Commercial Paper Guide: Essential Insights for 2025

As global financial markets enter a period of rapid transformation, understanding commercial paper is more crucial than ever for 2025. Businesses and investors alike are seeking flexible, short-term solutions to adapt to shifting economic conditions.

This comprehensive guide demystifies commercial paper, equipping you with essential knowledge on its definition, issuance, risk management, and the latest regulatory updates. Whether you are an issuer or an investor, mastering these insights can help you navigate the evolving landscape with confidence.

Leverage this guide to make informed decisions in the coming year and seize new opportunities in modern finance.

Understanding Commercial Paper: Definition, Types, and Key Features

Commercial paper stands as a cornerstone of modern money markets, serving as a flexible, short-term financing tool for corporations and financial institutions worldwide. At its core, commercial paper is an unsecured, short-term promissory note issued by companies with strong credit ratings. These instruments typically mature in one to 270 days, making them ideal for bridging temporary funding gaps.

For a comprehensive overview, see this Commercial Paper resource, which details its structure, history, and role in global finance.

The primary function of commercial paper is to provide quick, cost-effective funding for working capital needs. Issuers use it to cover payroll, inventory purchases, and other operating expenses, while investors gain access to a relatively low-risk, short-duration asset.

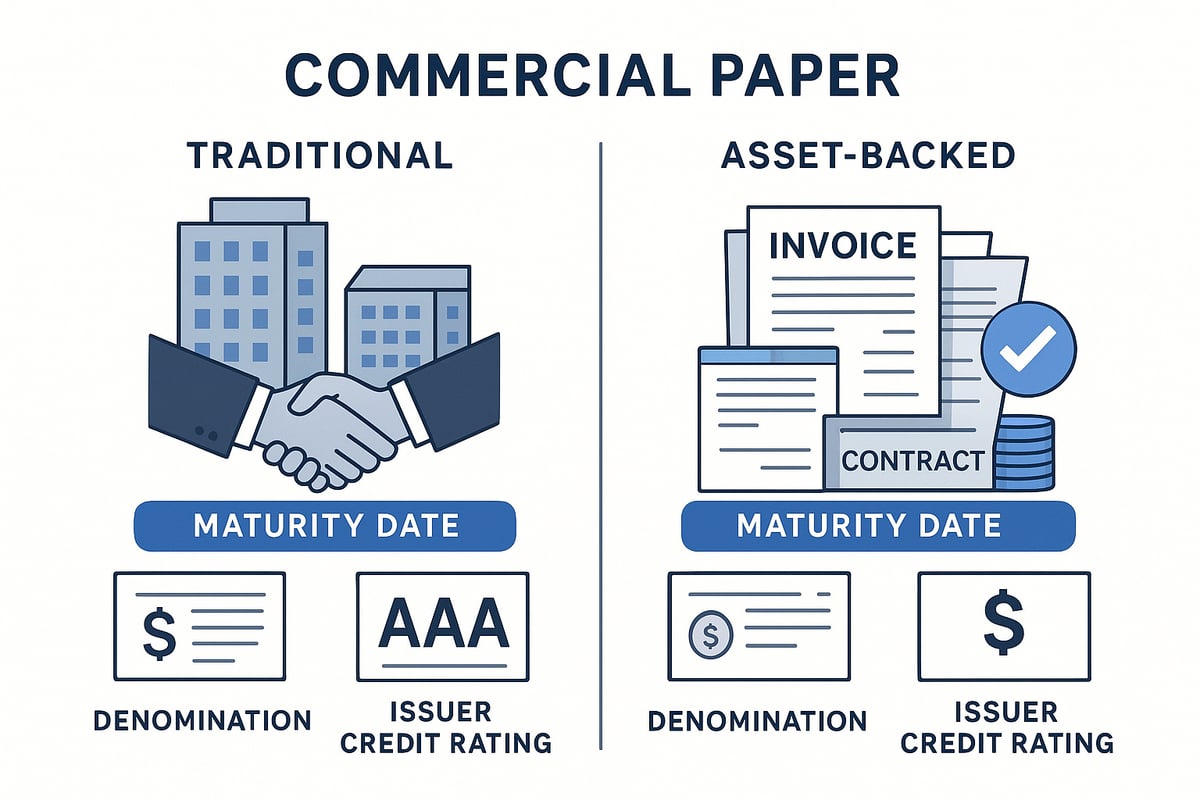

There are two main types of commercial paper: traditional and asset-backed commercial paper (ABCP). Traditional commercial paper is backed solely by the issuer's promise to pay, relying heavily on their creditworthiness. In contrast, ABCP is secured by a pool of underlying assets, such as receivables or loans, offering an extra layer of investor protection.

Here is a simple comparison:

| Feature | Traditional Commercial Paper | Asset-Backed Commercial Paper (ABCP) |

|---|---|---|

| Backing | Issuer’s creditworthiness | Pool of underlying assets |

| Typical Issuers | Large corporations, banks | Special purpose vehicles (SPVs) |

| Use Case | Working capital | Funding receivables, trade finance |

| Risk Profile | Credit risk of issuer | Asset and structural risk |

Key features that define commercial paper include its unsecured status, dependence on issuer credit quality, and appeal to institutional investors and money market funds. Because it is not backed by collateral, only companies with high credit ratings—often rated by agencies like Moody’s, S&P, or Fitch—are able to issue commercial paper at competitive rates.

Major issuers of commercial paper are typically large, well-established corporations and financial institutions. Names like General Electric, JPMorgan Chase, and multinational conglomerates frequently appear in the market. These firms use commercial paper programs to manage liquidity efficiently and avoid the higher costs of bank loans.

One notable regulatory aspect is the exemption from SEC registration for commercial paper with maturities under 270 days. This exemption streamlines issuance, reduces administrative burdens, and encourages more frequent use for short-term financing.

Denominations of commercial paper usually start at $100,000 and can reach much higher amounts, catering primarily to institutional buyers. Issuance formats vary, with most commercial paper sold at a discount and redeemed at face value, though some may offer explicit interest payments.

Global market statistics highlight the significance of commercial paper. The worldwide market has shown steady growth, with recent reports projecting the commercial paper market to approach $350 billion by 2030. In 2023 alone, issuance volumes surged in response to rising corporate liquidity demands and favorable interest rate conditions.

Understanding these foundational elements is crucial for anyone looking to navigate or invest in the commercial paper market in 2025. Staying informed about the types, features, and evolving trends will position both issuers and investors for success in the dynamic financial landscape.

The Role of Commercial Paper in Modern Financial Markets

Commercial paper plays a pivotal role in supporting the flow of funds in today’s financial landscape. As the need for flexible, short-term financing and investment options grows, both issuers and investors are turning to commercial paper for its efficiency and adaptability.

Importance for Issuers

For corporate issuers, commercial paper serves as a vital funding source for short-term needs like working capital, payroll, and inventory management. By issuing commercial paper, companies can quickly secure financing at competitive rates, often lower than traditional bank loans. This cost-effectiveness is especially appealing for firms with strong credit ratings.

Many large corporations implement rolling commercial paper programs, allowing them to continuously refinance maturing notes and maintain liquidity. This approach enables efficient cash flow management and reduces reliance on long-term debt. In recent years, even tech companies and non-financial firms have increasingly adopted commercial paper as part of their treasury strategies, reflecting the instrument’s growing versatility and appeal.

The flexibility, speed, and lower borrowing costs of commercial paper make it a cornerstone of modern corporate finance, helping issuers manage their short-term obligations with confidence.

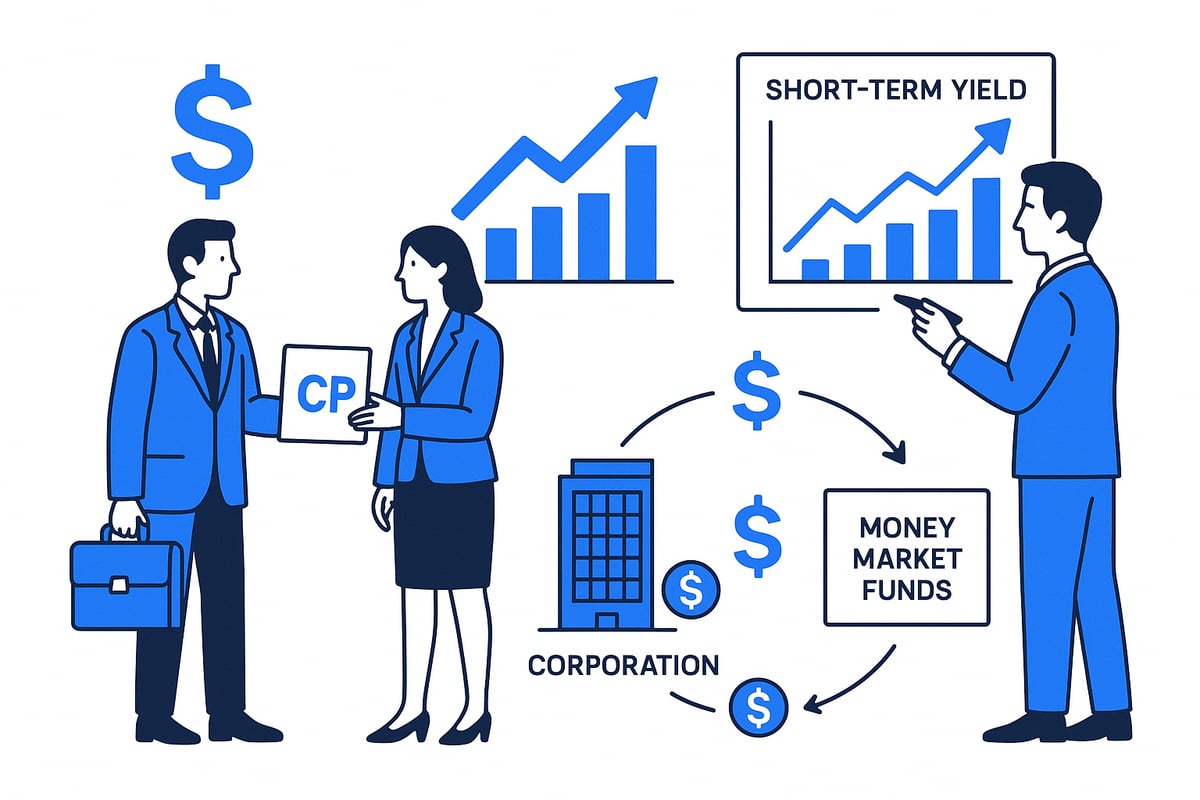

Value for Investors

Institutional investors, such as money market funds and pension funds, favor commercial paper for its attractive risk-return profile. Compared to government securities or bank deposits, commercial paper typically offers higher yields without significantly increasing risk, especially when issued by top-rated entities.

A major advantage is the ability to diversify portfolios with short-term instruments that match liability schedules. Investors can choose commercial paper with maturities and denominations tailored to their needs, enhancing liquidity management. The steady demand from institutional buyers also supports market stability.

| Investment Option | Typical Yield (%) | Liquidity | Risk Level |

|---|---|---|---|

| Commercial Paper | 4.2 – 5.0 | High | Low–Medium |

| Treasury Bills | 3.8 – 4.3 | High | Very Low |

| Bank Deposits | 3.0 – 3.5 | High | Very Low |

Commercial paper’s share in money market funds remains significant, underlining its role as a preferred choice for short-term investing and portfolio diversification.

Economic Impact and Market Dynamics

Commercial paper is essential for promoting market liquidity and efficient capital allocation. By enabling companies to access short-term funding, commercial paper supports ongoing business operations and investment, which in turn fuels economic growth.

The interconnectedness between commercial paper markets and the banking sector enhances overall financial stability. During periods of market stress, such as the 2008 financial crisis or the COVID-19 liquidity crunch, central banks have intervened to support commercial paper markets, highlighting their systemic importance.

Recent data reflects robust growth, with the commercial paper market projected to reach $350 billion by 2030. Despite occasional fluctuations in investor demand, default rates for high-quality issuers remain historically low. As market dynamics evolve, commercial paper continues to adapt, reinforcing its status as a cornerstone of global financial markets.

How Commercial Paper Is Issued: Step-by-Step Guide for 2025

Issuing commercial paper in 2025 requires a clear understanding of evolving market practices and regulatory requirements. This guide walks through each step, from establishing eligibility to ongoing management, ensuring both issuers and investors navigate the process with confidence.

Step 1: Assessing Eligibility and Creditworthiness

The foundation of any commercial paper program is the issuer’s financial strength. Only firms with robust balance sheets and strong reputations can access this market. Rating agencies such as Moody’s, S&P, and Fitch evaluate an organization’s creditworthiness, assigning ratings that signal risk to investors.

Typically, a minimum short-term rating of A-2/P-2/F2 is required for issuers to offer commercial paper at competitive rates. These ratings reflect the likelihood that the issuer will meet its short-term obligations. Companies regularly monitor their credit profiles, as downgrades can impact both pricing and market access.

Step 2: Structuring the Commercial Paper Program

Once eligibility is established, the issuer must determine the optimal structure for their commercial paper program. Key decisions include the maturity profile (ranging from a few days up to 270 days), denominations, and issuance frequency. Some firms prefer open-ended programs that allow for continuous issuance, while others opt for fixed-term arrangements.

Backup lines of credit from banks are commonly secured to assure investors that liquidity will be available if needed. These structural choices directly affect the flexibility, cost, and appeal of the commercial paper program.

Step 3: Regulatory and Legal Compliance

Compliance is essential for any commercial paper issuance. In the United States, commercial paper with maturities under 270 days is exempt from SEC registration, simplifying the process for issuers. However, documentation requirements and rules can vary by jurisdiction, so global issuers must stay informed about local regulations.

For asset-backed commercial paper (ABCP), specialized legal structures are required to safeguard investor interests. Legal counsel ensures all offering documents, disclosures, and contracts meet regulatory standards, minimizing the risk of legal challenges.

Step 4: Distribution and Placement

Distribution is a critical phase in the commercial paper issuance process. Issuers can choose between direct placement, where they sell directly to investors, and dealer-placed programs, which involve intermediaries like investment banks and brokers. Digital platforms are becoming increasingly popular, streamlining the placement process and expanding access to a broader investor base.

A successful strategy often involves a combination of these channels to maximize reach and pricing efficiency. The primary market overview offers valuable insight into the mechanisms behind the initial sale of commercial paper, highlighting the importance of strong relationships and market timing for effective placement.

Step 5: Ongoing Program Management and Rollover

Once commercial paper has been issued, ongoing management is vital for maintaining market confidence. Issuers closely monitor market conditions and investor sentiment to determine the best timing for rolling over maturing paper. Effective communication and transparent reporting are key to sustaining investor trust.

Common challenges include fluctuating interest rates and shifts in demand, which can impact rollover success. On average, large issuers report high rollover rates, but contingency plans, such as backup credit lines, are essential for navigating periods of market stress. Proactive management ensures that commercial paper remains a reliable funding source for organizations year-round.

Risk Management and Credit Considerations in Commercial Paper

Understanding risk management in commercial paper is critical for both issuers and investors. Despite its reputation as a safe, short-term funding tool, commercial paper carries specific risks that must be carefully assessed in any market environment.

Primary Risks in Commercial Paper

Commercial paper presents several primary risks that set it apart from other money market instruments. The most significant risks include:

- Default risk: Since commercial paper is unsecured, if an issuer faces sudden financial distress, investors may not be repaid in full.

- Liquidity risk: In volatile markets, holders may struggle to sell their commercial paper before maturity without incurring losses.

- Rollover risk: Issuers often rely on rolling over maturing commercial paper. If market sentiment sours, refinancing can become challenging.

- Interest rate risk: Rising rates may reduce the market value of outstanding commercial paper.

Compared to Treasury bills, which are government-backed, commercial paper relies entirely on the issuer’s creditworthiness. The risk profile is generally low for top-rated issuers, but not risk-free.

| Instrument | Default Rate | Liquidity | Yield | Backing |

|---|---|---|---|---|

| Commercial Paper | Very Low* | High | Moderate | Unsecured |

| Treasury Bills | Near Zero | Very High | Low | Government |

*For investment-grade issuers.

Credit Quality and Enhancements

The credit quality of commercial paper issuers is central to risk management. Only firms with strong balance sheets and high short-term credit ratings can issue at competitive rates. Most investors seek ratings of A-1/P-1 or better from agencies like Moody’s or S&P.

To further reduce risk, issuers may use credit enhancements such as:

- Liquidity facilities: Backup credit lines from banks.

- Guarantees: Parent company or bank guarantees.

- Asset-backed commercial paper (ABCP): Backed by pools of receivables or other financial assets. For more on this, see the asset-backed security definition.

These enhancements provide an extra layer of security, making commercial paper more attractive to risk-averse investors.

Lessons from Market Stress

Historical market disruptions offer vital lessons for today’s commercial paper market. During the 2008 financial crisis, several issuers defaulted when investors rapidly withdrew funds, and liquidity evaporated. Even highly rated commercial paper faced sudden downgrades and failed rollovers.

The COVID-19 crisis in 2020 also tested the market’s resilience. Central banks intervened to restore confidence and liquidity, helping prevent widespread defaults.

These events underscore the importance of strong credit standards, diversified funding sources, and robust liquidity management when dealing with commercial paper.

Investor Due Diligence and Risk Metrics

Prudent investors conduct rigorous due diligence before purchasing commercial paper. Key steps include:

- Reviewing the issuer’s short-term credit ratings and financial statements.

- Analyzing the structure and legal protections, especially for ABCP.

- Monitoring market developments and rating agency updates.

Historical data shows that default rates for top-tier commercial paper remain below 0.05%. However, rating downgrades or market stress can quickly impact yields and liquidity.

By staying informed and evaluating each offering’s risk profile, investors can confidently integrate commercial paper into their portfolios.

Regulatory Landscape and Key Updates for 2025

Navigating the regulatory landscape for commercial paper is essential for both issuers and investors as we move into 2025. The commercial paper market operates primarily under the oversight of the U.S. Securities and Exchange Commission (SEC), which exempts CP with maturities of less than 270 days from full registration. Internationally, most developed markets follow similar principles, emphasizing transparency and investor protection. These frameworks aim to foster confidence and maintain stability in short-term funding markets, making regulatory awareness a fundamental part of effective commercial paper management.

Recent years have brought significant regulatory developments for commercial paper, especially after market stress events. Money market fund reforms have increased scrutiny and introduced new transparency requirements, affecting both the volume and structure of CP issuance. For deeper insights into these reforms and their impact on market resilience, refer to this Research Note: Commercial Paper Market Should be More Resilient After Money Fund Reforms. These updates have prompted issuers to adjust their strategies, focus on robust disclosure, and develop more sophisticated risk management practices.

Global standards, such as Basel III, are also shaping the future of commercial paper. These standards require financial institutions to strengthen capital and liquidity buffers, which impacts their participation in CP markets. As a result, issuers must adopt best practices for risk assessment and investor communication, while investors are encouraged to conduct more comprehensive due diligence. Enhanced reporting and frequent portfolio reviews are now considered standard to meet evolving expectations and regulatory demands in the commercial paper sector.

Issuers and investors continue to face compliance challenges amid these shifting requirements. Common issues include adapting to new disclosure rules, integrating technology for reporting, and managing cross-border regulatory differences. Solutions often involve leveraging compliance technology, ongoing training, and proactive engagement with regulators. Data from recent years shows increases in transparency and a shift in investor demand, reflecting the market's adaptation to evolving commercial paper regulations and a commitment to maintaining its role as a key source of short-term funding.

Investment Strategies and Portfolio Integration for Commercial Paper

Navigating the evolving landscape of commercial paper in 2025 requires both strategic insight and a clear understanding of its portfolio applications. As a cornerstone of short-term liquidity management, commercial paper offers institutional and corporate investors a flexible tool to optimize yield and manage risk. Its short maturities and strong credit profiles make it a preferred instrument for enhancing cash efficiency while maintaining high liquidity.

Strategic Approaches for Commercial Paper Integration

Incorporating commercial paper into portfolios begins with effective strategies such as laddering and maturity matching. Laddering involves staggering maturities to ensure regular liquidity events, reducing reinvestment risk and smoothing cash flows. Maturity matching aligns commercial paper maturities with anticipated cash needs, optimizing liquidity without sacrificing yield.

Investors also weigh options between traditional commercial paper and asset-backed commercial paper, each presenting unique risk-return profiles. For a deeper understanding of how ABCP functions and its role in the market, see the Asset-Backed Commercial Paper Program. These approaches allow investors to tailor their commercial paper exposure to specific portfolio objectives.

Diversification and Risk Management with Commercial Paper

Diversification is a key advantage of commercial paper, allowing investors to spread risk across issuers, sectors, and maturities. By combining commercial paper with other instruments, portfolios gain resilience against market volatility and credit events.

Public sector entities and large corporations commonly allocate a significant share of their short-term assets to commercial paper, attracted by its favorable yield relative to deposits and government securities. According to industry data, commercial paper can represent over 30 percent of institutional money market fund holdings, providing both return enhancement and liquidity. Prudent risk management includes ongoing monitoring of issuer credit ratings and market conditions.

Practical Tips for Evaluating Commercial Paper Investments

Selecting the right commercial paper investments in 2025 demands careful due diligence. Start by reviewing issuer financials, recent rating actions, and the legal structure of the instrument. Evaluate the maturity schedule—understanding the maturity date in finance is crucial for aligning investments with cash flow needs.

Diversify across multiple issuers and consider program size, rollover history, and market reputation. Track historical performance data and watch for regulatory changes that may impact yields or liquidity. By staying informed and proactive, investors can leverage commercial paper to achieve both stability and attractive returns in their short-term portfolios.

Trends and Future Outlook: Commercial Paper in 2025 and Beyond

The landscape for commercial paper in 2025 is rapidly evolving, shaped by digital transformation, sustainability mandates, and shifts in global finance. As organizations seek efficient funding solutions, commercial paper continues to adapt, offering both issuers and investors new opportunities for growth and risk management.

Digitalization and Fintech Disruption

Digital platforms and fintech innovations are revolutionizing the issuance and trading of commercial paper. Automation, electronic documentation, and blockchain integration are streamlining processes, reducing costs, and enhancing transparency. New digital marketplaces are making it easier for issuers to connect with investors directly, bypassing some traditional intermediaries. The underwriter role in securities remains pivotal in facilitating these placements, adapting to technology-driven workflows and regulatory standards.

ESG and Sustainable Finance in CP

Environmental, social, and governance (ESG) considerations are gaining momentum in the commercial paper market. Issuers are introducing ESG-linked commercial paper, tying proceeds to sustainability goals or performance metrics. Investors are increasingly demanding transparent reporting and green credentials, driving a shift toward responsible finance. Recent data shows ESG-linked CP volumes rose by over 20 percent in 2024, illustrating a strong appetite for sustainable short-term instruments.

Interest Rate Cycles and Market Demand

Interest rate fluctuations and macroeconomic trends play a crucial role in shaping commercial paper demand and pricing. In periods of rising rates, issuers may favor shorter maturities while investors seek higher yields. Conversely, economic uncertainty can lead to shifts in investor risk appetite and an increased focus on credit quality. The commercial paper market remains sensitive to central bank policy and global liquidity conditions, requiring agile strategies from both issuers and investors.

Non-Traditional Participants and Structured Products

The commercial paper market is witnessing greater participation from non-traditional issuers, such as technology companies and fintech startups, alongside established corporations and financial institutions. Asset-backed commercial paper and innovative structured products are evolving, offering tailored solutions for liquidity and risk management. Digital platforms are lowering barriers for new entrants, expanding the investor base and diversifying sources of funding.

Future Market Outlook and Projections

Looking ahead, experts forecast continued growth for commercial paper, driven by digital adoption, regulatory changes, and sustainability integration. Market projections indicate global CP issuance could surpass $2.5 trillion by 2026, with technology adoption rates exceeding 45 percent in major markets. As ESG factors become standard practice and digital platforms mature, commercial paper is positioned to remain a cornerstone of modern financial markets, offering flexibility and resilience amid changing economic cycles.

| Trend | 2024 Data/Forecast | 2025+ Outlook |

|---|---|---|

| Digital Issuance Adoption | 38% of total volume | >45% by 2026 |

| ESG-Linked CP Growth | +20% YoY | Mainstream in major markets |

| Non-Traditional Issuer Share | 12% | Rising to 18% |

| Global CP Issuance | $2.1 trillion | $2.5 trillion by 2026 |

The future of commercial paper will be defined by innovation, sustainability, and adaptability. Staying informed about these trends is essential for leveraging new opportunities and managing risks in the evolving market.

As you explore the vital role commercial paper plays in today’s dynamic markets, it’s clear that understanding its nuances is key for navigating 2025 with confidence. Whether you’re an investor, student, or simply curious about the forces shaping financial markets, leveraging historical context can give you a real edge. We believe that learning from the past helps you spot emerging trends and make smarter decisions for the future. If you’re ready to deepen your insights and help shape a platform that brings financial history to life, I invite you to Join our beta and help us bring history to life.