accrual accounting.

Common Implementation Hurdles

Transitioning to accrual accounting introduces several common obstacles. Many businesses struggle to shift from cash-based methods, especially when legacy habits persist. Training staff on new concepts and processes can be time-consuming and resource-intensive.

Data migration is another major hurdle. Ensuring accuracy during the transfer of historical financial data is critical to avoid errors in the new accrual accounting system. Small businesses may face additional challenges, such as adapting to new software or lacking in-house expertise. Overcoming these hurdles requires careful planning, patience, and a commitment to education.

Overcoming Data and System Integration Issues

A key aspect of successful accrual accounting is integrating the system with existing ERP or CRM platforms. Seamless data flow between modules is essential for real-time reporting and accuracy. However, mismatched systems or manual processes can lead to delays and errors.

Automating invoice tracking and reconciliation reduces human error and increases efficiency. Staying up-to-date with Recent Trends in Accounting and Information System Research provides valuable insights into overcoming these integration challenges and leveraging technology to optimize accrual accounting workflows.

Managing Complexity in Multi-Entity or International Operations

For organizations with multiple entities or international operations, accrual accounting becomes even more complex. Managing transactions across different currencies and jurisdictions requires robust systems and clear protocols.

Consolidating financial statements while ensuring compliance with both local and international standards is essential. Accrual accounting supports this process, but only when systems are designed to handle the unique demands of global business. Regular reviews and updates to policies help maintain consistency and accuracy.

Avoiding Common Mistakes and Errors

Mistakes in accrual accounting can undermine the integrity of financial reports. Frequent errors include misclassifying revenue or expenses, missing necessary adjusting entries, and failing to reconcile accounts regularly.

| Common Mistake | Impact on Reporting |

|---|---|

| Misclassifying revenue | Inaccurate profit figures |

| Overlooking adjustments | Distorted period results |

| Missed reconciliations | Unreliable balances |

For example, missing an accrual at year-end can significantly affect reported results. To minimize errors, establish rigorous review procedures and foster a culture of attention to detail.

Best Practices for a Smooth Transition

A successful switch to accrual accounting starts with a clear, stepwise migration plan. Train staff at all levels to ensure everyone understands new procedures and principles. Leverage accounting software with robust accrual features to automate routine tasks and minimize manual effort.

Set up strong internal controls and maintain detailed audit trails to support transparency and compliance. Ongoing support and regular assessments help sustain improvements and ensure that accrual accounting delivers its full benefits.

Regulatory Updates and Trends in Accrual Accounting for 2025

As 2025 approaches, accrual accounting continues to evolve, shaped by new regulations, technological advancements, and broader reporting expectations. Staying informed about these changes is essential for accurate financial reporting and long-term business success.

Recent Changes in Accounting Standards

The landscape for accrual accounting is shifting due to updates in both GAAP and IFRS. Key changes include the ongoing adoption of ASC 606 and IFRS 15, which standardize revenue recognition across industries. For many businesses, these updates mean revising how and when revenue is reported, requiring careful review of contracts and internal processes.

Deadlines for compliance are firm, especially for public companies and those operating internationally. Staying compliant with these standards helps ensure financial statements accurately reflect business performance, reducing the risk of misstatements and regulatory penalties.

Technology and Automation in Accrual Accounting

Technology is playing a central role in modern accrual accounting. Businesses now leverage AI-powered platforms and cloud-based accounting software to automate complex processes, such as adjusting entries and reconciling accounts. These tools significantly reduce manual errors and free up finance teams to focus on analysis rather than data entry.

Automated systems also improve real-time visibility into financial data, supporting faster and more informed decision-making. As automation becomes more prevalent, companies adopting these solutions gain a competitive edge in accuracy and efficiency.

Environmental, Social, and Governance (ESG) Reporting

ESG factors are increasingly integrated into accrual accounting frameworks, as regulators push for greater transparency in sustainability practices. Companies are now expected to include metrics like carbon credits and environmental liabilities in their financial statements, using accrual methods to track obligations and benefits over time.

This trend highlights the growing importance of clear, comprehensive reporting. For a deeper look at how evolving standards can improve business communication and societal impact, see Understanding and Improving the Language of Business. Integrating ESG data ensures businesses meet new disclosure requirements and build trust with stakeholders.

Preparing for Future Changes

Regulatory environments are never static, and businesses must remain agile to adapt to new rules in accrual accounting. Ongoing professional development, regular review of authoritative resources, and consultation with industry experts are vital. Organizations like AICPA, FASB, and IASB provide timely updates and guidance for navigating future changes.

Being proactive in monitoring trends and regulatory shifts ensures continued compliance and positions companies for success in a rapidly changing financial landscape.

Accrual Accounting Best Practices: Strategies for Mastering Financial Reporting

Mastering accrual accounting requires a strategic approach to controls, technology, people, and process. The following best practices will help you elevate your financial reporting and ensure ongoing compliance in 2025.

Establish Robust Internal Controls

Strong internal controls are the backbone of effective accrual accounting. Start by assigning clear responsibilities for recording, reviewing, and approving transactions. This segregation of duties prevents errors and reduces the risk of fraud.

Regular audits and reconciliations are essential. Establish a schedule to review accounts payable, accounts receivable, and adjusting entries. Use checklists to ensure all necessary steps are followed during period-end closes.

Here is a simple table summarizing key controls for accrual accounting:

| Control Area | Best Practice |

|---|---|

| Segregation of Duties | Assign roles for entry, approval, review |

| Reconciliations | Monthly review of key accounts |

| Approval Processes | Require dual sign-off for significant entries |

By maintaining robust controls, you ensure your accrual accounting records are accurate and reliable, supporting trustworthy financial statements.

Use Technology to Streamline Processes

Modern accounting software is vital for efficient accrual accounting. Choose platforms that automate recurring accruals, adjusting entries, and reconciliations. Look for features like real-time dashboards, approval workflows, and seamless integration with other business systems.

Automation reduces manual errors and saves valuable time. Cloud-based solutions enable secure access from anywhere, supporting collaboration across teams and locations.

For deeper insight into how technology shapes accounting systems and internal controls, review the Highlights of Accounting Systems Research. Implementing these technological advancements will help your organization keep pace with regulatory demands and financial best practices.

Train and Empower Your Finance Team

Your team’s expertise is crucial to successful accrual accounting. Invest in ongoing training on core principles, new standards, and evolving technology. Encourage staff to attend workshops and pursue certifications relevant to accrual accounting.

Cross-training helps ensure continuity during absences or transitions. Empower team members to identify process improvements and share knowledge.

Consider organizing regular sessions to review changes in revenue recognition or adjusting entry procedures. A knowledgeable finance team will drive accuracy and consistency in your accrual accounting operations.

Align Accrual Accounting with Strategic Planning

Integrate accrual accounting data directly into your strategic planning. Use timely accrual-based reports to inform budgeting and forecasting. This approach enables leadership to make proactive decisions based on accurate, forward-looking financial information.

Scenario analysis becomes more powerful when built on accrual data. For example, use historical accrual trends to predict cash flow needs or assess the impact of new investments.

Aligning your accounting practices with business strategy ensures that financial reporting is not just compliant, but also a catalyst for growth and informed decision-making.

Monitor Key Performance Indicators (KPIs)

Tracking the right KPIs is essential in accrual accounting. Focus on metrics like days sales outstanding (DSO), accrued liabilities, and operating margin. These indicators provide early warnings of emerging issues and highlight areas for improvement.

For a deeper understanding of how accrual accounting impacts operating margin, explore Operating margin and financial analysis. Monitoring these KPIs regularly enables continuous improvement and supports transparent communication with stakeholders.

Use dashboards to visualize trends over time, and schedule periodic reviews to discuss results with your finance team.

Engage with Professional Advisors and Auditors

External advisors and auditors bring valuable perspective to your accrual accounting processes. Engage them early to address complex transactions, regulatory changes, or unusual events.

Regular consultations help ensure ongoing compliance with GAAP or IFRS standards. Advisors can also support internal staff training and help prepare for annual audits.

By fostering strong relationships with external experts, you minimize risk and gain confidence in the accuracy of your financial reporting.

Case Study: Successful Accrual Accounting Transformation

A mid-sized SaaS company transitioned from cash to accrual accounting to improve investor confidence. By implementing robust controls, leveraging cloud-based software, and monitoring key KPIs, the firm achieved more accurate financial statements.

This transformation enhanced their credibility, streamlined audits, and enabled better strategic decisions, demonstrating the tangible benefits of mastering accrual accounting.

Frequently Asked Questions about Accrual Accounting in 2025

Staying ahead with accrual accounting means understanding its practical impact on your business. Here are answers to the most common questions organizations face as they adapt to financial reporting requirements in 2025.

What types of businesses should use accrual accounting?

Accrual accounting is required for most public companies and organizations with complex operations. Businesses that carry inventory, extend credit, or have multiple revenue streams benefit from this method. It provides a clearer picture of financial health than cash accounting, especially for growing enterprises.

Small businesses and sole proprietors may qualify for cash accounting, but as operations expand, accrual accounting becomes essential. Regulatory bodies often mandate its use for compliance and transparency. If your business is scaling or seeking outside investment, accrual accounting is the recommended choice.

How does accrual accounting impact taxes?

Accrual accounting affects when income and expenses are recognized for tax purposes. Income is reported when earned, and expenses are deducted when incurred, regardless of cash movement. This timing difference can impact tax liabilities, especially at year-end.

The IRS requires accrual accounting for certain entities, such as corporations with gross receipts above a set threshold or those holding inventory. Strategic use of accrual accounting allows businesses to better align taxable income with actual business performance. Consulting with a tax professional ensures you maximize deductions and remain compliant.

What software solutions support accrual accounting?

Many leading accounting platforms are designed for accrual accounting. Popular options include QuickBooks, Xero, and NetSuite. These tools automate revenue recognition, track accounts receivable and payable, and generate accurate financial reports.

When choosing software, look for features like automated adjusting entries, customizable reporting, and seamless integration with other business systems. Cloud-based solutions enable real-time access and collaboration across teams. Selecting the right software streamlines accrual accounting processes and supports growth.

How can businesses ensure compliance with evolving standards?

Staying compliant with new accrual accounting regulations requires ongoing education and proactive management. Regular staff training, timely software updates, and monitoring of regulatory changes are essential steps. Collaboration with professional advisors and auditors helps address complex issues.

Businesses in government or nonprofit sectors can benefit from utilizing Research Resources from the American Accounting Association to stay informed about sector-specific standards and best practices. Engaging with these resources ensures your accrual accounting remains accurate and meets all reporting requirements.

As you’ve seen throughout this guide, understanding and implementing accrual accounting is essential for mastering financial reporting in 2025 and beyond. With new technological tools and evolving standards, it’s more important than ever to ground your analysis in both modern methods and historical context. If you’re passionate about uncovering the stories behind market movements and want to experience financial data in a new, interactive way, I invite you to Join Our Beta. Together, we can explore the past to make smarter decisions for the future—one insight at a time.