Cash Flow Statement Guide: Essentials for 2026 Success

Imagine navigating your business into 2026 with confidence, guided by a clear understanding of your financial position. The cash flow statement is your essential tool for gaining insights that give you an edge over competitors. This guide breaks down the complexities of the cash flow statement, showing you exactly how to use it for growth and stability. You will discover what a cash flow statement is, why it matters, its core components, and how to prepare and analyze it for better business decisions. By mastering these essentials, you can leverage your cash flow statement to drive success in 2026 and beyond.

What Is a Cash Flow Statement?

Understanding a cash flow statement is essential for anyone serious about financial management. It is one of the three core financial statements every business must prepare. The cash flow statement tracks all cash inflows and outflows over a specific period, acting as a bridge between the income statement and balance sheet. Unlike profit, which can be influenced by accounting choices, the cash flow statement emphasizes liquidity, showing exactly how much cash moves in and out. This focus on liquidity is vital for management, investors, and analysts alike. For example, a business might report high profits but still face insolvency if the cash flow statement shows negative cash flow. As Investopedia puts it, “The cash flow statement highlights liquidity, how well a business generates cash to fund growth and meet obligations.” For a broader look at how this fits into financial reporting, see financial statement fundamentals.

Definition and Purpose

A cash flow statement provides a clear summary of all cash transactions during a particular period. Its main purpose is to show how cash is generated and used, offering a transparent view of liquidity. The cash flow statement is distinct from the income statement, which measures profitability, and from the balance sheet, which captures assets and liabilities at a point in time. By tracking the actual movement of cash, the cash flow statement helps businesses avoid surprises that profit figures alone can hide. It is a crucial tool for decision-making, risk management, and regulatory compliance. For instance, a company may appear profitable but still struggle to pay bills if the cash flow statement reveals cash shortages. This document’s clarity supports both daily operations and long-term planning.

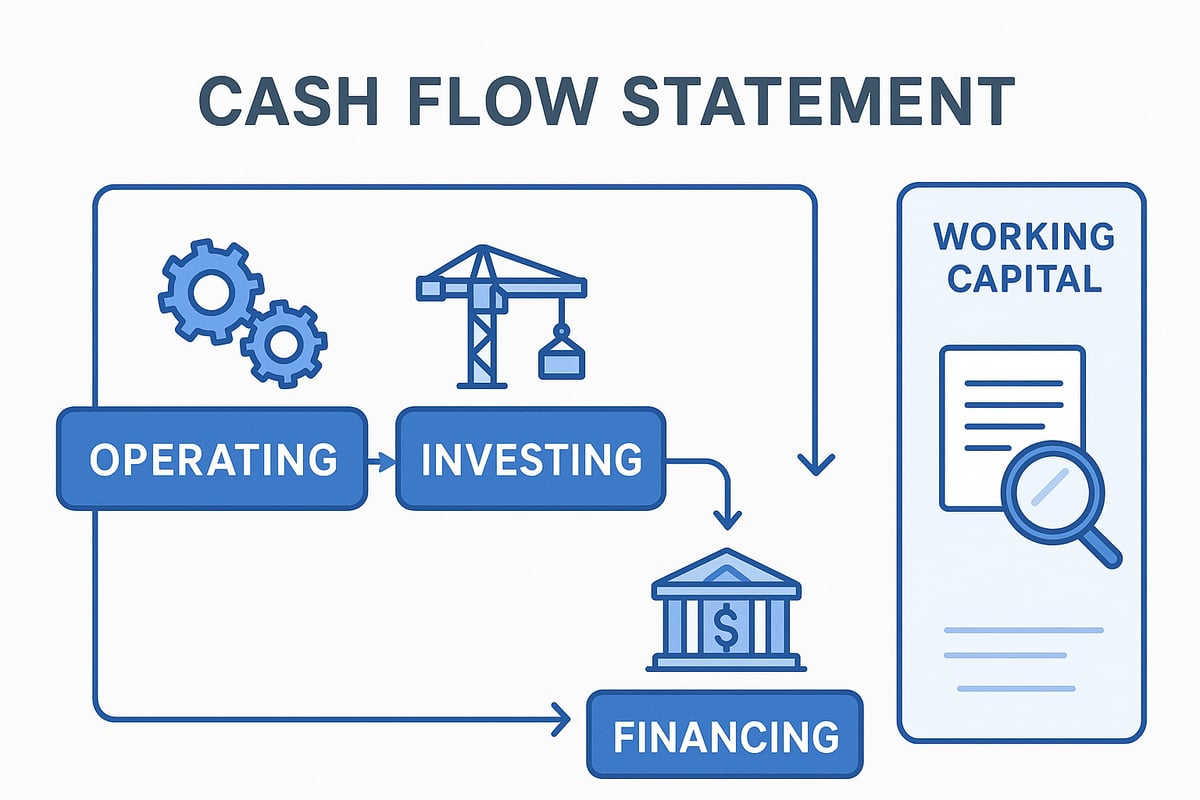

The Three Main Sections

Every cash flow statement is divided into three main sections: operating activities, investing activities, and financing activities. The operating section focuses on cash from core business operations, such as receipts from customers and payments to suppliers or employees. The investing section tracks cash used to purchase or sell assets, including property and equipment. The financing section details cash from borrowing, repaying loans, issuing stock, or paying dividends. Each section highlights a different aspect of financial health. For example, positive operating cash flow signals a business’s day-to-day viability, while investing cash flow can indicate growth or contraction. All major accounting frameworks, including GAAP and IFRS, require cash flow statements to follow this structure.

Accrual vs. Cash Accounting

The cash flow statement becomes especially important under accrual accounting. Unlike cash accounting, where transactions are recorded when cash changes hands, accrual accounting records revenue and expenses when they are earned or incurred. This can lead to non-cash items, such as depreciation or amortization, appearing on the income statement. These items affect reported profit but do not reflect actual cash movement. The cash flow statement adjusts for these differences, giving a true picture of cash available. For example, revenue recorded but not yet received can inflate income, but the cash flow statement will show if the business is actually collecting cash. As CFI notes, “Income statements and balance sheets don’t directly measure what happens to cash over a period.”

Who Uses Cash Flow Statements and Why

A wide range of stakeholders rely on the cash flow statement for informed decision-making. These include:

- Business owners and managers, who use it to manage liquidity and plan investments.

- Investors, who assess whether a company can sustain dividends and growth.

- Creditors and lenders, who evaluate loan repayment capacity.

- Analysts, who compare performance across businesses.

- Regulatory bodies, which require accurate reporting for compliance.

For example, investors often review the cash flow statement to determine if a company can continue paying dividends. According to CFI, over 90% of investors examine cash flow statements before making major decisions. This widespread use underscores its critical role in financial analysis and business strategy.

Why Cash Flow Statements Matter in 2026

Understanding the cash flow statement is crucial for any business aiming to thrive in 2026. This financial report provides a clear snapshot of how money moves in and out of your organization. By mastering it, you gain the insight needed to make informed choices, safeguard liquidity, and outperform competitors in a rapidly changing market.

Business Health and Liquidity

A cash flow statement reveals the true health of a business by showing exactly how much cash is available at any given moment. While profit is important, only cash ensures that bills, payroll, and suppliers are paid on time. Many companies have reported strong earnings, yet faced insolvency due to poor cash management.

Liquidity, highlighted in the cash flow statement, is vital for both survival and growth. Businesses with robust cash positions are better equipped to handle economic downturns, seize new opportunities, and invest confidently. As Investopedia states, “Cash flow statements are essential to understanding a company’s financial health.” This makes tracking cash flow an indispensable habit for any forward-thinking leader.

Decision-Making and Strategic Planning

The cash flow statement is a cornerstone of sound decision-making and strategic planning. It offers visibility into when cash is likely to come in and go out, which helps leaders set realistic budgets and timelines for projects or expansion. By analyzing historical cash flow patterns, organizations can predict their future cash needs, avoiding last-minute scrambles for funds.

Cash flow trends also signal when it may be time to seek outside financing or cut costs to maintain stability. Notably, 60% of failed small businesses cite cash flow problems as a primary cause, underscoring the need for proactive cash flow management. Relying on the cash flow statement, companies can make choices that align with both short-term needs and long-term goals.

Investor and Lender Confidence

Investors and lenders pay close attention to the cash flow statement when evaluating a business. Positive cash flow signals financial strength, making it easier to attract investment or secure loans on favorable terms. Banks routinely request cash flow statements as part of the loan approval process, using them to assess creditworthiness and repayment ability.

For investors, the cash flow statement provides key insights into a company’s ability to generate dividends and manage risk. Sustainable, growing cash flows indicate a stable business model, increasing investor confidence. Demonstrating strong cash flow through transparent reporting is a proven way to build trust with financial stakeholders.

Regulatory and Reporting Requirements

Regulatory frameworks such as GAAP and IFRS require all major businesses to prepare and disclose a cash flow statement. This statement is not just a best practice—it is a legal obligation for public companies and many private entities. Regulatory bodies and market analysts rely on these statements to verify compliance and ensure transparency.

For example, public companies must file a cash flow statement with the SEC, making it available to investors and analysts for review. As CFI notes, “Companies typically provide a cash flow statement for management, analysts and investors to review.” Adhering to these requirements not only avoids penalties but also demonstrates a commitment to transparency and good governance.

Adapting to 2026 Trends and Challenges

Business environments are evolving rapidly as digital transformation, global markets, and economic uncertainty reshape the landscape. In 2026, companies must embrace real-time cash flow monitoring and advanced forecasting to stay competitive. The cash flow statement is central to this evolution, especially as AI and automation tools become more widespread.

Forward-thinking organizations are now integrating technology to streamline cash flow analysis and spot risks sooner. For actionable insights on preparing for future volatility, see these Cash Flow Forecasting Best Practices, which outline strategies for stress-testing and improving receivables. Businesses that adapt their cash flow statement practices to these new trends are poised to gain a significant advantage in a changing world.

Components of a Cash Flow Statement: Deep Dive

Understanding the components of a cash flow statement is crucial for accurate financial analysis. Each section provides unique insights into a business's liquidity, growth, and financial strategy. Let's break down these components to see how they reveal the true story behind your numbers.

Operating Activities

The operating activities section of a cash flow statement details the cash generated or used by a company’s core business operations. This includes receipts from customers, payments to suppliers and employees, and other cash transactions related to day-to-day business.

To accurately represent cash flow, adjustments for non-cash items like depreciation and amortization are necessary. Changes in working capital, such as accounts receivable and inventory, also impact this section. For a deeper understanding of how working capital affects cash flow, see this working capital definition.

For example, if accounts receivable increase, it means cash has not been collected, reducing operating cash flow. Companies can use either the direct or indirect method to present this section. The indirect method is more common, starting with net income and adjusting for non-cash items and changes in working capital. The operating activities section is essential for understanding whether a business can sustain itself through its main activities.

Investing Activities

Investing activities in the cash flow statement show the cash spent on or received from long-term assets. This includes buying or selling property, equipment, and securities. When a company invests in new machinery or facilities, it often results in negative cash flow from investing activities, which can indicate growth or expansion.

Conversely, selling assets brings in cash, reflected as a positive figure in this section. Monitoring investing cash flows helps stakeholders assess how a company is allocating resources for future growth, and whether asset sales are supporting liquidity needs.

Financing Activities

The financing activities section outlines how a business raises and repays capital. This includes cash received from issuing shares or borrowing funds, as well as cash used to repay loans or pay dividends.

For instance, issuing new shares increases cash flow, while repaying debt or distributing dividends decreases it. Analyzing this section of the cash flow statement helps assess a company’s capital structure and financial flexibility. It reveals how management is funding operations and growth, and whether the business relies on external financing.

Net Increase/Decrease in Cash and Closing Balance

After totaling cash flows from operating, investing, and financing activities, the result is the net increase or decrease in cash for the period. This figure, when added to the opening cash balance, provides the closing cash balance for the period.

This reconciliation ensures the cash flow statement aligns with the balance sheet. A positive net cash flow increases liquidity, while a negative figure signals a potential need for external funding. This section is vital for monitoring a business’s ability to maintain liquidity and meet obligations.

Supplementary Disclosures and Non-Cash Transactions

Cash flow statements often include supplementary disclosures to provide a complete financial picture. Common disclosures are interest paid, taxes paid, and significant non-cash transactions such as acquiring assets via loans or issuing stock in exchange for assets.

Reporting these items is important for transparency and compliance with accounting standards. Non-cash transactions do not impact the cash position directly but can significantly affect the company’s financial structure. Proper disclosure ensures stakeholders have a clear, accurate view of the company’s cash flow dynamics.

Example of a Cash Flow Statement

Below is a simplified example of a cash flow statement structure, illustrating how the sections fit together:

| Section | Amount ($) |

|---|---|

| Operating Activities | 120,000 |

| Investing Activities | (50,000) |

| Financing Activities | 30,000 |

| Net Increase in Cash | 100,000 |

| Opening Cash Balance | 20,000 |

| Closing Cash Balance | 120,000 |

This example shows how the operating, investing, and financing sections interact to produce the final cash position. Understanding this structure is essential for effective cash flow management.

Step-by-Step: How to Prepare a Cash Flow Statement

Preparing a cash flow statement is a vital process for any business aiming for financial clarity and control. By following a systematic approach, you can ensure accuracy and compliance, while uncovering actionable insights for smart decision-making.

Step 1: Gather Financial Data

Start by collecting all the necessary financial documents for the period you wish to analyze. Typically, you will need the income statement and the balance sheet. Accurate, up-to-date records are essential for a reliable cash flow statement.

Ensure you identify the specific time frame, whether monthly, quarterly, or annually. For example, to prepare a yearly cash flow statement, use the year-end financial statements as your foundation.

Check that all data points are complete and consistent. Missing or outdated figures can lead to errors, affecting the integrity of your cash flow statement. Organizing your source documents at the outset saves time and reduces mistakes.

Step 2: Choose Direct or Indirect Method

Next, decide whether to use the direct or indirect method for presenting operating activities in your cash flow statement. The direct method lists actual cash receipts and payments, offering a straightforward view of cash movements. The indirect method, which is more common, starts with net income and adjusts for non-cash items and changes in working capital.

Most businesses favor the indirect method due to its alignment with accrual accounting and ease of preparation. For example, the indirect approach adjusts net income by adding back depreciation and accounting for changes in accounts receivable or payable.

Your choice of method impacts how clearly the cash flow statement reflects cash movement from core operations. Ensure consistency with your organization’s reporting policies.

Step 3: Calculate Operating Cash Flows

To determine operating cash flows, use your chosen method. The direct method requires listing all cash received from customers and cash paid to suppliers, employees, and others. The indirect method begins with net income and adjusts for non-cash expenses, such as depreciation and amortization, as well as changes in working capital.

For example, an increase in accounts receivable is subtracted, while a decrease is added. Non-cash expenses are always added back. Careful calculation here is crucial for a trustworthy cash flow statement. For more detailed guidance and examples, consult this Cash Flow Statement Preparation Guide.

Step 4: Determine Investing Cash Flows

This step focuses on cash flows from buying or selling long-term assets. Include cash spent on purchasing equipment, property, or investments, as well as proceeds from asset sales.

A negative figure in this section often indicates investments in growth, such as acquiring new machinery. Conversely, selling an asset generates a positive cash flow. Document each transaction clearly to avoid confusion.

Review all asset-related activities to ensure every relevant cash movement appears in this section of your cash flow statement. Proper classification is key for transparency and compliance.

Step 5: Determine Financing Cash Flows

Now, record all cash flows related to financing your business. This includes proceeds from loans, repayments of debt, issuing shares, and paying dividends.

For example, if you take out a new loan, it is a cash inflow. Repaying part of that loan is a cash outflow. Issuing equity or paying dividends also affects this section. Each financing activity shapes your business’s capital structure and must be reflected accurately in your cash flow statement.

Be sure to separate financing cash flows from operating and investing activities to maintain clarity.

Step 6: Reconcile Net Cash Flow and Closing Balance

After calculating cash flows from operating, investing, and financing activities, sum them to determine the net increase or decrease in cash for the period. Add this net change to your opening cash balance to arrive at the closing cash balance.

For example, if you started the period with $50,000, and your combined cash flows total $10,000, your closing cash balance will be $60,000. This final figure should match the cash amount on your balance sheet. Reconciling these numbers ensures your cash flow statement is accurate and complete.

Step 7: Review and Disclose Supplementary Information

Once the main sections are complete, review your cash flow statement for accuracy. Add required supplementary disclosures, such as interest and taxes paid during the period. Also, document significant non-cash transactions, like acquiring assets through loans or stock issuance.

Proper disclosure ensures compliance with accounting standards and provides stakeholders with a full picture of your business’s financial activities. Double-check that all regulatory requirements are met before finalizing your cash flow statement.

Example Walkthrough

Let’s walk through a simplified example. Assume your business had these activities over the year:

- Net income: $30,000

- Depreciation: $5,000

- Increase in accounts receivable: $2,000

- Equipment purchased: $10,000

- Loan received: $8,000

- Loan repaid: $3,000

- Opening cash balance: $15,000

Calculations:

- Operating: $30,000 + $5,000 - $2,000 = $33,000

- Investing: -$10,000

- Financing: $8,000 - $3,000 = $5,000

- Net change: $33,000 - $10,000 + $5,000 = $28,000

- Closing cash: $15,000 + $28,000 = $43,000

This example illustrates how each step contributes to a clear, actionable cash flow statement.

Analyzing and Interpreting Cash Flow Statements

Understanding how to analyze a cash flow statement is vital for making informed business decisions. A thorough analysis reveals hidden strengths and weaknesses, helping you steer your organization toward stability and growth.

Key Performance Indicators (KPIs) and Ratios

Evaluating a cash flow statement starts with identifying essential KPIs. These metrics turn raw data into actionable insights. Key ratios include:

- Operating Cash Flow Ratio: Measures liquidity by comparing operating cash flow to current liabilities.

- Free Cash Flow: Shows how much cash is available after capital expenditures, indicating funds for expansion or dividends.

- Cash Flow Margin: Calculates the percentage of cash generated from sales.

For investors, these ratios are the foundation for methods like the discounted cash flow method, which values a business based on future cash flows. Tracking these KPIs in your cash flow statement helps you assess operational strength and long-term potential.

Identifying Trends and Red Flags

Spotting trends in your cash flow statement is essential for proactive management. Look for patterns such as steadily rising or falling cash flows, which reveal much about business stability.

Red flags include:

- Persistent negative operating cash flow

- Discrepancies between net profit and cash flow

- Sudden, unexplained changes in cash movement

Leveraging resources like Cash Flow Statement Trends 2025 can help you stay ahead of emerging risks and opportunities. Regular trend analysis enables you to detect issues early and make timely adjustments.

Comparing Direct vs. Indirect Method Results

The method you use to prepare your cash flow statement can affect your interpretation. The direct method records actual cash receipts and payments, providing a clear view of cash sources and uses.

In contrast, the indirect method starts with net income and adjusts for non-cash items. While more common, it can sometimes obscure cash flow issues due to adjustments.

Comparing both methods, if possible, gives a fuller picture. The direct approach often highlights cash flow problems that might be hidden when using the indirect method.

Benchmarking Against Competitors and Industry

Benchmarking your cash flow statement against industry standards is crucial for context. By comparing KPIs and trends with similar businesses, you can identify strengths, weaknesses, and areas for improvement.

A simple benchmarking table might include:

| Metric | Your Company | Industry Average |

|---|---|---|

| Operating Cash Flow Ratio | 1.8 | 1.5 |

| Free Cash Flow Margin | 12% | 10% |

This comparative approach allows you to set realistic goals and demonstrate your financial health to stakeholders.

Real-World Case Studies

Case studies provide practical insight into cash flow statement analysis. For example, a technology startup with positive operating cash flow was able to survive an industry downturn, thanks to disciplined cash management.

On the other hand, a retail chain ignored warning signs in its cash flow statement, leading to liquidity issues despite reported profits. These real-world scenarios highlight the importance of regular, detailed analysis.

Common Mistakes and How to Avoid Them

Mistakes in analyzing a cash flow statement can distort your financial outlook. Common errors include:

- Ignoring non-cash items like depreciation or amortization

- Misclassifying transactions between operating, investing, and financing sections

- Overlooking required disclosures

To avoid these pitfalls, use reliable accounting software, ensure staff are well-trained, and regularly review your cash flow statement for accuracy. Accurate analysis protects your business from costly surprises.

Cash Flow Statement Pitfalls, Red Flags, and Best Practices

Understanding the cash flow statement is vital for financial clarity, but even seasoned professionals can fall into common traps. By recognizing pitfalls, spotting red flags, and following best practices, you can ensure your cash flow statement provides accurate insights and supports sound decision-making for 2026 and beyond.

Typical Pitfalls in Preparation and Reporting

Preparing a cash flow statement requires precision, yet several pitfalls can undermine its reliability. Common mistakes include using outdated or incomplete financial data, which can distort the statement's accuracy. Misallocating cash flows, such as recording loan repayments in the operating section instead of financing, is a frequent error.

Failing to account for non-cash items, like depreciation or asset swaps, can also mislead stakeholders. Omitting supplementary disclosures or not reconciling figures with the balance sheet may result in compliance issues. Avoid these pitfalls by conducting regular reviews, training staff, and utilizing robust accounting software when preparing your cash flow statement.

Red Flags for Businesses and Investors

A cash flow statement can reveal warning signs that demand immediate attention. Persistent negative cash flow from operations, despite reported profits, signals underlying issues with liquidity or revenue collection. Large, unexplained fluctuations between periods may indicate inconsistent accounting or operational instability.

Excessive reliance on financing activities to cover operational shortfalls is another red flag. If the operating section consistently shows outflows, the business might be masking problems with short-term borrowing. Analyzing the cash flow statement helps identify trends and potential problems early, allowing corrective action before they escalate.

Best Practices for 2026 and Beyond

To maximize the value of your cash flow statement, adopt best practices tailored for a rapidly evolving environment. Regularly monitor and forecast cash flows to anticipate challenges and seize growth opportunities. Integrate automation and AI tools for real-time analysis, reducing manual errors and increasing efficiency.

Cloud-based accounting platforms enable up-to-date tracking and easier collaboration across teams. Ongoing education for finance staff ensures compliance with new standards and improves analytical skills. For detailed guidance, Deloitte’s Statement of Cash Flows Roadmap is an excellent resource for interpreting the latest accounting requirements and industry practices.

Adapting to Changing Standards and Technology

The landscape for the cash flow statement is changing as regulatory standards evolve and technology advances. Stay informed about anticipated accounting changes to maintain compliance and transparency. Embrace AI-powered anomaly detection tools, which help spot irregularities and enhance accuracy.

Businesses that leverage technology for cash flow management gain a competitive edge, adapting swiftly to market shifts and regulatory updates. Regularly review industry trends and update processes to ensure your cash flow statement remains a reliable tool for strategic planning and reporting.

As you prepare to master cash flow statements for a successful 2026, remember that understanding the stories behind financial numbers can set you apart. By learning from historic market patterns and applying those insights to your business strategy, you’ll be better equipped to navigate future challenges and opportunities. If you’re curious to keep exploring financial markets through a historical lens—using interactive charts, AI-powered summaries, and original news—why not get involved early? Your perspective could help shape a unique resource for investors, students, and financial storytellers alike. Join Our Beta