Options Contract: Understanding Financial Derivatives

An options contract represents one of the most versatile financial instruments in modern markets, providing traders and investors with the ability to control large positions with limited capital while managing risk. These derivative securities have evolved from simple agreements between merchants in ancient civilizations to sophisticated financial tools traded on regulated exchanges worldwide. Understanding options contracts requires examining their structure, mechanics, and the historical context that shaped their development into the essential market instruments they are today.

The Fundamental Structure of Options Contracts

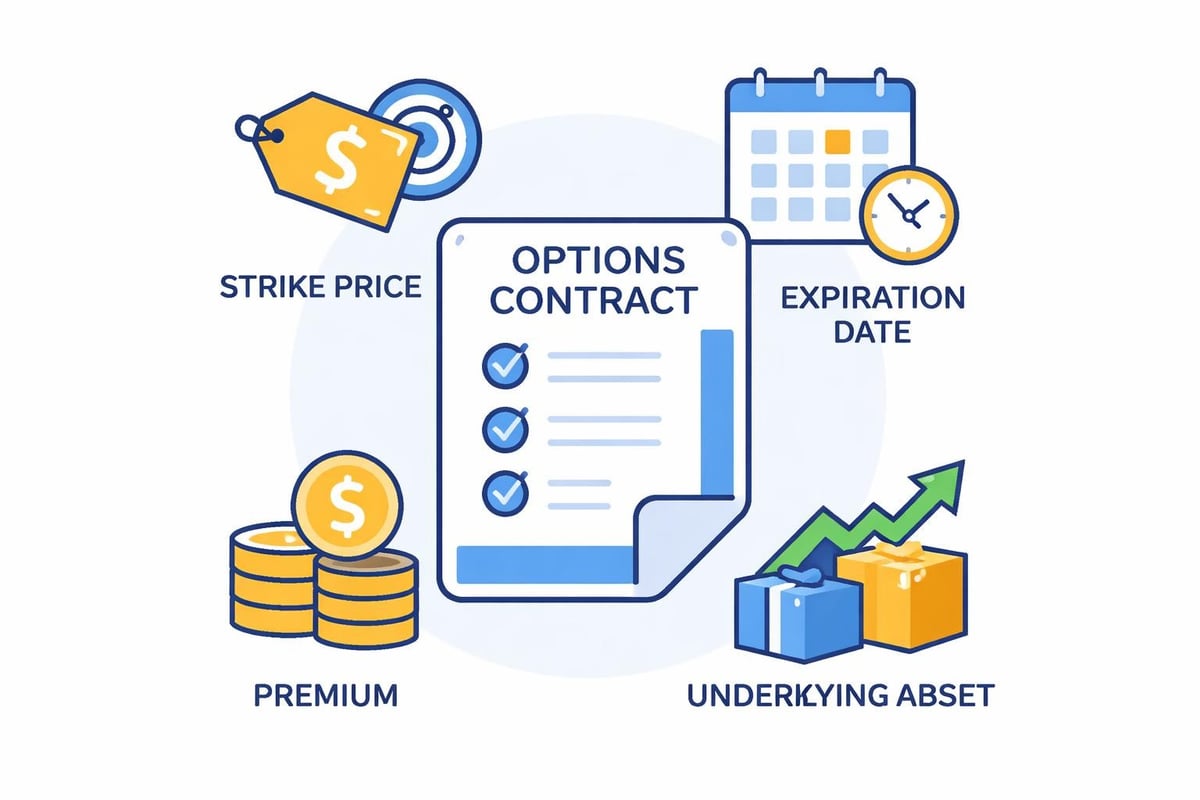

An options contract is a legally binding agreement that grants the buyer the right, but not the obligation, to buy or sell an underlying asset at a predetermined price within a specified timeframe. This fundamental characteristic distinguishes options from other financial instruments and provides unique strategic opportunities for market participants.

The contract specifies several critical components that define its terms. The strike price establishes the price at which the underlying asset can be bought or sold, while the expiration date sets the deadline for exercising the right. The premium represents the cost the buyer pays to acquire this right, and the underlying asset can range from stocks and bonds to commodities and currencies.

Call and Put Options

Options contracts divide into two primary categories that serve opposite market perspectives. Call options grant the holder the right to purchase the underlying asset at the strike price, benefiting when prices rise above this level. Conversely, put options provide the right to sell the underlying asset at the strike price, profiting when prices fall below this threshold.

Each type serves distinct strategic purposes:

- Call options allow investors to participate in upside potential with limited downside risk

- Put options provide portfolio protection or enable speculation on declining prices

- Both types can be bought or sold, creating four basic positions (long call, short call, long put, short put)

- The interplay between these positions enables complex multi-leg strategies

The legal framework governing options has developed over centuries to ensure enforceability and standardization, making these contracts reliable instruments for transferring risk between willing parties.

Historical Evolution and Market Development

The history of options contracts stretches back further than most investors realize. Ancient Greek philosopher Thales reportedly used options on olive presses to profit from an anticipated harvest, demonstrating the timeless appeal of leveraged speculation. However, modern options markets began taking shape in the seventeenth century with Dutch tulip traders who created contracts resembling contemporary options.

The real transformation occurred in 1973 when the Chicago Board Options Exchange (CBOE) opened, establishing the first regulated marketplace for standardized options contracts. This development revolutionized derivatives trading by introducing:

| Innovation | Impact |

|---|---|

| Standardized contracts | Improved liquidity and price discovery |

| Central clearing | Reduced counterparty risk |

| Regulated environment | Enhanced investor confidence |

| Transparent pricing | Fair market valuations |

The Options Clearing Corporation plays a crucial role in maintaining market integrity by issuing and guaranteeing all listed options contracts, ensuring that sellers fulfill their obligations even if individual parties default.

Regulatory Framework Development

Options contract regulation has evolved significantly since the 1970s to protect investors while maintaining market efficiency. The FINRA regulations governing options establish requirements for broker-dealers, ensuring that participants understand the risks involved in these complex instruments.

The Commodity Futures Trading Commission has also shaped the regulatory landscape, particularly for agricultural commodity options and other derivatives products. These regulations balance market innovation with investor protection, creating frameworks that have allowed options markets to flourish while managing systemic risks.

Pricing Mechanisms and Market Dynamics

Understanding how options contracts derive their value requires examining the factors that influence pricing. The Black-Scholes model, introduced in 1973, revolutionized options pricing by providing a mathematical framework for calculating theoretical values. This breakthrough earned its creators the Nobel Prize in Economics and fundamentally changed how markets approach derivatives.

Several variables determine an option's premium at any given moment:

- Underlying asset price relative to the strike price determines intrinsic value

- Time until expiration affects the option's time value component

- Implied volatility reflects market expectations for future price fluctuations

- Interest rates influence the cost of carrying positions

- Dividend expectations impact the relative value of calls versus puts

These factors interact dynamically as market conditions change, creating opportunities for traders who can accurately assess how shifts in one variable might affect option values. Much like how convertible bonds offer hybrid characteristics, options contracts blend elements of insurance, speculation, and strategic positioning.

Intrinsic Value Versus Time Value

Every options contract's premium divides into two components that behave differently as expiration approaches. Intrinsic value represents the amount an option would be worth if exercised immediately, calculated as the difference between the underlying asset's current price and the strike price (for in-the-money options).

Time value, also called extrinsic value, reflects the potential for the option to gain additional intrinsic value before expiration. This component decreases as expiration nears, a phenomenon known as time decay or theta. Understanding this relationship helps investors select appropriate strategies based on their market outlook and time horizon.

Strategic Applications in Portfolio Management

Options contracts serve multiple purposes beyond simple directional speculation. Sophisticated investors employ these instruments to enhance returns, generate income, and manage risk across diverse market conditions. The versatility of options makes them valuable tools for implementing nuanced investment strategies.

Protective puts function as portfolio insurance, allowing investors to maintain stock positions while limiting downside exposure. By purchasing put options on holdings, investors establish a floor price below which losses cannot accumulate, similar to how homeowners insurance protects property value.

Covered calls generate additional income by selling call options against existing stock positions. This strategy works well in neutral to slightly bullish markets, providing premium income while capping potential upside. Many income-focused investors integrate covered calls into their overall approach to enhance cash flow from portfolio holdings.

Advanced Multi-Leg Strategies

Experienced traders combine multiple options contracts to create positions with specific risk-reward characteristics. These strategies include:

- Vertical spreads that limit both maximum profit and maximum loss

- Iron condors designed to profit from low volatility and range-bound markets

- Butterflies that target specific price levels with limited risk

- Straddles and strangles that benefit from significant price movements regardless of direction

Each strategy responds differently to changes in the underlying asset's price, volatility, and time decay. Historical analysis reveals patterns in how these strategies performed during various market environments, providing valuable insights for contemporary implementation.

Historical Case Studies and Market Events

Examining how options contracts functioned during significant market events illuminates their practical impact and risks. The 1987 stock market crash demonstrated both the protective power of put options and the dangers of portfolio insurance strategies implemented at scale. As markets plunged, put options soared in value, protecting those who held them while exposing writers to enormous losses.

The 1998 collapse of Long-Term Capital Management highlighted risks inherent in complex derivatives positions, including options contracts leveraged across global markets. The hedge fund's sophisticated strategies, based partly on options arbitrage, unraveled when market volatility exceeded historical models' assumptions.

More recently, the 2008 financial crisis showcased how options on various underlying assets, including mortgage-backed securities, could amplify systemic risks when correlated positions moved simultaneously. These historical episodes emphasize the importance of understanding not just individual options mechanics but also how widespread options use affects broader market dynamics.

Lessons from Historical Volatility Spikes

Market history reveals recurring patterns in options behavior during crisis periods. Volatility typically spikes during market stress, dramatically increasing options premiums and creating opportunities for those positioned correctly while devastating unprepared participants.

| Event | Year | Impact on Options Markets |

|---|---|---|

| Black Monday | 1987 | Put options surged 500%+ in value |

| Dot-com Bubble Burst | 2000-2002 | Extended high volatility period |

| Financial Crisis | 2008 | VIX reached record highs above 80 |

| COVID-19 Pandemic | 2020 | Rapid volatility spike and recovery |

Understanding these historical patterns helps investors recognize similar conditions and adjust strategies accordingly. The efficient market hypothesis suggests markets incorporate available information, yet options markets sometimes anticipate or react to events in ways that create temporary dislocations.

Expiration and Settlement Procedures

Every options contract reaches its expiration date, triggering predetermined settlement procedures that vary based on contract specifications. Most equity options expire on the third Friday of the expiration month, though weekly options and other variations exist. Understanding settlement mechanics prevents costly surprises and enables proper position management.

American-style options allow exercise at any time before expiration, providing flexibility but complicating pricing models. European-style options permit exercise only at expiration, simplifying calculations but limiting strategic options. Most equity options use American-style exercise, while many index options follow European conventions.

Settlement itself occurs through either physical delivery or cash settlement. Physical settlement requires actual delivery of the underlying asset, while cash settlement exchanges only the monetary difference between strike price and market price. Index options typically use cash settlement since delivering a basket of stocks proves impractical.

Risk Considerations and Market Implications

Options contracts carry substantial risks that demand careful consideration before trading. Unlike stock ownership, which can theoretically be held indefinitely, options have finite lifespans that guarantee total loss if they expire worthless. This characteristic makes timing crucial and adds complexity beyond simple directional bets.

Leverage amplifies both gains and losses, allowing small price movements to generate significant percentage returns or losses on options positions. A stock moving 5% might cause a corresponding option to move 25% or more, depending on various factors. This magnification attracts speculators but increases risk for unprepared investors.

Liquidity varies widely across different options contracts. Heavily traded stocks typically feature liquid options markets with tight bid-ask spreads, while thinly traded underlying assets may have options that are difficult to enter or exit at fair prices. This consideration affects both execution costs and the ability to adjust positions as market conditions change.

Regulatory bodies continue adapting frameworks to address evolving risks in options markets. The basic concepts of option contracts remain consistent, but implementation details and available strategies continue expanding as markets develop new products and trading mechanisms.

Modern Market Infrastructure and Technology

Today's options markets bear little resemblance to the trading floor environments of the 1970s and 1980s. Electronic trading platforms have replaced open outcry systems, enabling faster execution, improved transparency, and access for retail investors previously excluded from options markets. This technological transformation has democratized options trading while introducing new considerations.

High-frequency trading algorithms now dominate options market-making, providing liquidity but occasionally creating flash crashes or unusual price dislocations. These systems can process thousands of quotes per second, adjusting prices based on complex models that incorporate real-time data from multiple markets simultaneously.

The development of combinatorial options markets represents cutting-edge research into more sophisticated market structures that could further improve pricing efficiency and strategic possibilities. These advances build upon decades of market evolution, creating increasingly complex ecosystems that require both historical understanding and current market awareness.

Recent innovations also include options on non-traditional underlying assets, from cryptocurrencies to volatility indexes themselves. These products extend options principles into new domains, creating opportunities while introducing risks that lack extensive historical precedent. Similar to how forward contracts evolved to meet specific hedging needs, options continue adapting to serve changing market demands.

Trading volume in options has exploded over recent decades, with millions of contracts changing hands daily across global exchanges. This growth reflects both increased institutional usage and expanding retail participation, fundamentally changing market dynamics and creating new patterns for historical analysis. Understanding how current markets differ from past environments helps investors contextualize contemporary price action and volatility patterns.

Options contracts have fundamentally shaped modern financial markets, providing essential tools for risk management, speculation, and strategic investing across multiple asset classes. By understanding their historical development, structural components, and practical applications, investors gain crucial context for interpreting market movements and implementing informed strategies. Historic Financial News empowers you to explore how options contracts influenced pivotal market events through interactive historical charts and AI-powered analysis, helping you recognize patterns and learn from past market dynamics to make better-informed decisions today.